FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Question

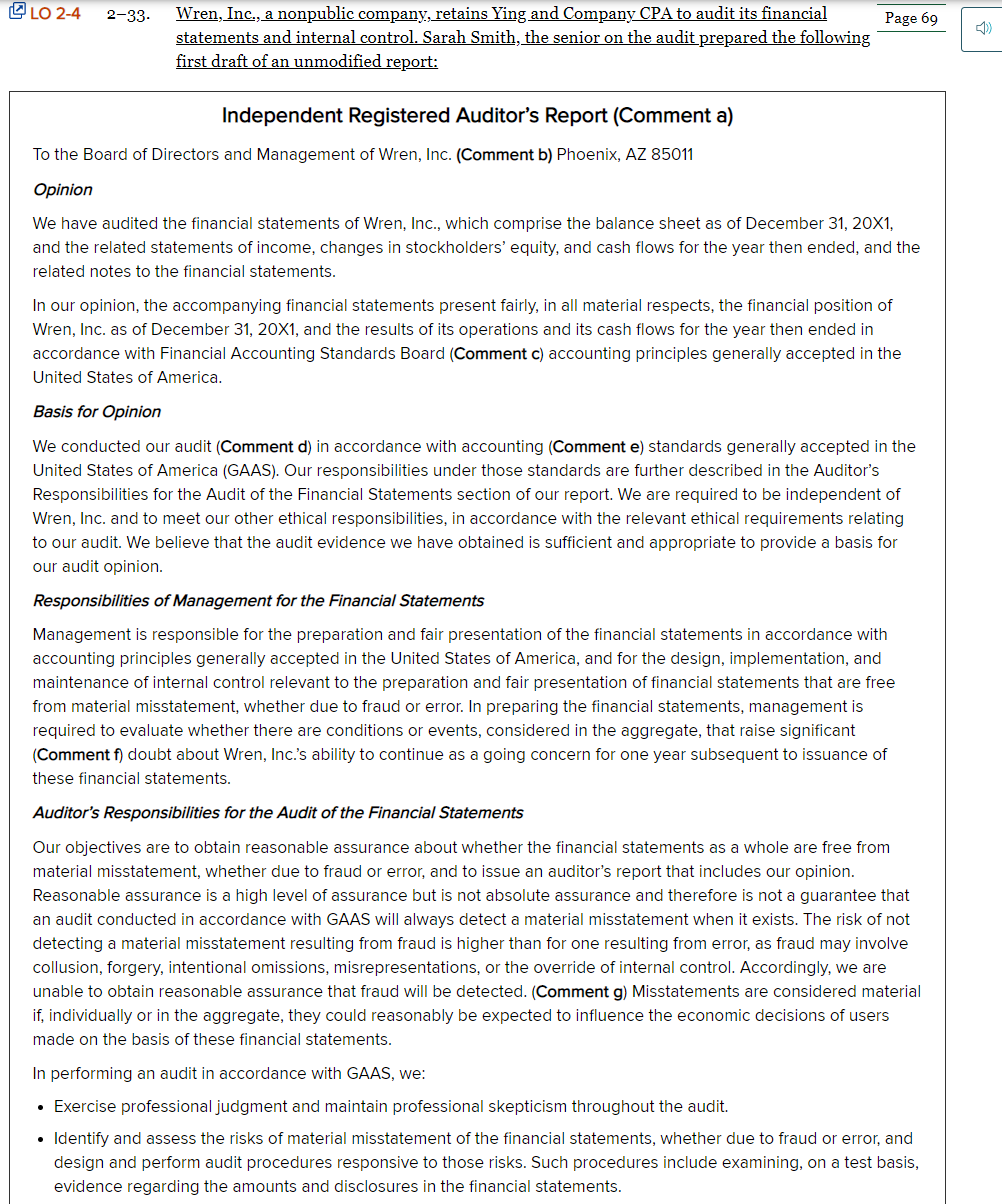

Transcribed Image Text:O LO 2-4

Wren, Inc., a nonpublic company, retains Ying and Company CPA to audit its financial

statements and internal control. Sarah Smith, the senior on the audit prepared the following

first draft of an unmodified report:

2-33.

