FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Topic Video

Question

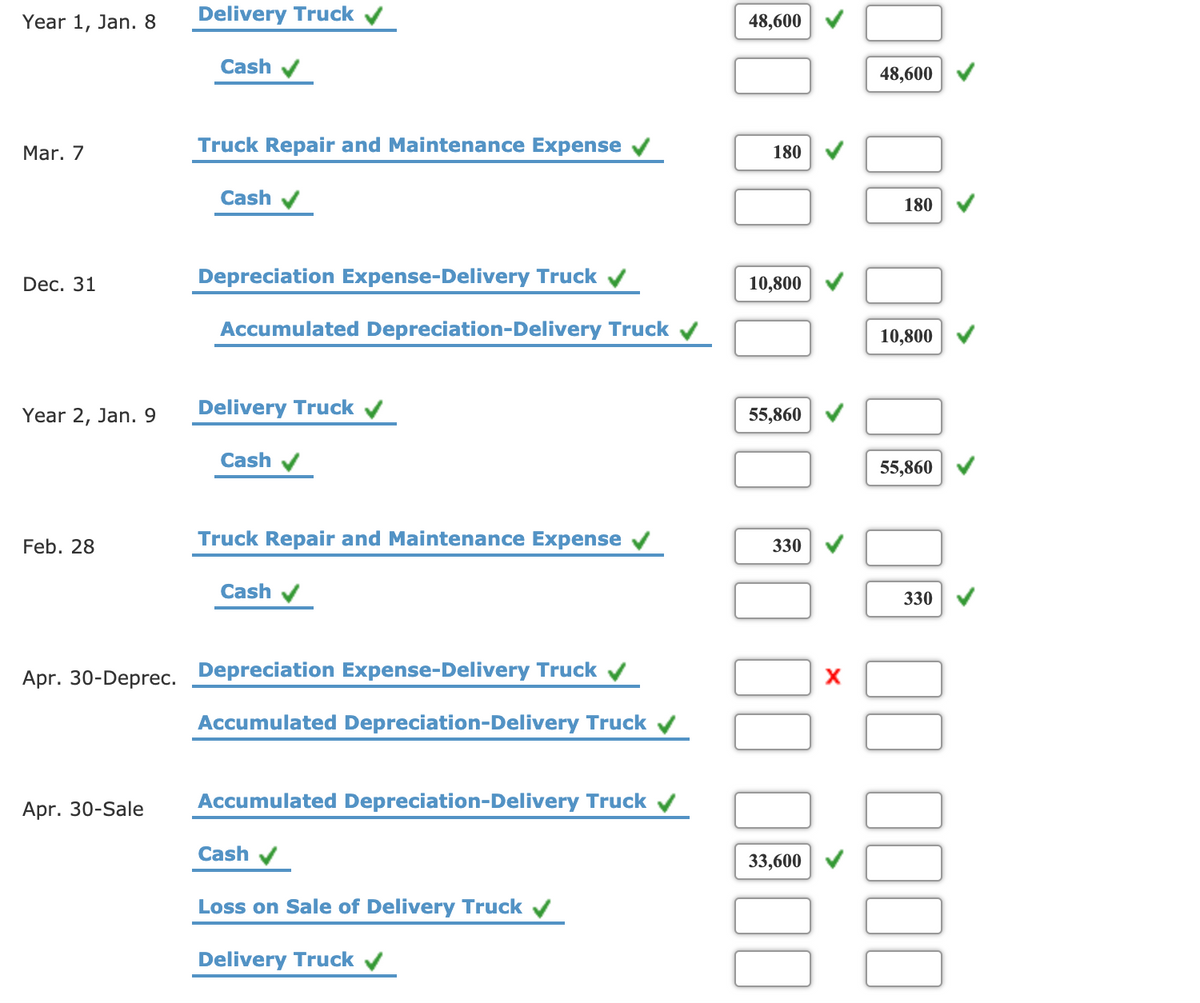

Transcribed Image Text:Year 1, Jan. 8

Delivery Truck v

48,600

Cash

48,600

Truck Repair and Maintenance Expense v

Mar. 7

180

Cash v

180

Dec. 31

Depreciation Expense-Delivery Truck v

10,800

Accumulated Depreciation-Delivery Truck v

10,800

Year 2, Jan. 9

Delivery Truck v

55,860

Cash

55,860

Feb. 28

Truck Repair and Maintenance Expense v

330

Cash v

330

Apr. 30-Deprec.

Depreciation Expense-Delivery Truck v

Accumulated Depreciation-Delivery Truck v

Apr. 30-Sale

Accumulated Depreciation-Delivery Truck v

Cash

33,600

Loss on Sale of Delivery Truck v

Delivery Truck v

Transcribed Image Text:Transactions for Fixed Assets, Including Sale

The following transactions and adjusting entries were completed by Robinson Furniture Co. during a three-year period. All are related to the use of delivery equipment.

