ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

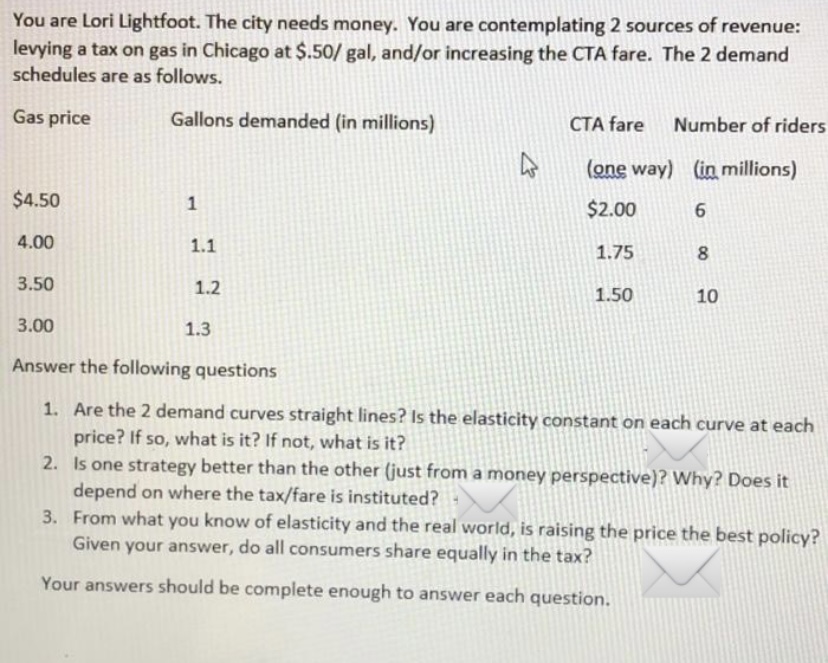

Transcribed Image Text:You are Lori Lightfoot. The city needs money. You are contemplating 2 sources of revenue:

levying a tax on gas in Chicago at $.50/ gal, and/or increasing the CTA fare. The 2 demand

schedules are as follows.

Gas price

Gallons demanded (in millions)

CTA fare

Number of riders

(one way) (in millions)

$4.50

1

$2.00

4.00

1.1

1.75

3.50

1.2

1.50

10

3.00

1.3

Answer the following questions

1. Are the 2 demand curves straight lines? Is the elasticity constant on each curve at each

price? If so, what is it? If not, what is it?

2. Is one strategy better than the other (just from a money perspective)? Why? Does it

depend on where the tax/fare is instituted?

3. From what you know of elasticity and the real world, is raising the price the best policy?

Given your answer, do all consumers share equally in the tax?

Your answers should be complete enough to answer each question.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Similar questions

- 2. Hope, Arkansas (home of both ex-President Bill Clinton and former Presidential candidate Mike Huckabee), has a subway system, for which a one-way fare is $1.50. There is pressure on Governor Huckabee to reduce the fare by one-third, to $1.00. The Governor is dismayed, thinking that this will mean Hope is losing one-third of its revenue from sales of subway tickets. The Governor's economic advisor reminds him that he is focusing only on the price effect and ignoring the quantity effect. Explain why the Governor's estimate of a one-third loss of revenue is likely to be an overestimate using elasticity of demand.arrow_forwarddo fastarrow_forwardthan high high minimum prices and taxation, what policies could be used to tackle binge drinking? 1. Other otherarrow_forward

- Note:- Do not provide handwritten solution. Maintain accuracy and quality in your answer. Take care of plagiarism.Answer completely.You will get up vote for sure.arrow_forward4. What do you think would be the effect on the equilibrium price and quantity of marijuana as a result of its consumption being legalized? Give reasons for your answer.arrow_forward1. In 2020 due to state deregulations ride sharing company X managed to lower its price which led to higher quantity demanded of their rides (a movement along the demand curve). The accompanying table describes what happened to prices and the quantity demanded of their service. Using the midpoint method, calculate the price elasticity of demand for the rides. 2008 2012 Quantity demanded (rides) 130 million 420 million Average price (per ride) $25 $15arrow_forward

- Note:- Do not provide handwritten solution. Maintain accuracy and quality in your answer. Take care of plagiarism. Answer completely. You will get up vote for sure.arrow_forwardA sales tax is imposed on good A. The supply of good A is not perfectly elastic or perfectly inelastic. Suppose that the demand for good A becomes more inelastic. (a) Will the tax burden on sellers increase or decrease? (b) Will the DWL increase or decrease?arrow_forwardWhat is the price elasticity of demand(Using the Midpoint method) when the price changes from $10 to $13? If the Government imposes a tax of $6 per burrito, how many burritos will be sold in the market?arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education