ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

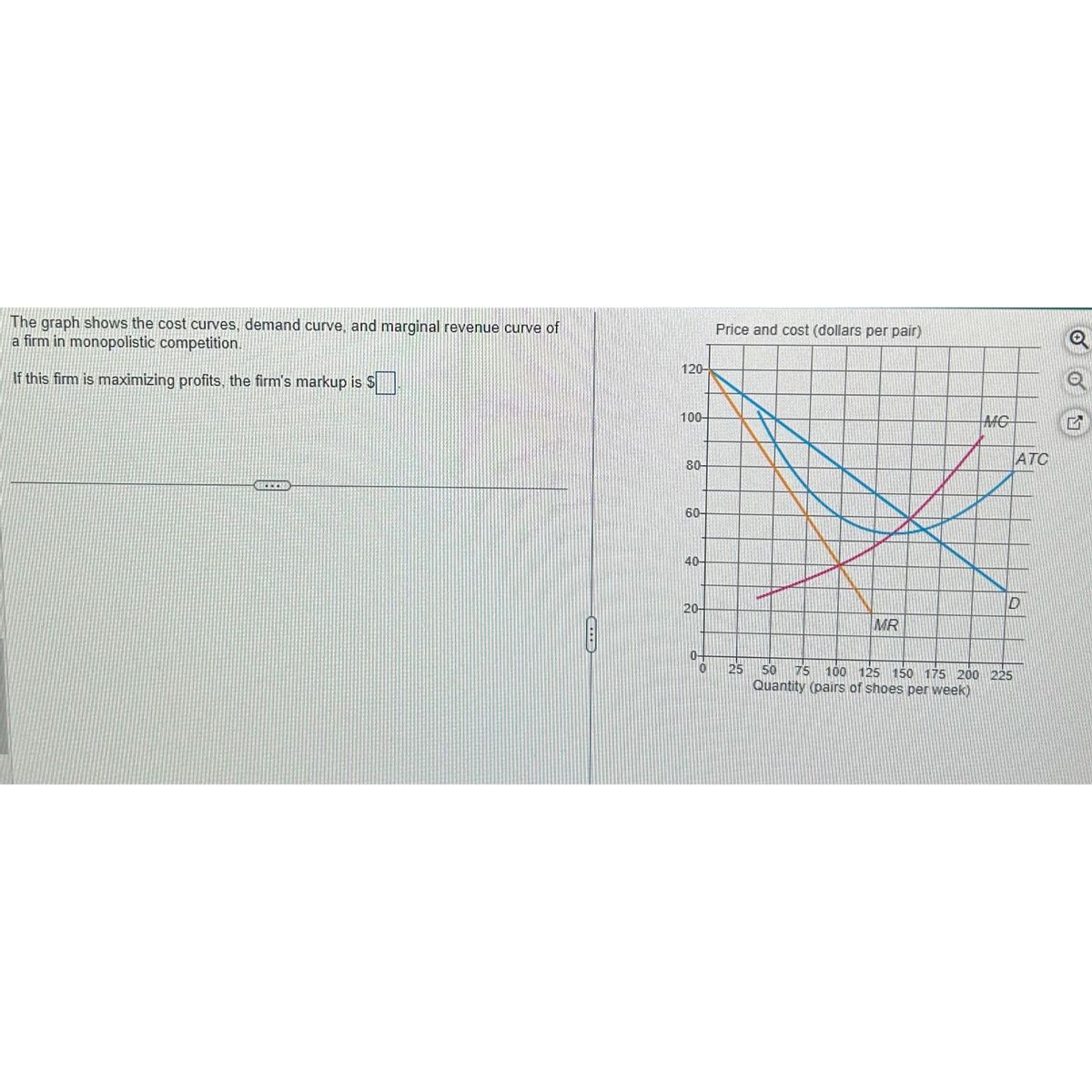

Transcribed Image Text:The graph shows the cost curves, demand curve, and marginal revenue curve of

a firm in monopolistic competition.