Page 69

Independent Registered Auditor's Report (Comment a)

To the Board of Directors and Management of Wren, Inc. (Comment b) Phoenix, AZ 85011

Opinion

We have audited the financial statements of Wren, Inc., which comprise the balance sheet as of December 31, 20X1,

and the related statements of income, changes in stockholders' equity, and cash flows for the year then ended, and the

related notes to the financial statements.

In our opinion, the accompanying financial statements present fairly, in all material respects, the financial position of

Wren, Inc. as of December 31, 20X1, and the results of its operations and its cash flows for the year then ended in

accordance with Financial Accounting Standards Board (Comment c) accounting principles generally accepted in the

United States of America.

Basis for Opinion

We conducted our audit (Comment d) in accordance with accounting (Comment e) standards generally accepted in the

United States of America (GAAS). Our responsibilities under those standards are further described in the Auditor's

Responsibilities for the Audit of the Financial Statements section of our report. We are required to be independent of

Wren, Inc. and to meet our other ethical responsibilities, in accordance with the relevant ethical requirements relating

to our audit. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for

our audit opinion.

Responsibilities of Management for the Financial Statements

Management is responsible for the preparation and fair presentation of the financial statements in accordance with

accounting principles generally accepted in the United States of America, and for the design, implementation, and

maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free

from material misstatement, whether due to fraud or error. In preparing the financial statements, management is

required to evaluate whether there are conditions or events, considered in the aggregate, that raise significant

(Comment f) doubt about Wren, Inc.'s ability to continue as a going concern for one year subsequent to issuance of

these financial statements.

Auditor's Responsibilities for the Audit of the Financial Statements

Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from

material misstatement, whether due to fraud or error, and to issue an auditor's report that includes our opinion.

Reasonable assurance is a high level of assurance but is not absolute assurance and therefore is not a guarantee that

an audit conducted in accordance with GAAS will always detect a material misstatement when it exists. The risk of not

detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve

collusion, forgery, intentional omissions, misrepresentations, or the override of internal control. Accordingly, we are

unable to obtain reasonable assurance that fraud will be detected. (Comment g) Misstatements are considered material

if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users

made on the basis of these financial statements.

In performing an audit in accordance with GAAS, we:

• Exercise professional judgment and maintain professional skepticism throughout the audit.

• Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, and

design and perform audit procedures responsive to those risks. Such procedures include examining, on a test basis,

evidence regarding the amounts and disclosures in the financial statements.

Transcribed Image Text:• Exercise professional judgment and maintain professional skepticism throughout the audit.

• Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, and

design and perform audit procedures responsive to those risks. Such procedures include examining, on a test basis,

evidence regarding the amounts and disclosures in the financial statements.

• Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are

appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of Wren,

Inc's internal control. Accordingly, no such opinion is expressed. (comment h)

• Evaluate the appropriateness of accounting policies used and the reasonableness of significant accounting

estimates made by management, as well as evaluating the overall presentation of the financial statements.

• Conclude whether, in our judgment, there are conditions or events, considered in the aggregate, that raise

substantial doubt about Wren, Inc's ability to continue as a going concern for a reasonable period of time.

We are required to communicate with those charged with governance regarding, among other matters, the planned

scope and timing of the audit, significant audit findings, and certain internal controlrelated matters that we identified

during the audit.

