Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

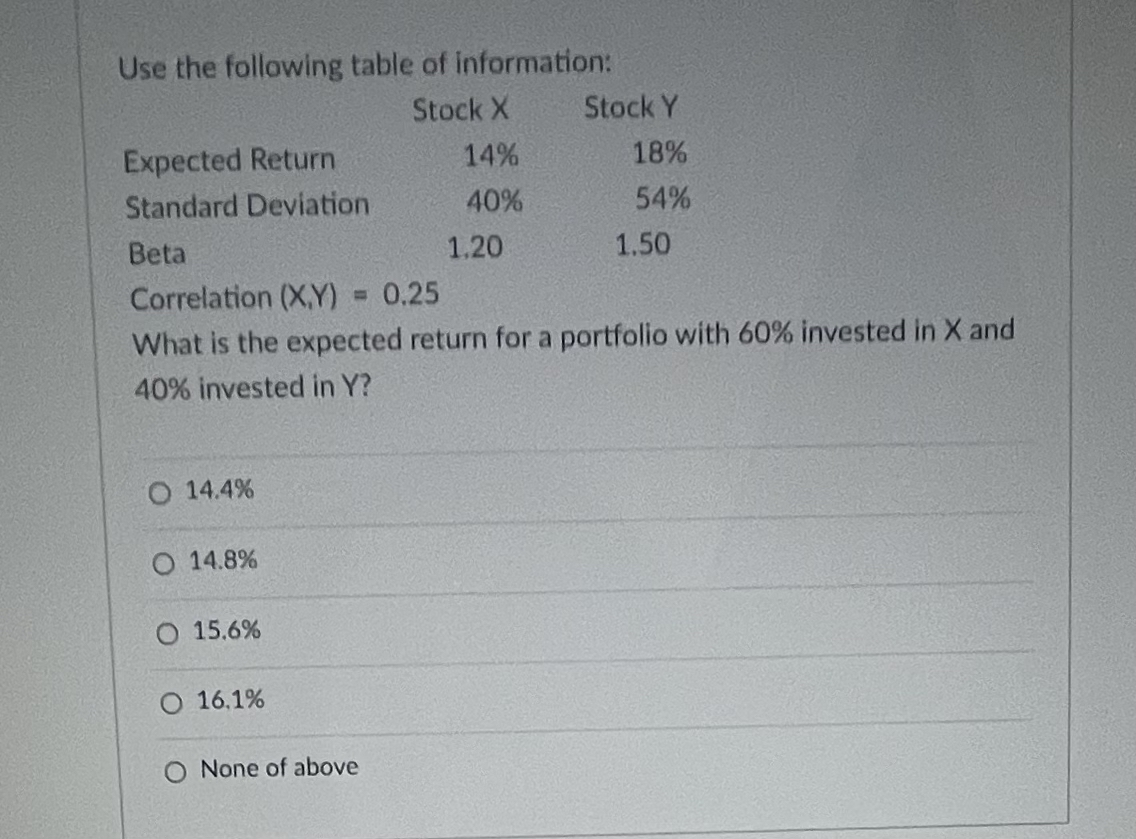

Transcribed Image Text:Use the following table of information:

Stock X

Stock Y

Expected Return

14%

18%

Standard Deviation

40%

54%

Beta

1.20

1.50

Correlation (X,Y) = 0.25

What is the expected return for a portfolio with 60% invested in X and

40% invested in Y?

O 14.4%

O 14.8%

O 15.6%

16.1%

None of above

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- only typed answer Stock A's stock has a beta of 1.30, and its required return is 15.25%. Stock B's beta is 0.80. If the risk-free rate is 4.75%, what is the required rate of return on B's stock? (Hint: First find the market risk premium.) Select the correct answer. a. 11.15% b. 11.18% c. 11.21% d. 11.24% e. 11.27%arrow_forwardAccounting Use the following information: Stock A B Good state 12% 17% Bad state 0% -1% Assume there is 60% probability that the good state occurs and 40% chance the bad state occurs. What is the expected return of a portfolio that is 9% invested in stock A and 1-9% invested in B? (Please use 5 decimal places, this should be written in percentage return, so an answer of 23.143% should be written at .23143)arrow_forwardU Assume CAPM holds. We know expected return and beta of two stocks: Stock A: E[ra] = 10% and beta_a = 1.5 Stock B: E[rb] = 5% and beta_b = 0.5 What would be the expected return of a stock that has a beta of 0.9? O 6.5% Ⓒ7% O 7.5% O 6% Question 5 Which of the following statements is false? o The CAPM follows from equilibrium conditions in a frictionless mean-variance economy with rational investors According to CAPM, everyone should hold a mix of the market portfolio and the risk-free asset. According to CAPM, everyone can generate positive return by buying positive alpha stocks and by selling negative alpha stocks. According to CAPM, the expected return on a stock is a linear function of its beta.arrow_forward

- Consider the following data State of Nature Prob. Stock A Return Boom 0.3 16.00% Normal 0.6 14.20% Recession 0.1 8.00% What is the expected return for Stock A? Group of answer choices 14.12% 12.14% 15.12% 14.00%arrow_forwardConsider the following stock return scenarios for three stocks: Stock Stock A B Economy Up Average Down 8% 5% 0% 2% 3% 4% Stock с 12% 0% -5% If each state of the economy is equally likely, calculate the expected return and population standard deviation for a portfolio invested entirely in Stock A. Which stock should be added to the portfolio to reduce risk?arrow_forwardGiven the following information on a investment portfolio: Stock Name Expected returns $invested in stock Standard deviation of returntesla 15.5% 3750 10.3%microsoft 9.8% 5000 5.6%pfizer 13.8% 1250 12% Which stock should have the most systematic risk?arrow_forward

- Consider the following expected returns, volatilities, and correlations: Stock Duke Energy Microsoft Wal-Mart Expected Standard Correlation with Correlation with Correlation with Return Duke Energy Deviation 14% 6% 44% 24% 23% 14% 1.0 -1.0 0.0 Microsoft -1.0 1.0 0.7 Wal-Mart 0.0 0.7 1.0 a) Consider a portfolio consisting of only Duke Energy and Microsoft. What is the percentage of your investment (portfolio weight) that you would place in Duke Energy stock to achieve a risk-free investment. b) What are the expected return and volatility of a portfolio that consists of a long position of $10,000 in Wal-Mart and a short position of $2000 in Microsoft? c) What are the expected return and platility of a portfolio that has $3000 invested in Duke Energy, $4000 invested in Microsoft, and $3000 invested in Walmart stock?arrow_forwardNonearrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education