ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

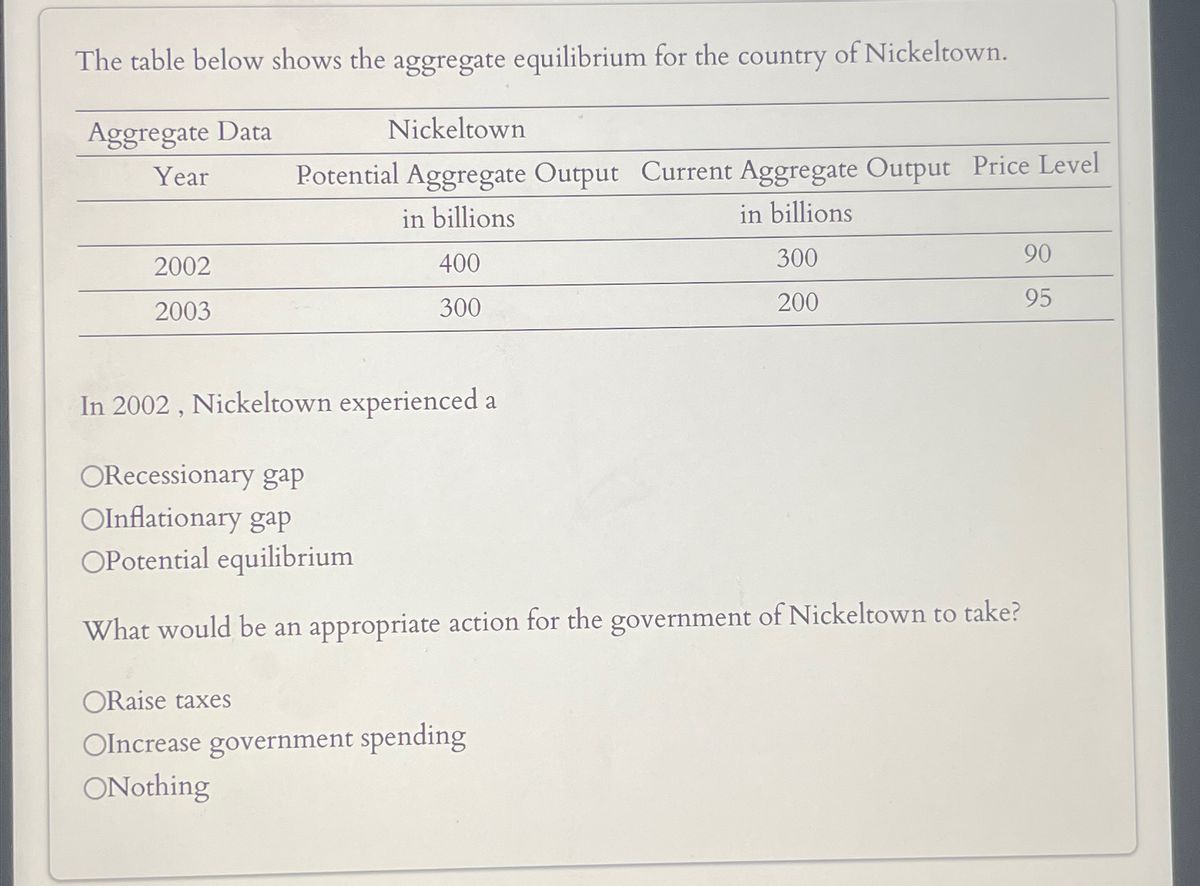

Transcribed Image Text:The table below shows the aggregate equilibrium for the country of Nickeltown.

Aggregate Data

Year

Nickeltown

Potential Aggregate Output Current Aggregate Output Price Level

2002

2003

in billions

400

300

In 2002, Nickeltown experienced a

ORecessionary gap

OInflationary gap

in billions

300

90

200

95

OPotential equilibrium

What would be an appropriate action for the government of Nickeltown to take?

ORaise taxes

OIncrease government spending

ONothing

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 4 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- The economy is in long run equilibrium. Congress’s passage of new laws significantly increasing the regulation of business. It is assumed that everything else stays constant. What do we expect in aggregate demand, short run aggregate supply aggregate supply in short run? And what happens in long run, and long run equilibrium price level and output? Explicitly state what happens to equilibrium price level and output in both short run and long run and how economy corrects from short run to long run.arrow_forward2arrow_forwardPlease no written by hand solution Assume that the potential GDP of the economy of Arion is $1,160, and that the aggregate demand and aggregate supply are as shown in the following table. Aggregate Quantity Demanded 1 Aggregate Quantity Demanded 2 Price Index Aggregate Quantity Supplied $1,240 96 $1,000 1,220 97 1,040 1,200 98 1,080 1,180 99 1,120 1,160 100 1,160 1,140 101 1,200 1,120 102 1,240 1,100 103 1,270 1,080 104 1,300 1,060 105 1,330 a. The value of equilibrium real GDP is and the price level is . There is (Click to select) gap. The gap is equal to $ . b. If firms become more optimistic and aggregate demand increases by $60, complete the aggregate demand 2 column in the table above. c. The new value of equilibrium real GDP is and the price level is now . d. There is (Click to select) gap. The gap is equal to $ .arrow_forward

- Price Level 0 AS₁ a ASO b c Real GDP Refer to the figure above. If aggregate supply is AS, and aggregate demand is ADo, then: a surplus of real output of gh yould f represents a price level that would result in a surplus of real output of ac f represents a price level that would result in a shortage of real output of ac f represents a price level that would result in a surplus of real output of a at any price level above g. a shortage of real output would occur occurarrow_forwardPossitive short run relatioship between the prices level for outpput and reall gdp holding the prices of inputs fexed a- longo-run aggregate supply SRAS curve b- long run aggregate demand SRAS curve c- short eun aggregate supply SRAS curve d- short-run aggregate demand SRAS curvearrow_forwardWhich of the following would shift long-run aggregate supply to the right? a. increased immigration from abroad Ob. a decrease in the price of an imported natural resource C. opening the economy to international trade Od. All of the above are correct.arrow_forward

- 5) Compare and contrast how the UK macroeconomy and its policymakers responded to sharp increases in the price of oil in the early 1970s and 2022/3.arrow_forwardexplain the likely effects of U.S boom on the demand for canadian exports.what woukd be the effect of canadian aggregate demand?suppose the bank of canada viewed its monetary policy as being appropriate for keeping gdp of canada close to potential gdp . what would you hen predict to be the central bank's response to foriegn boom in U.Sarrow_forwardRefer to the figure to answer two questions. Price Level (average price) PE E a. How much output is unsold at the price level P₁? OD-S OS-QE 05-D₁ OQE-Di OP₁ b. At what price level is all output produced sold? OP₁-PE O PE+ P1 OPE Aggregate supply D₁ QE S₁ Real Output (quantity per year) Aggregate demandarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education