CONCEPTS IN FED.TAX.,2020-W/ACCESS

20th Edition

ISBN: 9780357110362

Author: Murphy

Publisher: CENGAGE L

expand_more

expand_more

format_list_bulleted

Question

None

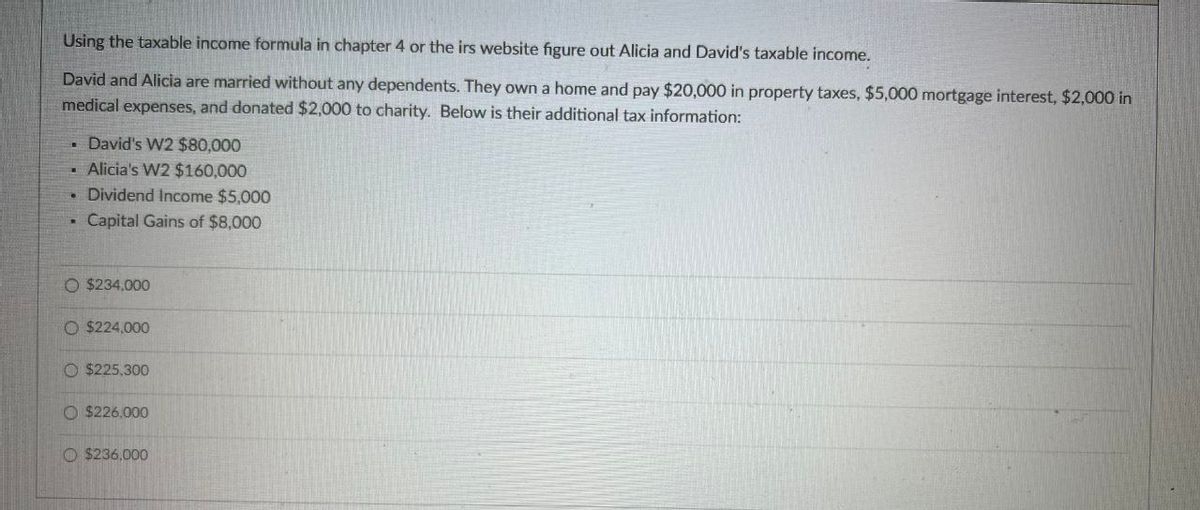

Transcribed Image Text:Using the taxable income formula in chapter 4 or the irs website figure out Alicia and David's taxable income.

David and Alicia are married without any dependents. They own a home and pay $20,000 in property taxes, $5,000 mortgage interest, $2,000 in

medical expenses, and donated $2,000 to charity. Below is their additional tax information:

•

David's W2 $80,000

Alicia's W2 $160,000

. Dividend Income $5,000

Capital Gains of $8,000

O $234,000

$224,000

O $225,300

O $226,000

$236,000

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps

Knowledge Booster

Similar questions

- In each of the following problems, identify the tax issue(s) posed by the facts presented. Determine the possible tax consequences of each issue that you identify. Thans grandmother dies and leaves him jewelry worth 40,000. In addition, he is the beneficiary of a 100,000 life insurance policy that his grandmother had bought before she retired.arrow_forwardDana and Larry are married and live in Texas. Dana earns a salary of $45,000 and Larry has $25,000 of rental income from his separate property. If Dana and Larry file separate tax returns, what amount of income must Larry report? $0 $22,500 $25,000 $47,500 None of the abovearrow_forwardLeroy and Amanda are married and have three dependent children. During the current year, they have the following income and expenses: Salaries 120,000 Interest income 45,000 Royalty income 27,000 Deductions for AGI 3,000 Deductions from AGI 9,000 a. What is Leroy and Amandas current year taxable income and income tax liability? b. Leroy and Amanda would like to lower their income tax. How much income tax will they save if they validly transfer 5,000 of the interest income to each of their children? Assume that the children have no other income and that they are entitled to a 1,050 standard deduction.arrow_forward

- Sheila, a single taxpayer, is a retired computer executive with a taxable income of 100,000 in the current year. She receives 30,000 per year in tax-exempt municipal bond interest. Adam and Tanya are married and have no children. Adam and Tanyas 100,000 taxable income is comprised solely of wages they earn from their jobs. Calculate and compare the amount of tax Sheila pays with Adam and Tanyas tax. How well does the ability-to-pay concept work in this situation?arrow_forwardJason and Mary are married taxpayers in 2019. They are both under age 65 and in good health. For 2019 they have a total of $41,000 in wages and $700 in interest in come. Jason and Mary's deductions for adjusted gross income amount to $5,000 and their itemized deductions equal $18,700. They have two children, ages 32 and 28, that are married and provide support for themselves. What is the amount of Jason and Mary's adjusted gross income?$____________ What is the amount of their itemized deductions or standard deduction? $____________ What is their taxable income? $____________arrow_forwardBrad and Angie are married and file a joint return. For year 14, they had income from wages in the amount of 100,000 and had the following capital transactions to report on their income tax return: What is the amount of capital loss carryover to year 15? a. (155,000) b. (152,000) c. (132,000) d. (125,000)arrow_forward

- Otto and Monica are married taxpayers who file a joint tax return. For the current tax year, they have AGI of $80,300. They have excess depreciation on real estate of $67,500, which must be added back to AGI to arrive at AMTI. The amount of their mortgage interest expense for the year was $25,000, and they made charitable contributions of $7,500. If Otto and Monica's taxable income for the current year is $47,800 determine the amount of their AMTI. _______________________________________________________________________arrow_forwardStewie, a single taxpayer, operates an activity as a hobby. Brian, a different taxpayer, operates a similar activity as a bona fide business. Stewie's gross income from his activity is $5,000 and his expenses are $6,000. Brian's gross income and expenses are coincidentally the same as Stewie. Neither Stewie nor Brian itemize, but both have other forms of taxable income. What is the impact on taxable income for Stewie and Brian from these activities? Stewie will report $0 income and Brian will report a $1,000 loss. Stewie will report $5,000 income and $0 deduction and Brian will report a $1,000 loss. Stewie and Brian will report $0 taxable income. Stewie and Brian will report a $1,000 loss. Stewie will report a $1,000 loss and Brian will report $5,000 income.arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you