MATLAB: An Introduction with Applications

6th Edition

ISBN: 9781119256830

Author: Amos Gilat

Publisher: John Wiley & Sons Inc

expand_more

expand_more

format_list_bulleted

Related questions

Question

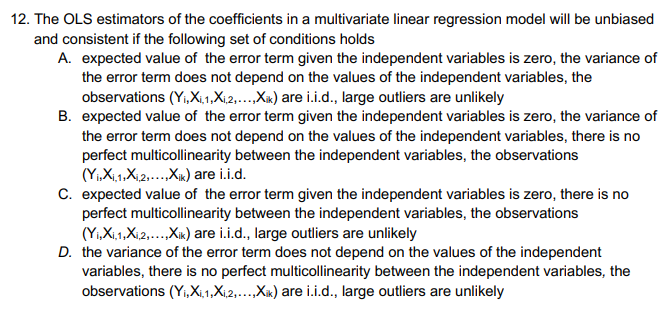

Transcribed Image Text:12. The OLS estimators of the coefficients in a multivariate linear regression model will be unbiased

and consistent if the following set of conditions holds

A. expected value of the error term given the independent variables is zero, the variance of

the error term does not depend on the values of the independent variables, the

observations (Yi,Xi,1,X₁,2,...,Xik) are i.i.d., large outliers are unlikely

B. expected value of the error term given the independent variables is zero, the variance of

the error term does not depend on the values of the independent variables, there is no

perfect multicollinearity between the independent variables, the observations

(Y₁X₁,1X₁,2,...,Xik) are i.i.d.

C. expected value of the error term given the independent variables is zero, there is no

perfect multicollinearity between the independent variables, the observations

(Yi,Xi,1,Xi,2,...,Xik) are i.i.d., large outliers are unlikely

D. the variance of the error term does not depend on the values of the independent

variables, there is no perfect multicollinearity between the independent variables, the

observations (Yi,X₁,1,X₁,2,...,Xik) are i.i.d., large outliers are unlikely

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps with 1 images

Knowledge Booster

Similar questions

- 19arrow_forwardA small independent organic food store offers a variety of specialty coffees. To determine whether price has an impact on sales, the managers kept track of how many kilograms of each variety of coffee were sold last month. The data and summary statistics (including the averages, standard deviations and the correlation coefficient) are shown in the table. If the "price per kilogram" is the predictor variable and "kilograms sold" is the response variable, then use a regression line to predict the the amount of kilograms sold for a "price per kilogram" equal to $15. Round your numbers to 3 decimal places.arrow_forwardThis table reports the regression coefficients when the returns of the size-institutionalownership portfolio (columns 1 and 2) returns are regressed on three variables: a constant(column 3), the stock market returns (column 4), and the change of the value weighted discountof the closed end fund industry (column 6). Columns 5 and 7 report the corresponding t-statistics of the coefficient estimates. Note that a t-statistic with an absolute value above 1.96means the coefficient estimate is significantly different from 0 at the 1% level. Column 8reports the R square of the regressions. Column 9 reports the mean institutional ownership ofeach portfolio. The last column reports the F-statistics for a multivariate test of the null hypothesis that the coefficient on ΔVWD in the Low (L) ownership portfolio is equal to theHigh (H) ownership portfolio. Two-tailed p-values are in parentheses. 1. What is the main finding of this Table? 2. What is the explanation for…arrow_forward