The double-declining-balance method of depreciation is used.

Year 1

Jan. 8. Purchased a used delivery truck for $48,600, paying cash.

Mar. 7. Paid garage $180 for changing the oil, replacing the oil filter, and tuning the engine on the delivery truck.

Dec. 31. Recorded depreciation on the truck for the fiscal year. The estimated useful life of the truck is 9 years, with a residual value of $10,200 for the truck.

Year 2

Jan. 9. Purchased a new truck for $55,860, paying cash.

Feb. 28. Paid garage $330 to tune the engine and make other minor repairs on the used truck.

Apr. 30. Sold the used truck for $33,600. (Record depreciation to date in Year 2 for the truck.)

Dec. 31. Record depreciation for the new truck. It has an estimated trade-in value of $10,100 and an estimated life of 7 years.

Year 3

Sept. 1. Purchased a new truck for $85,000, paying cash.

Sept. 4. Sold the truck purchased January 9, Year 2, for $34,000. (Record depreciation to date in Year 3 for the truck.)

Dec. 31. Recorded depreciation on the remaining truck. It has an estimated residual value of $15,300 and an estimated useful life of 10 years.

Required:

Journalize the transactions and the adjusting entries. If an amount box does not require an entry, leave it blank. Do not round intermediate calculations. Round your final

answers to the nearest cent.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Presented here are selected transactions for Cullumber Limited for 2024. Cullumber uses straight-line depreciation and records adjusting entries annually. Jan. 1 Sold a delivery truck for $19.190 cash. The truck cost $67,530 when it was purchased on January 1, 2021, and was depreciated based on a four-year useful life with a $6,290 residual value. Sept. 1 Dec. 30 Sold computers that were purchased on January 1, 2022. They cost $11,628 and had a useful life of three years with no residual value. The computers were sold for $540 cash. Retired equipment that was purchased on January 1, 2015. The equipment cost $146,400 and had a useful life of 10 years with no residual value. No proceeds were received. Show Transcribed Text Gain on Disposal Vehicles Assume that, when the delivery truck was sold on January 1, the accountant only recorded a debit to Cash and a credit to Gain on Disposal. Because of this, also assume that the accountant recorded depreciation on this asset for 2024. What…arrow_forwardSale of Equipment Equipment was acquired at the beginning of the year at a cost of $612,500. The equipment was depreciated using the straight-line method based on an estimated useful life of 9 years and an estimated residual value of $49,470. a. What was the depreciation for the first year? Round your answer to the nearest cent. $ b. Using the rounded amount from Part a in your computation, determine the gain(loss) on the sale of the equipment, assuming it was sold at the end of year eight for $106,489. Round your answer to the nearest cent and enter as a positive amount. $Loss c. Journalize the entry to record the sale. If an amount box does not require an entry, leave it blank. Round your answers to the nearest cent. Cash Accumulated Depreciation-Equipment Loss on Sale of Equipment Equipmentarrow_forwardBlue Co. purchased equipment on October 4, 20X1 at a cost of $63,000. The equipment has an estimated useful life of 4 years and an estimated salvage value of $3,000. Blue Co. uses the straight-line depreciation method. Blue Co.’s fiscal year-end is December 31. Assuming Blue Co. uses the half-year convention, what was the accumulated depreciation as of December 31, 20X2? (Round all results to the nearest whole dollar.) a. $30,000 b. $22,500 c. $15,000 d. $7,500arrow_forward

- Entries for Sale of Fixed Asset Equipment acquired on January 5 at a cost of $107,600, has an estimated useful life of 12 years, has an estimated residual value of $9,200, and is depreciated by the straight-line method. a. What was the book value of the equipment at December 31 the end of the fourth year? $ b. Assuming that the equipment was sold on April 1 of the fifth year for 67,585. 1. Journalize the entry to record depreciation for the three months until the sale date. Round your answers to the nerest whole dollar if required. 2. Journalize the entry to record the sale of the equipment. If an amount box does not require an entry, leave it blank. Do not round intermediate calculations.arrow_forwardEquipment acquired on January 8 at a cost of $150,800, has an estimated useful life of 15 years, has an estimated residual value of $8,900, and is depreciated by the straight-line method. a. What was the book value of the equipment at December 31 the end of the fourth year? - Assuming that the equipment was sold on April 1 of the fifth year for 105,335. 1. Journalize the entry to record depreciation for the three months until the sale date. Round your answers to the nerest whole dollar if required. 2. Journalize the entry to record the sale of the equipment. If an amount box does not require an entry, leave it blank. Do not round intermediate calculations.arrow_forwardKnife Edge Company purchased tool sharpening equipment on July 1, 20Y5, for $16,200. The equipment was expected to have a useful life of three years and a residual value of $900. Instructions: a. Determine the amount of depreciation expense for the years ended December 31, 20Y5, 20Y6, 20Y7 and 20Y8 by the straight-line method. Depreciation Expense 20Y5 $fill in the blank 1 20Y6 $fill in the blank 2 20Y7 $fill in the blank 3 20Y8 $fill in the blank 4 b. Determine the amount of depreciation expense for the years ended December 31, 20Y5, 20Y6, 20Y7 and 20Y8 by the double-declining-balance method. Round the double-declining-balance depreciation rate to six decimal places and round your final answers to the nearest whole dollar. Depreciation Expense 20Y5 $fill in the blank 5 20Y6 $fill in the blank 6 20Y7 $fill in the blank 7 20Y8 $fill in the blank 8arrow_forward

