ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

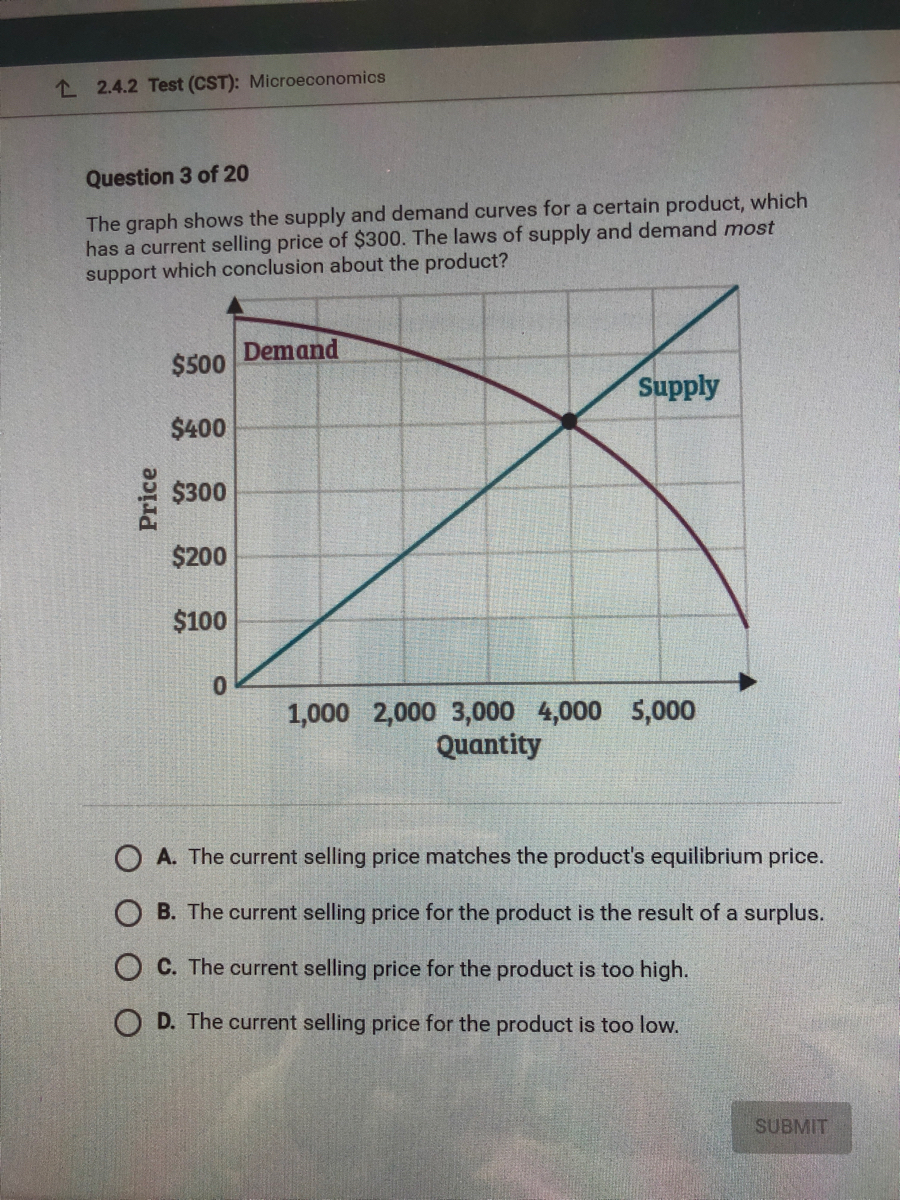

the graph shows the supply and demand curves for a certain product, which has a current selling price of $300. The laws of supply and demand most support which conclusion about the product?

Transcribed Image Text:### Microeconomics: Supply and Demand Analysis

**Question 3 of 20**

The graph below illustrates the supply and demand curves for a specific product with a current selling price of $300.

#### Graph Explanation:

- **Axes**:

- The vertical axis (Y-axis) represents the price of the product in dollars, ranging from $0 to $500.

- The horizontal axis (X-axis) represents the quantity of the product, ranging from 0 to 5,000 units.

- **Curves**:

- The **Demand Curve** (in red) slopes downward from left to right, indicating that as the price decreases, the quantity demanded increases.

- The **Supply Curve** (in blue) slopes upward from left to right, indicating that as the price increases, the quantity supplied increases.

- **Equilibrium Point**:

- The intersection of the supply and demand curves represents the equilibrium price and quantity, which appears to be at approximately $400 and 3,000 units.

#### Question:

The laws of supply and demand most support which conclusion about the product, given its current selling price of $300?

#### Options:

- **A.** The current selling price matches the product's equilibrium price.

- **B.** The current selling price for the product is the result of a surplus.

- **C.** The current selling price for the product is too high.

- **D.** The current selling price for the product is too low.

**Note:** The correct answer choice can be determined based on the relationship between the current price and the equilibrium point on the graph.

#### Conclusion:

To make an informed conclusion, examine where the current price of $300 falls on the graph relative to the equilibrium point at $400. If the current price is lower than the equilibrium price, it suggests a shortage. If higher, it indicates a surplus.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Consider two markets: the market for motorcycles and the market for pancakes. The initial equilibrium for both markets is the same, the equilibrium price is $4.50, and the equilibrium quantity is 29.0. When the price is $7.75, the quantity supplied of motorcycles is 65.0 and the quantity supplied of pancakes is 103.0. For simplicity of analysis, the demand for both goods is the same. Using the midpoint formula, calculate the elasticity of supply for pancakes. Please round to two decimal places.arrow_forwardDemand for Martha’s Mums will be 650 small mum plants if they are priced at $4.25 each but only 150 if they are priced at $10.75 each. a. Find the linear demand equation for Martha’s small mums (let x = number of small mum plants supplied, y = price). b. At what price will the demand for Martha’s mums drop to zero? c. What will be the demand for Martha’s mums if they are free? (Round to the nearest whole number).arrow_forwardWrite down the factors affecting demand. Which of the following factors will cause the following products to increase or decrease? Convenience food (sold in food shops and supermarkets) Products purchased in the internet Mobile phones Pay-per - view- television programming Books Airline travel within Us; air travel with UKarrow_forward

- Suppose that improved technology lowers the cost of manufacturing skis. What effect would this have in the market for skis?arrow_forwardSuppose that the price of product A increases from $10 to $19. As a result, quantity demanded for product B changes from 300 to 265. What can we say about products A and B? Explain?arrow_forwardConsider the supplier of a product that is an inferior good. For instance, an aluminum supplier for a canned goods producer. During a recession during which average incomes fall, which of the following best describes what would happen to the profit-maximizing price of the supplier? a. The supplier’s profit-maximizing price would decrease due to an increase in demand. b. The supplier’s profit-maximizing price would increase due to an increase in demand. c. The supplier’s profit-maximizing price would decrease due to a reduction in demand. d. The supplier’s profit-maximizing price would increase due to a reduction in demand.arrow_forward

- Which of the following is one of the factors determining if demand for a good is price elastic or price inelastic? Select one: a. The cost of the resources used in producing the good. b. The relative share of the budget spent on the good. c. Whether the good is a substitute or a complement. d. Whether the good is imported or exported.arrow_forwardIn the graph, a decrease in the price of the item will cause the movement from (select all that apply): Price Old supply New supply H K Quantity point M to point G point G to point L point M to point K point J to point M point L to point K point H to point Garrow_forwardWhy do demand curves slope down (i.e., sales volume usually rises at lower prices)?arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education