ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

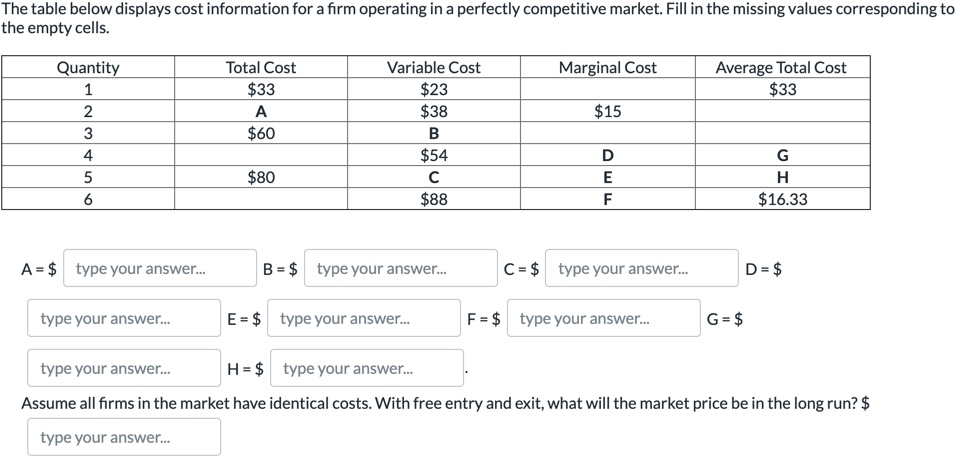

Transcribed Image Text:The table below displays cost information for a firm operating in a perfectly competitive market. Fill in the missing values corresponding to

the empty cells.

Average Total Cost

$33

Quantity

Total Cost

Variable Cost

Marginal Cost

1

$33

$23

A

$38

$15

3

$60

В

4

$54

D

G

$80

H

6

$88

F

$16.33

A = $

type your answer..

B = $

type your answer..

C= $ type your answer.

D = $

type your answer..

E = $ type your answer...

F = $ type your answer.

G = $

type your answer.

H = $ type your answer..

Assume all firms in the market have identical costs. With free entry and exit, what will the market price be in the long run? $

type your answer.

Expert Solution

arrow_forward

Step 1

A perfectly competitive market is the market with large number of buyers and sellers, selling homogeneous goods and services at the price given by the industry.

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Please fill out this table!arrow_forwardPQ 14.05 Reagan is a farmer and sells her wheat in a perfectly competitive market. Reagan produces 30,000 bushels of wheat for an average total cost of $7.50, marginal cost of $7.30, and average variable cost of $7.10. In the short-run, Reagan should produce more wheat if the current price is above, and should shut down if the current price is below Select an answer and submit. For keyboard navigation, use the up/down arrow keys to select an answer. a $7.50; $7.30 $7.50; $7.10 $7.10; $7.30 $7.10; $7.00 e $7.30; $7.10 f $7.30; $7.00arrow_forwardA profit-maximizing firm in a competitive market is currently producing 500 units of output. It has average revenue of $10, average total cost of $8, and fixed costs of $200. a. What is its profit? b. What is its marginal cost? c. What is its average variable cost? d. Is the efficient scale of the firm more than, less than, or exactly 100 units?arrow_forward

- Consider the perfectly competitive market for sports jackets. The following graph shows the marginal cost ( MCMC ), average total cost ( ATCATC ), and average variable cost ( AVCAVC ) curves for a typical firm in the industry.arrow_forwardThinking on the Margin to Increase Profitability Have you ever walked into a restaurant for lunch and found it almost empty? Why, you might ask, does the restaurant even bother to stay open? It might seem that the revenue from so few customers could possible cover the cost of running the restaurant. Provide an opinion using the concepts of sunk costs, marginal cost and marginal revenue.arrow_forwardFirms in the market for dog food are selling in a purely competitive market. A firm producing dog food has an output of 10,000 pounds of dog food, for which it sells for $0.50 a pound. At the output level of 10,000 pounds the average variable cost is $0.40, the average total cost is $0.70, and the marginal cost is $0.50. What do expect will happen in the long-run? Explain.arrow_forward

- Question 5.5 T-Shirt Enterprises is selling in a purely competitive market. It is producing 3,000 units, selling them for $2 each. At this level of output, the average total cost is $2.50 and the average variable cost is $2.20. Based on these data, the firm should shut down in the short run. decrease output to 2,500 units. ontinue to produce 3,000 units. increase output to 3,500 units.arrow_forwardGiven the following Information about a competitive firm's costs, calculate marginal cost and then answer three questions. Instructions: Enter your responses as a whole number. If you are entering any negative numbers be sure to include a negative sign (-) In front of those numbers. Output (Units) Total Cost Marginal Cost 10 $50 11 52 $ 2 12 56 $ 4 13 62 $ 6 14 70 $ 8 15 80 $ 10 16 92 $ 12 17 106 $ 14 18 122 $ 16 19 140 $ 18 a. If the prevailing market price is $12 per unit, how much should the firm produce? 16 units b. How much profit will it earn at that output rate? 100 c. If the firm Increases output by 1 unit, the firm will make more profit.arrow_forwardA firm has fixed costs of $40 and variable costs as indicated in the table below. For each level of output (total product) calculate total cost, average fixed cost, average variable cost, average total cost and marginal cost. Write your response in the table provided. b) Discuss why a firm in perfect competition will not charge a price above or below the market price.arrow_forward

- Given the table below for a firm operating in a perfectly competitive market, what is the short run fixed cost? Output 0 1 2 3 $20 $10 $12 Total Cost $10 $20 $28 $34 Cannot be determinedarrow_forwardProblems: Question #6: The Phantom Farms bakery produces pumpkin pies according to the following short run cost schedules. Assume the pumpkin pie industry is perfectly competitive and that the bakery can only produce and sell whole pies. AVC = ATC = MC = Quantity (pies) TFC = total TVC = total TC = total fixed cost variable cost average average total marginal cost variable cost cost cost (i) same as (i) 1 14 18 14.0 18 14 2 same as (i) (ii) 28 12.0 14 10 3 same as (i) 38 42 12.7 (v) 14 4 same as (i) 60 (iii) 15.0 16 22 same as (i) 86 90 17.2 18 (vi) same as (i) 116 120 (iv) 20 30 Fill in the five missing cost numbers indicated in the table above. (i) (ii) (iii) (iv) (v) (vi) If the price of pumpkin pies is $22 per pie, how many pies should Phantom Farms produce in the short run? What profit or loss does the firm earn? Explain how you arrived at this answer. Illustrate Phantom Farms' choice with a graph and indicate profits or losses. 3arrow_forwardThe following cost data is for a firm which is selling in a perfectly competitive market: Average fixed Average variable Average total Total Marginal cost S17 product cost S100.00 50.00 33.33 25.00 20.00 cost $17.00 cost $117.00 66.00 47.33 39.25 34.00 2 16.00 15 3 4 15.00 14.25 14.00 14.00 15.71 17.50 13 12 13 16.67 14.29 12.50 11.11 10.00 9.09 7.33 30.67 30.00 14 26 30 35 7 8. 9. 10 11 30.00 30.55 31.60 33.09 35.00 19.44 21.60 41 24.00 48 12 26.67 56 Refer to the data above. If there were 600 identical firms in this industry and total or market demand is as shown below, equilibrium price will be: Quantity demanded 3,000 6,000 9,000 11,000 14,000 19,500 Price $50 42 36 32 20 13 $36arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education