- Sale of Equipment Equipment was acquired at the beginning of the year at a cost of $587,500. The equipment was depreciated using the straight-line method based on an estimated useful life of 9 years and an estimated residual value of $47,305. a. What was the depreciation for the first year? Round your answer to the nearest cent. b. Using the rounded amount from Part a in your computation, determine the gain or loss on the sale of the equipment, assuming it was sold at the end of year eight for $100,097. Round your answer to the nearest cent. Enter your answer as a positive amount. Feedback c. Journalize the entry to record the sale. If an amount box does not require an entry, leave it blank. Round your answers to the nearest cent.arrow_forwardSale of Equipment Equipment was acquired at the beginning of the year at a cost of $587,500. The equipment was depreciated using the straight-line method based on an estimated useful life of 9 years and an estimated residual value of $41,420. a. What was the depreciation for the first year? Round your answer to the nearest cent. 2$ b. Using the rounded amount from Part a in your computation, determine the gain or loss on the sale of the equipment, assuming it was sold at the end of year eight for $97,086. Round your answer to the nearest cent. Enter your answer as a positive amount. c. Journalize the entry to record the sale. If an amount box does not require an entry, leave it blank. Round your answers to the nearest cent.arrow_forwardEquipment was acquired at the beginning of the year at a cost of $78,840. The equipment was depreciated using the straight-line method based upon an estimated useful life of 6 years and an estimated residual value of $7,860. a. What was the depreciation expense for the first year?$fill in the blank 4b6aeefb5057020_1 b. Assuming the equipment was sold at the end of the second year for $59,600, determine the gain or loss on sale of the equipment.$fill in the blank 4b6aeefb5057020_2 c. Journalize the entry to record the sale. If an amount box does not require an entry, leave it blank or enter "0". - Select - - Select - - Select - - Select - - Select - - Select - - Select - - Select -arrow_forward

- Willow Creek Company purchased and installed carpet in its new general offices on April 30 for a total cost of $18,000. The carpet is estimated to have a 15-year useful life and no residual value.a. Prepare the journal entry necessary for recording the purchase of the new carpet.b. Record the December 31 adjusting entry for the partial-year depreciation expense for the carpet, assuming that Willow Creek Company uses the straight-line method.arrow_forwardŠale of Equipment Equipment was acquired at the beginning of the year at a cost of $550,000. The equipment was depreciated using the straight-line method based on an estimated useful life of 9 years and an estimated residual value of $44,205. a. What was the depreciation for the first year? Round your answer to the nearest cent. b. Using the rounded amount from Part a in your computation, determine the gain or loss on the sale of the equipment, assuming it was sold at the end of year eight for $95,704. Round your answer to the nearest cent. Enter your answer as a positive amount. $ c. Journalize the entry to record the sale. If an amount box does not require an entry, leave it blank. Round your answers to the nearest cent.arrow_forwardTransactions for fixed assets, including sale depreciation is used. Year 1 January 8. Purchased a used delivery truck for $61, 440, paying cash. March 7. Paid garage $180 for changing the oil, replacing the oil filter, and tuning the engine on the delivery truck. December 31. Recorded depreciation on the truck for the fiscal year. The estimated useful life of the truck is 8 years, with a residual value of $12,900 for the truck. Year 2 January 9. Purchased a new truck for $70, 560, paying cash. February 28. Paid garage $260 to tune the engine and make other minor repairs on the used truck. April 30. Sold the used truck for $40, 440. (Record depreciation to date in Year 2 for the truck.) December 31. Record depreciation for the new truck. It has an estimated residual value of $12,700 and an estimated life of 7 years. Year 3 September 1. Purchased a new truck for $93, 000, paying cash. September 4. Sold the truck purchased January 9, Year 2, for $42,900. (Record depreciation to date for…arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education