Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

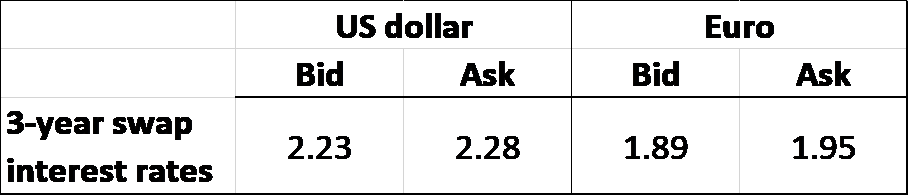

Tyson Inc. is entering into a 3-year pay-euros and receive-dollars cross currency swap. The 3-year swap interest rates are quoted in the table below. At what rate will Tyson receive dollars and at what rate will Tyson pay euros?

Question 8 options:

|

|

Receive at 2.28% and pay at 1.89% |

|

|

Receive at 2.23% and pay at 1.95% |

|

|

Receive at 2.28% and pay at 1.95% |

|

|

Receive at 2.23% and pay at 1.89% |

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Commercial bank A and Savings bank B entered into a swap contract. The swap has a notional principal amount of $200 million and calls for Commercial Bank A to make annual floating interest rate payment of LIBOR minus 0.75% to Savings Bank B. In return, Savings Bank B pays fixed 8% interest rate to Commercial Bank A. If LIBOR is 8%, what is the net payment?arrow_forwardAnswer a) and b) Problem 3: Interest Swap Companies A and B have been offered the following rates per annum on a $50 million five-year loan: Company A Company B Floating LIBOR +0.7% LIBOR +1.0% Fixed 6.0% 7.5% Company A requires a floating-rate loan and company B requires a fixed-rate loan. a) Design a swap that will net a bank, acting as an intermediary, 30 basis points (0.3%) per annum and that is equally attractive to the two companies. Illustrate the swap with a diagram. b) Determine the effective financing costs for A and B.arrow_forwardJon establishes a long position of one T-bond future today for a settlement price of 101'02. The exchange requires an initial margin of $2700 and a maintenance margin of $2500. Below are the next two days closing price on this contract. Day 1: settlement price100'31 Day 2: settlement price 99'30 The margin account balance after two days is Numeric Response dollarsarrow_forward

- Company A borrows $2 million at Libor + 3% for five years and Company B takes a $2 million five-year loan at a fixed 7% interest rate. The two companies enters into an interest rate swap arrangement, where Company A will pay Company B a fixed 6% interest rate on a notional $2 million and Company B will pay Company A Libor + 2% on a notional $2 million. What has been accomplished? Question 16 options: Both companies have been able to link the payment to Libor Company A has achieved payments mirroring a fixed interest rate while Company B will be paying a floating rate Company A has achieved payments mirroring a floating interest rate while Company B has achieved a fixed rate Both companies will be paying the same interest rate for the duration of the loanarrow_forwardYou can borrow CAD (Canadian dollar) at 8 percent, which is 2 percent above the swap rate, or at CAD Libor + 1 percent. If you want to borrow at a fixed-rate, what is the best way: direct, or synthetic (that is, using a floating-rate loan and a swap)? Direct borrowing would be to borrow at a fixed rate of 8 percent. Synthetic fixed-rate cad borrowing would be to borrow CAD at a floating rate of Libor + 1 percent and arrange a swap where you pay fixed 6 percent CAD in exchange for receiving CAD Libor.arrow_forwardA trader purchased an at the money 1 year OTC put option on the DAX index for a cost of Eur 10000. What is the traders minimum potential credit Exposure to the counter part over the term of the tradearrow_forward

- H3. A 2-year swap based on LIBOR is entered into on 30/6/2010 with current spot 3 month LIBOR at 0.54%. The swap is based on a notional principal of $100m What is the swap rate? Please show proper step by step calculationarrow_forwardNetflix company has entered into a plain vanilla interest rate swap on $2,500,000 notional principal. The company pays fixed rate of 7.0% on payments that occur at 60-day intervals. Six payments remain with the next one due in exactly 60 days. On the other side of the swap, the company receives payments based on the LIBOR rate. Describe the transaction that occurs between the company and the dealer at the end of the first period if the appropriate LIBOR rate is 8.5%.arrow_forwardA 2-year swap based on LIBOR is entered into on 30/6/2010 with current spot 3 month LIBOR at 0.54%. The swap is based on a notional principal of $100m What is the swap rate?arrow_forward

- Ford has a 5 year $100m fixed rate loan with Citibank at 0.061 (annual rate). Ford now thinks rates will go lower and calls Goldman Sachs for a swap and receives a quote of 0.029 / 0.030 (annual rate) against 6m LIBOR flat and executes the swap. Assume at the next rate reset, 6m LIBOR is 0.018 (annual rate). What is Ford's net effective annual interest rate for that rate reset in decimal terms to three decimal places? (eg 5.10% = 0.051)arrow_forwardUse the following table of spot rates: Years to Maturity Annual Effective Spot Rate 3.00% 2 3.60% 3. 3.85% 4 4.05% 5. 4.20% For a 2-year-deferred, 3-year interest rate swap with the level notional amount is I million and 1-year spot rate at time 3 is 3%, what is the amount of the net settlement payment at time 4? Is this amount paid by the payer, or by the receiver? O a. 15,950 paid by the receiver Ob. 16,950 pay by the receiver O. 15,950 paid by the payer Od. 16,950 paid by the payer O e. None of the abovearrow_forward15. The table below presents the costs of borrowing for Caterpillar and Tesla, and the a Swap Bank quote against LIBOR. Caterpillar would like to get a $5,000,000.00 floating rate loan. Tesla would like to get a $5,000,000.00 fixed rate loan. How much can Tesla save each year by entering a swap agreement? (a) $37,000 (b) $9,500 (c) $8,000 (d) $27,500 Fixed-Rate Borrowing Cost Floating-Rate Borrowing Cost Caterpillar Tesla 3.00 6.50 LIBOR LIBOR +2.60 Swap Bank Quote Bid Ask 3.19% 3.74% (e) None of the abovearrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education