Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

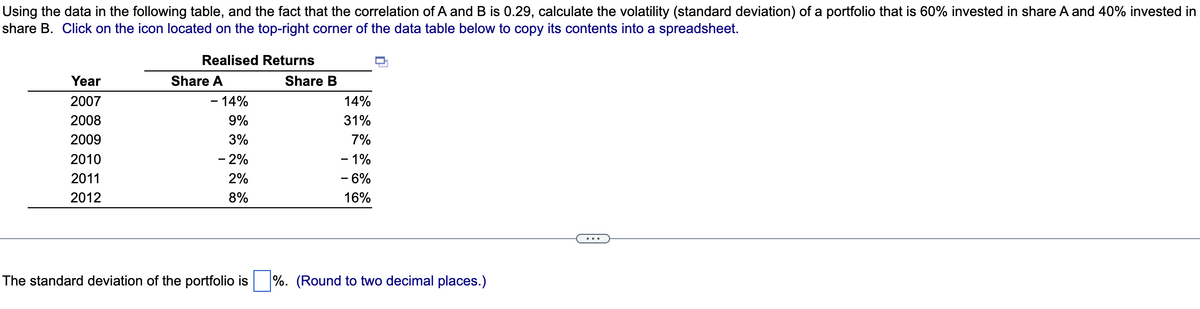

Transcribed Image Text:Using the data in the following table, and the fact that the correlation of A and B is 0.29, calculate the volatility (standard deviation) of a portfolio that is 60% invested in share A and 40% invested in

share B. Click on the icon located on the top-right corner of the data table below to copy its contents into a spreadsheet.

Realised Returns

Year

Share A

Share B

2007

- 14%

14%

2008

2009

9%

3%

31%

7%

2010

- 2%

- 1%

2011

2%

- 6%

2012

8%

16%

The standard deviation of the portfolio is ☐ %. (Round to two decimal places.)

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Similar questions

- f2. Subject :- Accountingarrow_forwardF1 plaese help.....arrow_forwardHistorical Realized Rates of Return You are considering an investment in either individual stocks or a portfolio of stocks. The two stocks you are researching, Stock A and Stock B, have the following historical returns: ΤΑ -17.00% 37.00 28.00 ЇВ -6.00% 16.00 -12.00 -5.00 47.00 23.00 21.00 a. Calculate the average rate of return for each stock during the 5-year period. Do not round intermediate calculations. Round your answers to two decimal places. Stock A: Stock B: % % Std. Dev. b. Suppose you had held a portfolio consisting of 50% of Stock A and 50% of Stock B. What would have been the realized rate of return on the portfolio in each year? What would have been the average return on the portfolio during this period? Do not round intermediate calculations. Round your answers to two decimal places. Negative values, if any, should be indicated by a minus sign. Year 2017 2018 2019 2020 2021 Average return c. Calculate the standard deviation of returns for each stock and for the portfolio.…arrow_forward

- Using the data in the following table, calculate the volatility (standard deviation) of a portfolio that is 75% invested in stock A and 25% in stock B.arrow_forwardSuppose Johnson & Johnson and the Walgreen Company have the expected returns and volatilities shown below, with a correlation of 22.4%. Johnson & Johnson Walgreen Company E [R] 6.5% 10.7% SD [R] 15.5% 19.9% For a portfolio that is equally invested in Johnson & Johnson's and Walgreen's stock, calculate: a. The expected return. b. The volatility (standard deviation). a. The expected return. The expected return of the portfolio is %. (Round to one decimal place.)arrow_forwardGiven the time series of historical stock returns below, what is the standard deviation? (Hint: theexpected return is 4%)Time Period 1 2 3 4 5return (%) 5% -7% 12% 13% -3% a. 7.585%b. 0.79%c. 8.888%d. 2.155%arrow_forward

- (Expected return and risk) The following data represent returns for the common stocks over a one- year period. Probability Returns Google -20% 8.5% 12% -18% 4.6% 0.1 0.2 0.2 0.3 0.2 ATT -10% 4% 19% 20% -6% The standard deviation of Google return is numbers.) _%. (Keep the sign and two decimalarrow_forwardUsing the data in the following table, calculate the volatility (standard deviation) of a portfolio that is 60% invested in stock A and 40% in stock B. The volatility of the portfolio is %. (Round to two decimal places.) Data table (Click on the following icon in order to copy its contents into a spreadsheet.) Year Stock A Stock B 2010 2011 2012 2013 2014 2015 -10% 19% 4% -3% 5% 12% 19% 39% 24% -8% -8% 35% Print Done Хarrow_forwardCurrent Attempt in Progress To achieve a zero standard deviation for a portfolio, calculate the weights of stock A and stock B, assuming the correlation coefficient is-1. Use the following information. (Round intermediate calculations and final answers to 2 decimal places, e.g. 31.21%.) State of the economy Probability of Expected return on Expected return on occurrence stock A in this state stock B in this state High growth 30% 41.5% 56.5% Moderate growth 25% 21.5% 26.5% Recession 45% -11.5% -21.5% Weight of stock A % Weight of stock B %arrow_forward

- Am. 340.arrow_forwardColonel Motors (C) Separated Edison (S) Expected Return 10% 8% Standard Deviation 6% 3% Please represent graphically all potential combinations of stocks C and S, if the correlation coefficient between the returns of stocks C and S is: A) 1 B) 0 C) -1 Please report these investment opportunity sets in the corresponding Excel sheets.arrow_forwardUsing the data in the following table, and the fact that the correlation of A and B is 0.56, calculate the volatility (standard deviation) of a portfolio that is 60% invested in stock A and 40% invested in stock B. Realized Returns Year Stock A 2008 -6% 2009 12% 2010 7% 2011 -2% 2012 2% 2013 5% Stock B Question content area bottom 12% 35% 10% -2% -12% 33% Part 1 The standard deviation of the portfolio is %.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education