If this firm is maximizing profits, the firm's markup is $

S

ALECK

120-

100-

80-

60-

40-

20-

0

Price and cost (dollars per pair)

25

MR

ATC

D

50

100 125 150 175 200 225

Quantity (pairs of shoes per week)

75 100 12

SAVE

AI-Generated Solution

info

AI-generated content may present inaccurate or offensive content that does not represent bartleby’s views.

Unlock instant AI solutions

Tap the button

to generate a solution

to generate a solution

Click the button to generate

a solution

a solution

Knowledge Booster

Similar questions

- Assuming that the monopolistic competitor faces the demand and costs depicted below and finds the profit maximizing level of output, what will be the firm's revenue? 45 40 35 30 25 20 15 10 5 Select one: a. $64 b. $80 c. $120 MC1 d. $0 because the firm will shut down ATC₁ AVC1 MR1 D₁ 1 2 3 4 5 6 7 8 9 хоarrow_forwardSuppose the figure to the right shows the demand curve for a monopolistically competitive firm. Show the firm's marginal revenue curve. 20- 18- Using the line drawing tool, graph the firm's marginal revenue curve. Label this curve "MR." 16- Carefully follow the instructions above, and only draw the required object. 14- E 12 10- 4- 12 16 20 24 28 32 36 40 Quantity Price (dollars per unit)arrow_forwardls uccess Tips ■ccess Tips NOUT Actumpto Koup the Highest/3 3. Is monopolistic competition efficient? Suppose that a firm produces baseball bats in a monopolistically competitive market. The following graph shows its demand curve, marginal revenue (MR) curve, marginal cost (MC) curve, and average total cost (ATC) curve. Place a black point (plus symbol) on the graph to indicate the long-run monopolistically competitive equilibrium price and quantity for this firm. Next, place a grey point (star symbol) to indicate the minimum average total cost the firm faces and the quantity associated with that cost. PRICE (Dollars par bat) 80 70 60 20 MO о о 10 20 40 ATC 60 QUANTITY (Thousands of bas) Demand Man Camp Outcome Min Unit Cost Because this market is a monopolistically competitive market, you can tell that it is in long-run equilibrium by the fact that optimal quantity. Furthermore, the quantity the firm produces in long-run equilibrium is average total cost. at the the quantity at which…arrow_forward

- Q28arrow_forwardΣ 00 Help The table below shows the total cost (TC) and marginal cost (MC) for Choco Lovers, a monopolistic firm producing different quantities of chocolate gift boxes. Fill in the blanks in the table. Total Quantity Price Total Cost Marginal Cost Marginal Revenue Revenue $20 $30 25 475 230 $8 540 267.5 7.5 13 35 17 307.5 11 40 45 640 352.5 6. 11 15 675 14 472.5 13 5. Instructions: Enter your answers as whole numbers. For profit, round your answer to 2 decimal places. Profit-maximizing quantity = %3D Profit-maximizing price = %3D Profit = %3D 2 68°F Mostly clear nere to search 直 0 L Profile Ball®1.0 F6 F5 F4 F2 F1 & V 24 4 23 5. 3. 2. T R B C. Altarrow_forwardPlease only Typing answer I need ASAParrow_forward

- I need both answers typing no chatgptarrow_forward3. A monopolistically competitive firm sells boots and has the following in the short run: Demand: P = 80 – 0.5Q %3D MR: MR = 80 – Q TC = 1.5Q? + 40 1.5Q + (40/Q) TC: АТC: MC: MC = 3Q %3D Find the firm's profit maximizing quantity and price. Find the firm's profit or loss. Show some work here: Quantity = Price = Profit or Loss = (circle one, and write the number)arrow_forwardMarkbury is a monopoly selling widgets. If the government imposes a $100 000 tax on every monopolistic firm in the country, then Select one: a. Markbury’s annual profit will no change since its marginal cost is unchanged b. Markbury’s annual profit will fall by $100 000 since its marginal cost would rise by $100 000 c. Markbury’s annual profit will fall by less than $100 000 since its marginal cost would rise by less than $100 000 d. Markbury’s annual profit will fall by $100 000 but its marginal cost will not change e. The impact on Markbury’s profit is difficult ascertain, without more informationarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education