ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

18....

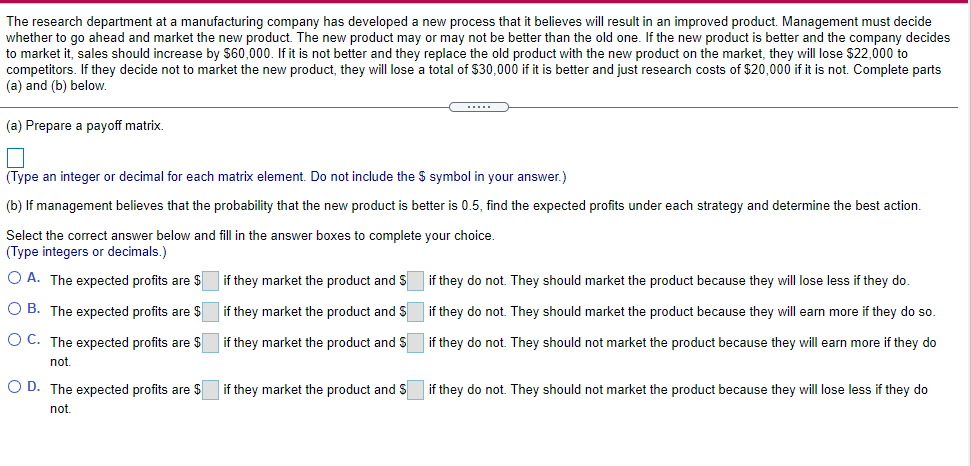

Transcribed Image Text:The research department at a manufacturing company has developed a new process that it believes will result in an improved product. Management must decide

whether to go ahead and market the new product. The new product may or may not be better than the old one. If the new product is better and the company decides

to market it, sales should increase by $60,000. If it is not better and they replace the old product with the new product on the market, they will lose $22,000 to

competitors. If they decide not to market the new product, they will lose a total of $30,000 if it is better and just research costs of $20,000 if it is not. Complete parts

(a) and (b) below.

(a) Prepare a payoff matrix.

(Type an integer or decimal for each matrix element. Do not include the $ symbol in your answer.)

(b) lf management believes that the probability that the new product is better is 0.5, find the expected profits under each strategy and determine the best action.

Select the correct answer below and fill in the answer boxes to complete your choice.

(Type integers or decimals.)

O A. The expected profits are $

if they market the product and S

if they do not. They should market the product because they will lose less if they do.

O B. The expected profits are $

if they market the product and S

if they do not. They should market the product because they will earn more if they do so.

O C. The expected profits are $ if they market the product and S

if they do not. They should not market the product because they will earn more if they do

not.

O D. The expected profits are $ if they market the product and S

if they do not. They should not market the product because they will lose less if they do

not.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- 9arrow_forward1. Years ago, an apple producer argued that the United States should enact a tariff, or a tax, on imports of bananas. His reasoning was that “the enormous imports of cheap bananas into the United States tend to curtail the domes-tic consumption of fresh fruits produced in the United States.”. a. Was the apple producer assuming that apples and bananas are substitutes or complements? Briefly explain. b. If a tariff on bananas acts as an increase in the cost of supplying bananas in the United States, use two demand and supply graphs to show the effects of the apple producer’s proposal. One graph should show the effect on the banana market in the United States, and the other graph should show the effect on the apple market in the United States. Be sure to label the change in equilibrium price and quantity in each market and any shifts in the demand and supply curves.arrow_forwardDollars 9 490 MC ATC 9 MR Output h] Refer to the diagram. Equilibrium price is Mutiple Choicearrow_forward

- Sapling Learning macmillan learning Suppose that the graph below illustrates the market demand for burgers per month with an equilibrium price of $3.00 and equilibrium quantity of 4 thousand burgers. Please indicate on the graph the effects of excess inventories that lowers the price by $2, place point A at the new equilibrium, and then answer the question. 6 Price (S) 5 A 3.0 3 2 1 0 0 1 2 A Demand 3 4 4.0 Quantity (thousands) 5 6 7 8 Map What is the new quantity of burgers demanded? Enter your answer in thousands, and specify to one decimal place. Number 0 thousandarrow_forwardExplain: “The success of a new product depends not only on its marginal utility but also on its price.”arrow_forwardGive correct typing answer with explanationarrow_forward

- Solve D) and E) Only typed answerarrow_forwardQuantity per unit of time C Quantity per unit of time Refer to the graph above. Assume the graph reflects demand in the automobile market. Which arrow best captures the impact of increased prices of automobiles on the automobile market? OA. A OB, B C.C D. Darrow_forward15. Consider Graphs |-V. (See supplementary graphs.) Which graph represents going from a positive fare to a zero fare? Graph I Graph II Graph II a. b. C.arrow_forward

- pls, solve this ques within 10-15 minutes with clear explanations and also explain why other options are wrong I'll give you multiple upvotes.arrow_forward11:40 AM Mon 22 Mar @ 56% McGraw-Hill ConnectEd Close Mc Graw Hill Education Microeconomics - Gr.10 - VA- Minitest 1 - 2nd T... I Hind Saeed Question 12 Section 1: 12/30 What would be a good synonym for "equilibrium" in the term “equilibrium price"? Explain your choice. 200 words remaining Save & Continue »arrow_forwardWhat is the relationship between supply anddemand when a market is in equilibrium? Explainhow the incentives facing cell phone companiesand consumers cause the market for cell phones toreach equilibriumarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education