ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

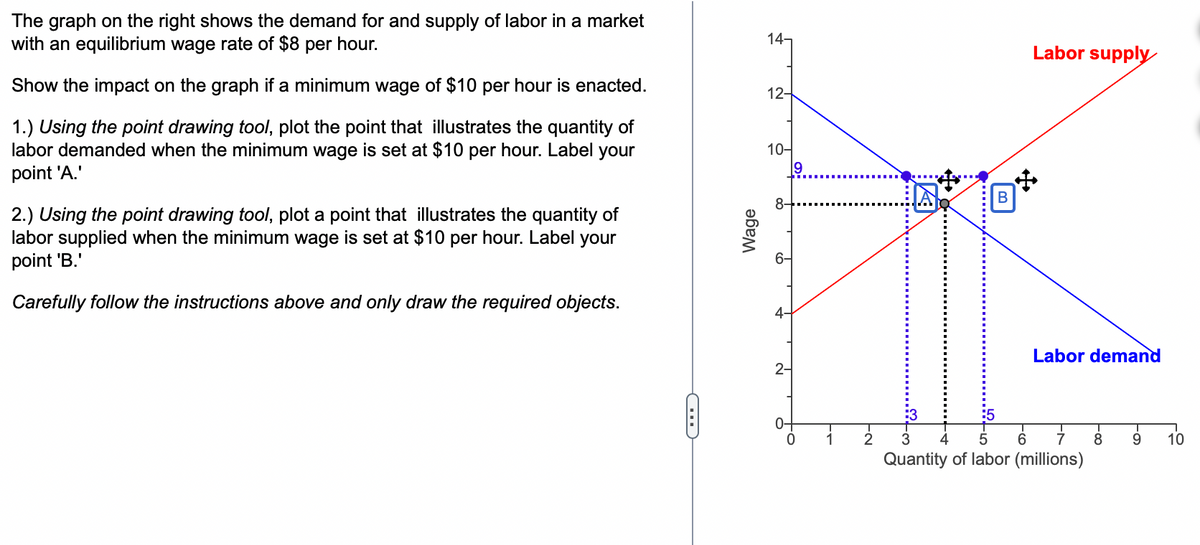

Transcribed Image Text:The graph on the right shows the demand for and supply of labor in a market

with an equilibrium wage rate of $8 per hour.

Show the impact on the graph if a minimum wage of $10 per hour is enacted.

1.) Using the point drawing tool, plot the point that illustrates the quantity of

labor demanded when the minimum wage is set at $10 per hour. Label your

point 'A.'

2.) Using the point drawing tool, plot a point that illustrates the quantity of

labor supplied when the minimum wage is set at $10 per hour. Label your

point 'B.'

Carefully follow the instructions above and only draw the required objects.

Wage

14-

12-

10-

8-

co

có

4.

2-

9

0

B

Labor supply

Labor demand

6

7

Quantity of labor (millions)

8 9

10

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- to finance a new health insurance program, the government of Millonia imposes a new $2-per-hour payroll tax to be paid by employers. What do you expect to happen to wages and the size of the workforce? Explain How will this answer change in markets where labor is inelastically demanded? Explainarrow_forwardGraph the original and new equilibrium. The pilot's union at all major air carriers has demanded and been granted a 20 percent pay increase. What will happen in the air travel market? How would this result differ if the demand for air travel was more elastic at the original equilibrium price?arrow_forwardConsider the Labor Market in New York and New Jersey. In both markets Demand is given by w = 1000-2E. Assume New York has a perfectly inelastic supply of 400 workers and New Jersey has perfectly inelastic supply of 200 workers. a. Graph the two markets and find the equilibrium wage in each market. b. With costless mobility across markets what would the long-run wage in each market. Show this in your graphs. c. Instead, assume that there are still 400 workers in New York and 200 in New Jersey but now the cost of moving is $ 100. What will be the long-run wage in each market? Explainarrow_forward

- draw a graph with this difinitions To visualize the impact of the minimum wage on the labor market, I have created an original graph (see below). This graph depicts a hypothetical labor market before and after an increase in the minimum wage. [Please insert your original graph here.] In the graph, the x-axis represents the quantity of labor, and the y-axis represents the wage rate. The blue curve (labeled "Initial Equilibrium") represents the initial labor market equilibrium, where the supply of labor (S) intersects with the demand for labor (D) at point A, determining the initial wage rate and employment level. The red curve (labeled "After Minimum Wage Increase") illustrates the impact of a minimum wage hike. When the government imposes a higher minimum wage, it acts as a price floor (represented by the horizontal line). This results in a new equilibrium at point B, where the wage rate is higher, but employment is lower compared to the initial equilibrium.arrow_forwardIn Tucson there are lots of bars and restaurants all of whom employ many workers. Wages for waitstaff are similar across most locations. What is the most appropriate market structure for the market for waitstaff in Tucson?arrow_forwardWhat are the pros and cons of increasing the minimum wagearrow_forward

- Island City is located on a small island, while Plains City is located at the center of a large, flat, featureless plain. Draw two labor-supply curves, one for each city. a. The supply curve for Island City is [steeper/flatter] because. . . . b. The elasticity of supply of labor in Island City is [higher, lower].arrow_forwardUsing an appropriate illustration explain the impact of the minimum wage in the labour marketarrow_forwardThe following graph shows the labor market for research assistants in the fictional country of Universalia. The equilibrium wage is $10 per hour, and the equilibrium number of research assistants is 250. Suppose the government has decided to institute a $4-per-hour payroll tax on research assistants and is trying to determine whether the tax should be levied on the employer, the workers, or both (such that half the tax is collected from each side). Use the graph input tool to evaluate these three proposals. Entering a number into the Tax Levied on Employers field (initially set at zero dollars per hour) shifts the demand curve down by the amount you enter, and entering a number into the Tax Levied on Workers field (initially set at zero dollars per hour) shifts the supply curve up by the amount you enter. To determine the before-tax wage for each tax proposal, adjust the amount in the Wage field until the quantity of labor supplied equals the quantity of labor demanded. You will not be…arrow_forward

- Explain the challenges of an increasing minimum wage for an economyarrow_forward$30 a week boost to minimum wage The government increased the minimum wage by $30 a week to $570 a week. Unions wanted a $35 a week increase, but employers argued that a $35 a week. increase was unaffordable. Source: ABC Australia, February 11, 2011 The graph shows a market for low-skilled labor. If the minimum wage is set at $570 a week, If the minimum wage is set at $540 a week, OA. some people who want a job can't get one; everyone who wants a job has one B. firms cannot hire all the labor they want; everyone who wants a job has one OC. everyone who wants a job has one; firms cannot hire all the labor they want OD. everyone who wants a job has one; some people who want a job can't get one 590- 580- 570- 560- 550 540- 530- 520- 510+ 9.8 Wage rate (dollars per week) A D 9.9 10.1 10 Quantity (millions of hours per year) S 10.2 Next Q Q Garrow_forwardWalmart employs the majority of people in small rural town. It's demand for labor is given by QD=100-2P. The supply of labor is given by Qs=3P. ✓ people would be If the labor market functioned as a competitive market, the wage rate (the price of labor) would be employed, and the producer surplus would be Because Walmart faces little competition for workers, it decides to offer the wage that maximizes consumer surplus (the monopsonist price). This wage is ✓being employed. The producer surplus is now ✓. Note: don't worry if the number of ✓, which results in workers is not an integer.arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education