FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Question

1. Using the problem above, how much is the cash investment of PA RIN?

2. Using the same problem, how much is the total assets?

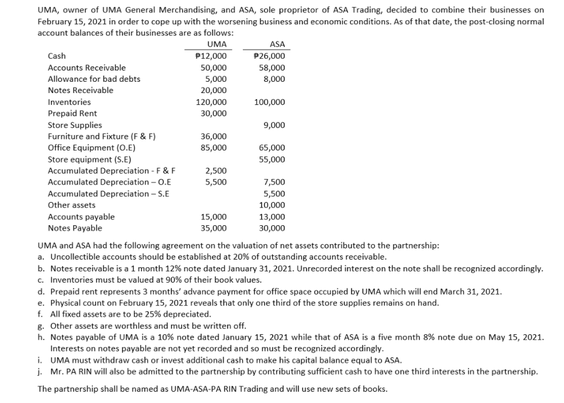

Transcribed Image Text:UMA, owner of UMA General Merchandising, and ASA, sole proprietor of ASA Trading, decided to combine their businesses on

February 15, 2021 in order to cope up with the worsening business and economic conditions. As of that date, the post-closing normal

account balances of their businesses are as follows:

UMA

ASA

Cash

P12,000

P26,000

Accounts Receivable

50,000

58,000

Allowance for bad debts

5,000

8,000

Notes Receivable

20,000

Inventories

120,000

100,000

Prepaid Rent

30,000

Store Supplies

9,000

36,000

85,000

Furniture and Fixture (F & F)

Office Equipment (O.E)

Store equipment (S.E)

Accumulated Depreciation - F& F

Accumulated Depreciation - 0.E

Accumulated Depreciation - S.E

Other assets

65,000

55,000

2,500

7,500

5,500

5,500

10,000

Accounts payable

15,000

13,000

Notes Payable

35,000

30,000

UMA and ASA had the following agreement on the valuation of net assets contributed to the partnership:

a. Uncollectible accounts should be established at 20% of outstanding accounts receivable.

b. Notes receivable is a 1 month 12% note dated January 31, 2021. Unrecorded interest on the note shall be recognized accordingly.

c. Inventories must be valued at 90% of their book values.

d. Prepaid rent represents 3 months' advance payment for office space occupied by UMA which will end March 31, 2021.

e. Physical count on February 15, 2021 reveals that only one third of the store supplies remains on hand.

f. All fixed assets are to be 25% depreciated.

g. Other assets are worthless and must be written off.

h. Notes payable of UMA is a 10% note dated January 15, 2021 while that of ASA is a five month 8% note due on May 15, 2021.

Interests on notes payable are not yet recorded and so must be recognized accordingly.

i. UMA must withdraw cash or invest additional cash to make his capital balance equal to ASA.

i. Mr. PA RIN will also be admitted to the partnership by contributing sufficient cash to have one third interests in the partnership.

The partnership shall be named as UMA-ASA-PA RIN Trading and will use new sets of books.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- 3. Which of the three types of cash flows could best be desribed as cash-basis net income? Operating Investing Financingarrow_forward3. Which of the three types of cash flows could best be desribed as cash-basis net income? Operating Investing Financingarrow_forwardGive an example of the Cash-Flow Approach?arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education