ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

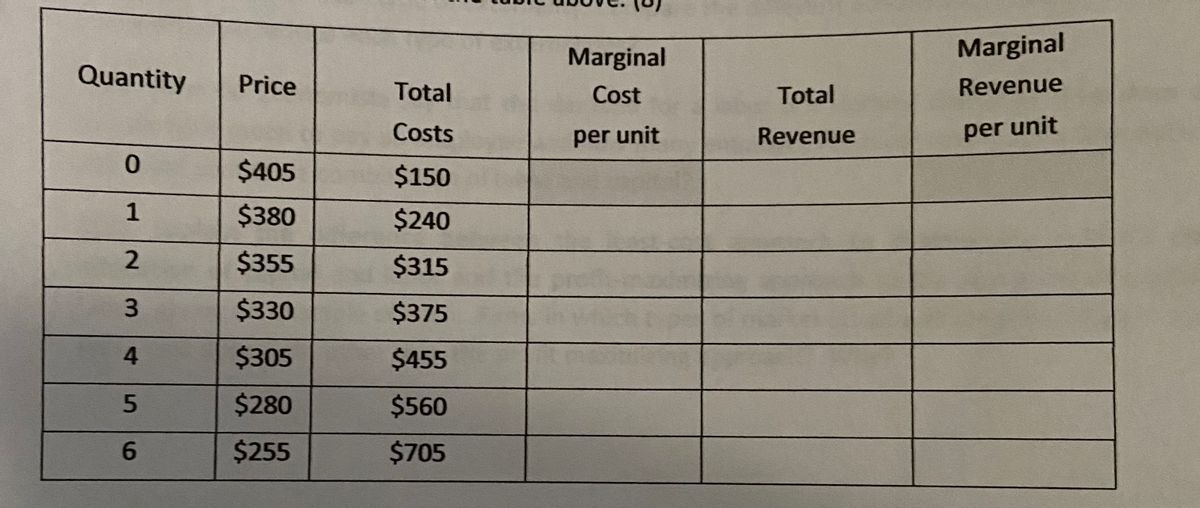

The table represents the demand (quantity at each

a. Based upon the data in your table, how many products will the firm produce and at what price will it sell it product to maximize profit? Will the firm make an economic profit? If so, how much?

b. In what type of market structure does this firm participate? How did you decide this?

Transcribed Image Text:Marginal

Marginal

Quantity

Price

Revenue

Total

Cost

Total

Costs

Revenue

per unit

per unit

$405

$150

1

$380

$240

2

$355

$315

3.

$330

$375

4.

$305

$455

5

$280

$560

6.

$255

$705

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 4 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Four Microeconomics Questions How to solve and answer these four questions?arrow_forwardcan anyone help me with my homework pleasearrow_forwardneed help with the graphs Note:- Do not provide handwritten solution. Maintain accuracy and quality in your answer. Take care of plagiarism. Answer completely. You will get up vote for sure.arrow_forward

- Assume that the plum market has lots of different farms. They are producing pretty much the same product. The plum market is very much like a perfectly competitive market. When answering this question, please use an explanation in words and the diagrams of the perfect competition model. A capitalist interested in the California plum market has asked you for an analysis. The capitalist comments, “I am guessing that plums are going to increase in popularity. What does that mean in the market?" Help this capitalist understand what might happen in this market given that plums will experience an increase in popularity. Please apply the perfect competition model. c. What happens to efficiency during these market changes? Please explain.arrow_forwardyou've been learning about what makes a market perfectly competitive, how a firm in a perfectly competitive market makes profit-maximizing decisions, and how a perfectly competitive market moves towards equilibirium. But how applicable is this to real life? For this discussion, try to think of a market (for a product or service) that is perfectly competitive or very close to it. What characteristics of the market make it like perfect competition? Are there factors that keep it from being perfectly competitive? If so, what are they? How close do you think the firms in this market are to perfectly competitive firms in choosing equilibrium price and quantity?arrow_forwardQuestion:Imagine that you set up your own business. Assume that your firm produces a single product. Please discuss in detail whether the market for your product satisfies the basic assumptions of perfectly competitive markets one by one.arrow_forward

- Identify an industry that enjoys perfect (or nearly perfect) competition. How do the competitors interact with each other and suppliers and customers?arrow_forwardYou read in a business magazine that farmers are reaping high profits. With the theory of perfect competition in mind, what do you expect to happen over time (in the long run) to each of the following? The profits of farmers based on what happens to the price, what do you think will happen to the profits earned by the firms/farmers that previously existed in the market?arrow_forwardCan you think of a product that meets at least most of the criteria required for a perfectly competitive market? Which criteria does it fail to meet?arrow_forward

- 1. Why is water, which is essential to life, so cheap, while diamonds, which are not essential to life, so expensive? Explain your answer using total utility (TU) and marginal utility (MU). 2. Discuss the advantages of perfect competition. 3. What is the shape and elasticity of the demand curve facing a perfectly competitive firm? Why? 4. How does the firm determine how much to produce in the short run?arrow_forward1. Suppose you are the owner of a burger restaurant that has a cost of production given by C = 400 + 0.02q^2 where q is the number of burgers produced per day. Assume that the market for burgers is perfectly competitive. a. If the market price for a burger is $10, how many burgers should the manager plan to produce in a day? b. What is the profit level? Is this the maximum profit that the restaurant can make per day? c. What output will the firm produce if the price of a burger goes down to $8?arrow_forwardYour uncle has just purchased a wheat farm and wants your advice on how he should price his product. Explain to your uncle the characteristics of the market structure under which his farm falls and how this will help him to determine the price and quantity of the wheat he will produce.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education