Ying and Company, CPAS

Phoenix, Arizona February 3, 20X2 (Comment i)

(Comment j)

Respond as to the accuracy of the following comments made by a reviewer of the report:

Page 70

Comment is Correct (yes

Reviewer's Comments

or no)

a. Delete "REGISTERED."

b. “Management" should not be included.

c. Delete “Financial Accounting Standards Board."

d. “Audit" should be replaced with “examination."

e. “Accounting" should be replaced with "audit."

f. “Serious" should be replaced with “Significant."

g. The preceding sentence should be deleted.

h. The preceding sentence should be deleted.

i. The date should be year-end-December 31, 20X2

j. The report is required to indicate the year in which we began serving as

Wren, Inc's auditor.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps with 3 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- The standard unqualified opinion based on the audit of a public company's financial statements includes a. A discussion of Key Audit Matters if KAMs are discovered. b. A reference to Key Audit Matters if no KAMs are discovered. c. A statement that the CPA firm is registered with the AICPA. d. An indication of how long the firm has served as the company's auditors. e. A Basis for Opinion section preceding the Opinion of Financial Statements section.arrow_forwardMurray & Co., CPAs completed the audit of Classic, Inc., a non-issuer, on March 1, 2018 for a January 31, 2018 fiscal year end. The audit team encountered no significant issues and found no material misstatements. Murray & Co. has audited Classic, Inc. for several years and past audits did not reveal any significant issues or material misstatements. The audit team partner determined that a standard (unmodified) report on Classic, Inc.'s financial statements was appropriate. The auditors’ report, drafted by I.M. Nu, a staff assistant, is provided below. Independent Auditor’s Report To the Board of Directors and Shareholders Classic, Inc. Report on the Audit of the Financial Statements OpinionWe have audited the financial statements of Classic Inc., which comprise the balance sheet as of January 31, 2021 and the related statements of changes in shareholders' equity and cash flows for the year then ended, and the related notes to the financial statements. In our opinion, the…arrow_forwardGordon & Moore, CPAS, were the auditors of Fox & Company, a brokerage firm. Gordon & Moore examined and reported on the financial statements of Fox, which were filed with the Securities and Exchange Commission. Several of Fox's customers were swindled by a fraudulent scheme perpetrated by two key officers of the company. The facts establish that Gordon & Moore were negligent, but not reckless or grossly negligent, in the conduct of the audit, and neither participated in the fraudulent scheme nor knew of Its existence. The customers are suing Gordon & Moore under the antifraud provisions of Section 10(b) and Rule 10b-5 of the Securities Exchange Act of 1934 for alding and abetting the fraudulent scheme of the officers. The customers' sult for fraud is predicated exclusively on the negligence of the auditors in falling to conduct a proper audit, thereby failing to discover the fraudulent scheme. Required: Answer the following, setting forth reasons for any conclusions stated. a. What is…arrow_forward

- You are a partner incharge of the audit for Bargin Ltd, a private company. The finishing of the audit report is pending for the income year 2018 and you have recorded some situations where possible action is required They are listed below: Bargin Ltd, carries its property, plant, and equipment accounts at current market values. Current market values exceed historical cost by a highly material amount, and the effects are pervasive throughout the financial statements. Management of Bargin Ltd, refuses to allow you to observe, or make, any counts of inventory. The recorded book value of inventory is highly material. You were unable to confirm accounts receivable with Bargin Ltd, customers. However, because of detailed sales and cash receipts records, you were able to perform reliable alternative audit procedures. One week before the end of fieldwork, you discover that the audit manager on the Bargin Ltd, engagement owns a material amount of Bargin Ltd, common stock. You relied…arrow_forwardYou a partner incharge of the audit for Bargin Ltd, a private company. The completion of the audit report is pending for the income year 2018 and you have recorded some situations where possible action is required They are listed below: Bargin Ltd, carries its property, plant, and equipment accounts at current market values. Current market values exceed historical cost by a highly material amount, and the effects are pervasive throughout the financial statements. Management of Bargin Ltd, refuses to allow you to observe, or make, any counts of inventory. The recorded book value of inventory is highly material. You were unable to confirm accounts receivable with Bargin Ltd, customers. However, because of detailed sales and cash receipts records, you were able to perform reliable alternative audit procedures. One week before the end of fieldwork, you discover that the audit manager on the Bargin Ltd, engagement owns a material amount of Bargin Ltd, common stock. You relied…arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education