- Select all statements that are true of the least-squares regression line. ) It assumes a linear relationship between the explanatory and the response variable. R-squared is the portion of sample variance in the explanatory variable that can be explained by variation in the response variable. ) It can be used to predict the mean response of the explanatory variable. | R-squared is the portion of sample variance in the y variable that can be explained by variation in the x variable.arrow_forwardA group of Maternal and Child Health public health practitioners are interested in the relationship between depression and a number of health outcomes. Suppose the research team gathers information on a group of participants, and constructs a multiple linear regression model looking at the relationship between depression and household income dichotomized as above and below the federal poverty line controlling for a number of potential confounders. The following is a computerized output displaying the results of their analysis. Parameter Estimate Standard Error t Value Pr > |t| Intercept 0.2617346843 0.09209917 2.84 0.0046 Income (1/0) -.1962038300 0.04574793 -4.29 <.0001 Race (W or AA) -.0320329506 0.03900447 -0.82 0.4118 bmicontinuous 0.0051185980 0.00216986 2.36 0.0186 Alcohol (Y/N) -.0088735044 0.03090631 -0.29 0.7741 A) What are the independent and dependent variables? B) Which potential…arrow_forwardSuppose that Y is normal and we have three explanatory unknowns which are also normal, and we have an independent random sample of 21 members of the population, where for each member, the value of Y as well as the values of the three explanatory unknowns were observed. The data is entered into a computer using linear regression software and the output summary tells us that R-square is 0.9, the linear model coefficient of the first explanatory unknown is 7 with standard error estimate 2.5, the coefficient for the second explanatory unknown is 11 with standard error 2, and the coefficient for the third explanatory unknown is 15 with standard error 4. The regression intercept is reported as 28. The sum of squares in regression (SSR) is reported as 90000 and the sum of squared errors (SSE) is 10000. From this information, what is the number of degrees of freedom for the t-distribution used to compute critical values for hypothesis tests and confidence intervals for the individual model…arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- MATLAB: An Introduction with ApplicationsStatisticsISBN:9781119256830Author:Amos GilatPublisher:John Wiley & Sons Inc

Probability and Statistics for Engineering and th...StatisticsISBN:9781305251809Author:Jay L. DevorePublisher:Cengage Learning

Probability and Statistics for Engineering and th...StatisticsISBN:9781305251809Author:Jay L. DevorePublisher:Cengage Learning Statistics for The Behavioral Sciences (MindTap C...StatisticsISBN:9781305504912Author:Frederick J Gravetter, Larry B. WallnauPublisher:Cengage Learning

Statistics for The Behavioral Sciences (MindTap C...StatisticsISBN:9781305504912Author:Frederick J Gravetter, Larry B. WallnauPublisher:Cengage Learning  Elementary Statistics: Picturing the World (7th E...StatisticsISBN:9780134683416Author:Ron Larson, Betsy FarberPublisher:PEARSON

Elementary Statistics: Picturing the World (7th E...StatisticsISBN:9780134683416Author:Ron Larson, Betsy FarberPublisher:PEARSON The Basic Practice of StatisticsStatisticsISBN:9781319042578Author:David S. Moore, William I. Notz, Michael A. FlignerPublisher:W. H. Freeman

The Basic Practice of StatisticsStatisticsISBN:9781319042578Author:David S. Moore, William I. Notz, Michael A. FlignerPublisher:W. H. Freeman Introduction to the Practice of StatisticsStatisticsISBN:9781319013387Author:David S. Moore, George P. McCabe, Bruce A. CraigPublisher:W. H. Freeman

Introduction to the Practice of StatisticsStatisticsISBN:9781319013387Author:David S. Moore, George P. McCabe, Bruce A. CraigPublisher:W. H. Freeman

MATLAB: An Introduction with Applications

Statistics

ISBN:9781119256830

Author:Amos Gilat

Publisher:John Wiley & Sons Inc

Probability and Statistics for Engineering and th...

Statistics

ISBN:9781305251809

Author:Jay L. Devore

Publisher:Cengage Learning

Statistics for The Behavioral Sciences (MindTap C...

Statistics

ISBN:9781305504912

Author:Frederick J Gravetter, Larry B. Wallnau

Publisher:Cengage Learning

Elementary Statistics: Picturing the World (7th E...

Statistics

ISBN:9780134683416

Author:Ron Larson, Betsy Farber

Publisher:PEARSON

The Basic Practice of Statistics

Statistics

ISBN:9781319042578

Author:David S. Moore, William I. Notz, Michael A. Fligner

Publisher:W. H. Freeman

Introduction to the Practice of Statistics

Statistics

ISBN:9781319013387

Author:David S. Moore, George P. McCabe, Bruce A. Craig

Publisher:W. H. Freeman