ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

Transcribed Image Text:D

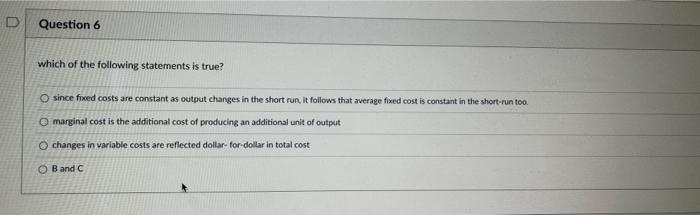

Question 6

which of the following statements is true?

O since fixed costs are constant as output changes in the short run, it follows that average fixed cost is constant in the short-run too.

O marginal cost is the additional cost of producing an additional unit of output

O changes in variable costs are reflected dollar-for-dollar in total cost

OB and C

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Assume that Peter's short run Total Cost Curve is TC = 20,000q– 200q² +q° . Calculate his (short run) Average Total Cost (ATC) for quantities of 50, 100, and 150 and sketch his ATC curve given the values you calculated. IIII -LJ-J-L- -LJ-J-1- IIII IIII -TT-1 ----- +-+-- - -- 1-t- 11 3D %3D - -+ -- - -- -4 %3D ד - ררו T-T-r- %3D %3D %3D %3D %3D +--- ー- +-ナー ゴーキ-キート- %3D IIII -Larrow_forwardSolve it correctlyarrow_forwardQuestion 7 When a firm produces 100 units of output, the firm's marginal cost is $10, average variable cost is $5 and average total cost is $8. What is the fixed cost? O $100 O $200 $0 O $300 O $50arrow_forward

- By doubling a machine's inputs, the output increases three times. How does this affect cost and what does this characterize? O Per unit costs rises, Diseconomies of Scale O Per unit costs falls, Economies of Scale O Per unit costs remains the same, Constant Economies of Scale O Per unit cost rises, Economies of scale Per unit cost falls, diseconomies of scale.arrow_forwardA firm's total cost is $12,000. Its variable cost is $5,500. What is the firm's fixed cost? $3,500 O $2.22 $6,500 O $4,500 Incorrect. none of the other answers are correctarrow_forwardPlease help me answer these questions. Thanks in advancearrow_forward

- These occur when doubling all of the inputs to a production process doubles the output. The shape of a firm's long-run average cost curve depends both on returns to scale in production and the effect of scale on the prices it pays for its inputs. O Decreasing returns to scale in production O Constrained optimisation problem O Constant returns to scale in production O Decreasing returns to scalearrow_forwardThe N.M. Corporation has exactly the same costs of production as last year except for fixed costs, which are $50,000 this year compared to $30,000 last year. Which of the following statements is false? O The total cost curve will be the same this year as last year. O The fixed cost curve will have the same slope this year as last year. O The variable cost curve will be the same this year as last year. O The marginal cost curve will be the same this year as last year.arrow_forwardCost LRAC B A Quantity Figure 1 Long run average cost curve for a firm Figure 1 shows a long run average cost curve for a firm. If the firm increases output from point A to point B this is an example of: Select one: O i. A change in production function O ii. Economies of scale iii. Constant unit cost O iv. Diseconomies of scalearrow_forward

- QUESTION 1 When diseconomies of scale occur: CA. the long-run average total cost O B. marginal cost intersects average OC the long-run average total cost O D. average fixed costs curve falls total cost curve rises will risearrow_forwardYou learn that a firm's average total costs (ATC) and average variable costs (AVC) are exactly equal. What does that mean? O Marginal cost is zero O ATC and AVC must be equal to zero O Average fixed costs (AFC) are zero O Economic profit is positive O Economic profit is negativearrow_forwardBob produces candles. The average total cost reaches its minimum at a quantity O A. the same as the quantity at which the average variable cost reaches its minimum. O B. lower than the quantity at which the average variable cost reaches its minimum. O C. the same as the quantity at which the marginal cost is at a maximum. O D. the same as the quantity at which the marginal cost is at a minimum. O E. greater than the quantity at which the average variable cost reaches its minimum.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education