ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

QUESTION 22 Why is the

Answer please Both the Questions...

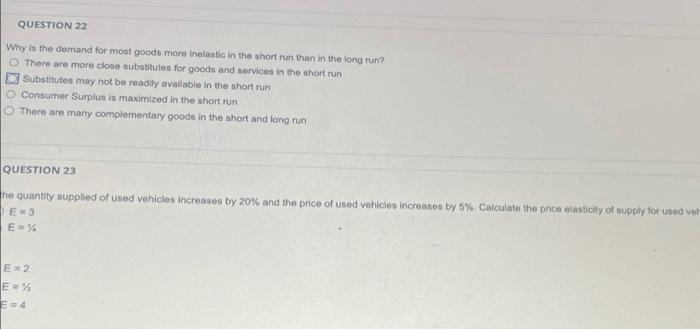

Transcribed Image Text:QUESTION 22

Why is the demand for most goods more inelastic in the short run than in the long run?

O There are more close substitutes for goods and services in the short run

Substitutes may not be readily available in the short run

O Consumer Surplus is maximized in the short run

O There are many complementary goods in the short and long run

QUESTION 23

the quantity supplied of used vehicles increases by 20% and the price of used vehicles increases by 5%. Calculate the price elasticity of supply for used vel

E-3

E=%

E=2

E=%

E=4

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 4 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Calculating elasticity Draw a set of coordinate axes on a piece of graph paper. Label the horizontal axis from 0 to 50 units and the vertical axis from $0 to $20 per unit. Draw a demand curve that intersects the vertical axis at $10 and the horizontal axis at 40 units. Draw a supply curve that intersects the vertical axis at $4 and has a slope of 1. Make the following calculations for these curves, using the midpoint formula: a. What is the price elasticity of demand over the price range $5 to $7? b. What is the price elasticity of demand over the price range $1 to $3?arrow_forwardTable 5.6 Quantity Supplied Price 10 $10 20 $20 30 $30 40 $40 50 $50 Refer to Table 5.6. If price decreases from $50 to $30, the price elasticity of supply is: Group of answer choices 10 5 0.5 2 1arrow_forward1. The equation for a demand curve is P = 45 - 3Q. What is the elasticity in moving from a quantity of 4 to a quantity of 5? 2. The equation for a demand curve is P = 4/Q. What is the elasticity of demand as the price falls from 10 to 8? What is the elasticity of demand as the price falls from 18 to 16? Would you expect these answers to be the same?arrow_forward

- QUESTION 1 20 16 12 8 4 P S 0 D 0 4 8 12 16 20 24 01. What is the "own price elasticity of demand" between price = $10 and price = $6 a) 1 b) 2/3 c) 3/2 d) 2/5 e) 5/2arrow_forwardPrice Quantity $20 12 $18 17 $16 20 $14 24 $12 30 $10 36 $ 8 40 $ 6 44 $ 4 48 Using the above table, over which range is the price elasticity of demand Unitary?arrow_forwardGrilled cheese sandwiches are $4, and the quantity demanded is 60. When the price falls to $3/sandwich, the quantity demanded rises to 80. What is the price elasticity of grilled cheese sandwiches? Widgets are $3, and the quantity demanded is 200. When the price of widgets rises to $5, the quantity demanded falls to 100. What is the price elasticity of demand for widgets? Coffee is $1 per cup, and the quantity demanded is 500. The price of coffee rises to $1.25 per cup, and the quantity demanded falls to 400. What is the price elasticity of demand for cups of coffee?arrow_forward

- Answer all parts please...arrow_forwardIf the price elasticity of demand for a good is 8, then if the price decreased by 6 percent, what would happen to the quantity demand? Table 1 Price Quantity $100 0 $80 10 $60 20 $40 30 $20 40 $0 50arrow_forwardWhen the price of a good is $6, the quantity demanded is 50 units per month; when the price is $8, the quantity demanded is 30 units per month. Find the arc price elasticity of demand for this good and comment on it.arrow_forward

- #4 Determining the price elasticity of demand of a product involves all of the following factors, but NOT the total number of firms in a market. the availability of substitutes to the product. whether the product is a luxury or a necessity.arrow_forwardIf the price of product X increases from $10 to $12, the quantity demanded for gasoline (X) will fall from 100 to 82 and the quantity demanded for product Y also falls from 90 to 63 but the quantity demanded product Z will increase from 50 to 76. a.What is the price elasticity of demand for X?b.What is cross-price elasticity of demand for Ywith respect to price X? What are X and Y?c.What is cross-price elasticity of demand for Zwith respect to price X? What are X and Z?arrow_forwardThe following table contains a monthly demand and supply schedule for large, single- topping, carry-out pizza Pizza Price (per pack) Quantity demanded for pizza (per pack) Quantity supplied for pizza (per pack) Quantity demanded for good Y $21 6000 7900 6000 $19 7000 7200 8000 $17 8000 6500 10000 (A) Calculate the price elasticity Of demand (PED) for good X when price fall from S 19 to $ 17. (B) Suppose you are the sellers of pizza based on the value of PED obtained In your answer for Question(A), would you or would you not raise the price of pizza? Why? (C)What S the cross elasbcity of demand (CED) of Good Y when price of carry-out pizza fall from $19 to S17? How is pizza and the Good Y related?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education