Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

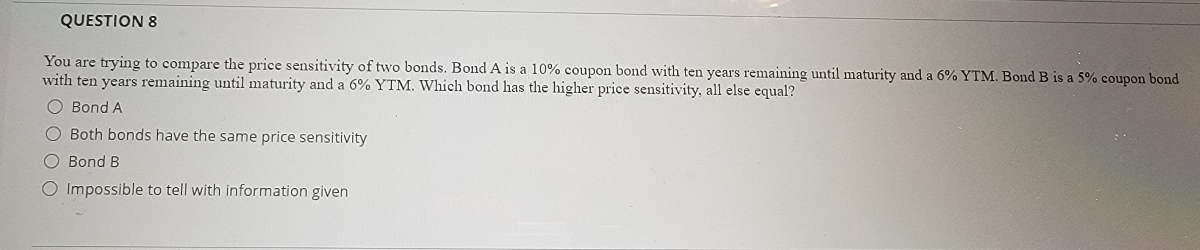

Transcribed Image Text:QUESTION 8

You are trying to compare the price sensitivity of two bonds. Bond A is a 10% coupon bond with ten years remaining until maturity and a 6% YTM. Bond B is a 5% coupon bond

with ten years remaining until maturity and a 6% YTM. Which bond has the higher price sensitivity, all else equal?

O Bond A

O Both bonds have the same price sensitivity

O Bond B

O Impossible to tell with information given

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Similar questions

- Give typing answer with explanation conclusionarrow_forward9. Interest Rate Risk. Suppose that you are a fixed income portfolio manager at Bourbon Street Capital. You have the following bonds issued by Royal, Inc. and Chartres, LLC in your portfolio and you want to understand the risk profile of your portfolio. Given that both bonds pay semiannual coupons, answer the following questions. (Remember to convert your answer to units of full years.) Coupon Yield to maturity Maturity (years) Royal, Inc. Chartres, LLC. Bond A Bond B 9% 8% 5 $100.00 $104.055 8% 8% 2 Par $100.00 Price $100.00 (a) What is the DV01 (at current prices) for bonds A and B? (b) What are the Macaulay Durations (at current prices) for the two bonds? (c) What are the modified durations for the two bonds? (d) What is the convexity of the two bonds?arrow_forwardA plot of the yields on bonds with different terms to maturity but the same risk, liquidity, and tax considerations is known as O A. a yield curve. B. a risk-structure curve. OC. a term-structure curve. 5- O D. an interest-rate curve. Suppose people expect the interest rate on one-year bonds for each of the next four years to be 3%, 6%, 5%, and 6%. If the expectations theory of the term structure of interest rates is correct, then the implied interest rate on bonds with a maturity of four years is nearest whole number). %. (Round your response to the 2- Refer to the figure on your right. Suppose the expected interest rates on one-year bonds for each of the next four years are 4%, 5%, 6%, and 7%, respectively. 1. 1.) Use the line drawing tool (once) to plot the yield curve generated. 3 Term to Maturity in Years 2.) Use the point drawing tool to locate the interest rates on the next four years. 5. 3- Interest Rate .....arrow_forward

- 不 Which of the bonds A to D is most sensitive to a 1%drop in interest rates from Consider the following bonds: 6.5% to 5.5% Which bond is least sensitive? Bond Data table is most sensitive. (Select from the drop-down menu.) (Click on the following icon in order to copy its contents into a spreadsheet.) Bond A BC D Coupon Rate (annual payments) 0.0% 0.0% 4.3% 7.7% Print Done Maturity (years) 10 15 15 10arrow_forwardNonearrow_forwardBASIC (Questions 1-17) 1. Interpreting Bond Yields Is the yield to maturity on a bond the same thing as the required return? Is YTM the same thing as the coupon rate? Suppose today a 10 percent coupon bond sells at par. Two years from now, the required return on the same bond is 8 percent. What is the coupon rate on the bond now? The YTM? LO 2 LO 2 2. Interpreting Bond Yields Suppose vou buy a 7 percent counon 20-veararrow_forward

- Bond A and Bond B are zero coupon bonds. Bond A has a maturity of 10 years and Bond B has a maturity of 15 years. This would mean that Bond B has more interest rate risk as compared to Bond A. Group of answer choices True Falsearrow_forward16arrow_forwardUse Macauly's Duration Price Approximation formula for this. Before a change in interest rates, your bond has the following characteristics: present value of $5,557.56, Duration of 3.69 years with market interest rates of 5%. Calculate the percentage change in the bond's price if market rates fall to 4.85%. Be sure to include the negative sign IF you think the price goes down. Iarrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education