ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

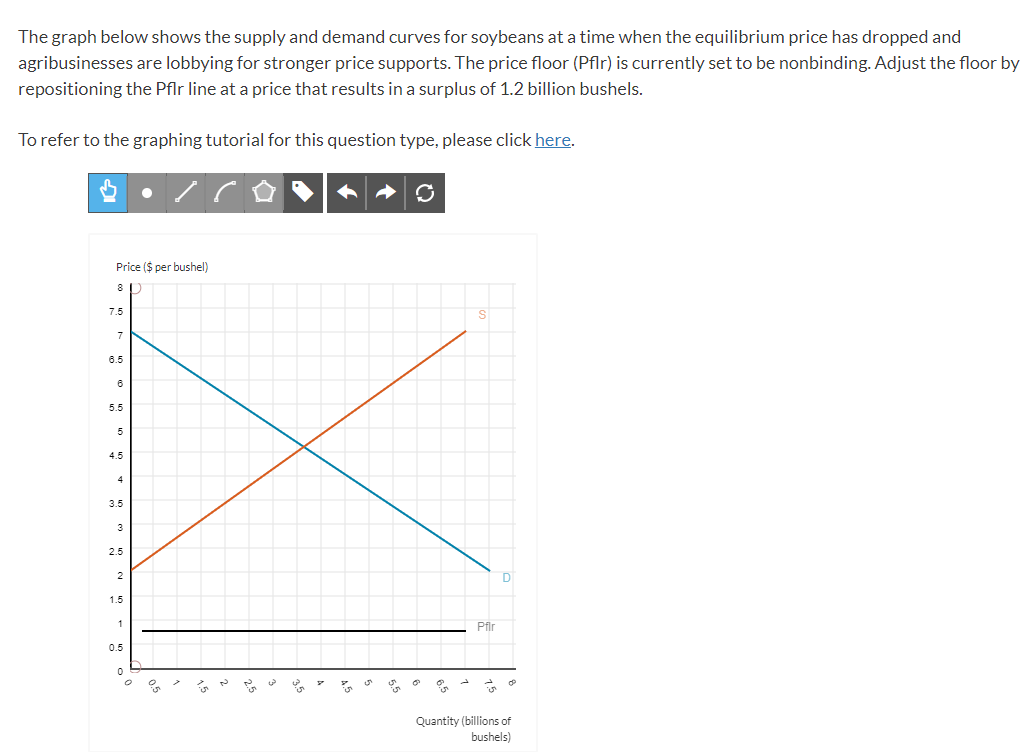

Transcribed Image Text:The graph below shows the supply and demand curves for soybeans at a time when the equilibrium price has dropped and

agribusinesses are lobbying for stronger price supports. The price floor (Pflr) is currently set to be nonbinding. Adjust the floor by

repositioning the Pflr line at a price that results in a surplus of 1.2 billion bushels.

To refer to the graphing tutorial for this question type, please click here.

Price ($ per bushel)

81

7.5

7

6.5

6

5.5

5

4.5

3.5

3

2.5

1.5

0.5

0

i

i

%

S

Pflr

In

D

OP

Quantity (billions of

bushels)

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Typed numeric answer will be automatically saved. Question 3 The inverse demand for push scooters: P = 900 -4Q The inverse supply for push scooters: P = 25+ 3Q What is the equilibrium price in this market? Draw the graph, if it helps. Typed numeric answer will be automatically saved. Knygaarrow_forwardThe market for cake is shown with the following supply and demand function. Demand: Q = 7500 - 500P Supply: Q = -500 + 500P The market price needs to be above ____ before firms would begin start producing cake.arrow_forwardIf the demand equation of a product is p= 210-g and the supply equation for a product is p= 29+2 then, the equilibrium price equalsarrow_forward

- At a price of $2:29 per bushel, the supply of a certain grain is 7500 million bushels and the demand is 7600 million bushels. At a price of $2.4 per bushel, the supply is 7000 million bushels and the demand is 7500 million bushels (A) Find a price-supply equation of the form p mxb, where p is the price in dollars and x is the supply in milions of bushels (B) Find a price-demand equation of the form p mx +b, where p is the price in dollars and x is the demand in millions of bushels (C)Find the equilibrium point (D) Graph the price-supply equation, price-demand equation, and equilibrium point in the same coordinate system. (A) The price-supply equation is p (Type an exact answer) -CTDarrow_forwardAn increase in technology with a simultaneous decrease in the number of buyers will cause the equilibrium price to fall and equilibrium quantity to be indeterminate. True Falsearrow_forwardMarket in equilibrium: consider a market for electric vehicles (EVS), where the equilibrium price (P*) is $30,000 per vehicle, and the equilibrium quantity (Q*) is 10,000 vehicles per year. draw the initial supply and demand graph. P qor Q Events: Due to advancements in battery technology, the cost of producing EVs decreases significantly. Additionally, governments around the world introduce stricter regulations on emissions from gasoline-powered vehicles, leading to an increased demand for EVs. Explain how both the supply and demand curves would be affected. Draw the new supply and demand curves on your graph (in red) and predict the changes in equilibrium price and quantity. Demand: Supply: +arrow_forward

- If E were the old equilibrium in the market for wheat in the figure below, and E' the new one, which of the following could have caused the change? E' (E D' D2 Consumer income rose, causing a supply shift. Bad weather caused a supply shift. Supply and demand both shifted. Consumer income rose, causing a demand shift. All of the above are plausible descriptions. а. b. c. d. e.arrow_forwardEstimate the equilibrium price. $ per pan. Round to the nearest dollar. Use the graph attached below to help answer the question i appreciate it thanks!!!!arrow_forwardMarket research has revealed the following information about the market for lamps: The demand schedule can be represented by the equation QD = 24 - 3P, where OD is the quantity demanded and P is the price. The supply schedule can be represented by the equation Os-4 + 2P, where Qs is the quantity supplied. (Show all your work). a) Sketch the demand and supply curves, carefully labeling your intercepts. b)Calculate the equilibrium price (P*) and quantity (Q*) in the market for lamps. c) If the market price was artificially set at P-$6, what kind of imbalance would this create in the market (surplus or shortage)? Of exactly how much? d) If the market price was artificially set at P-$2, what kind of imbalance would this create in the market (surplus or shortage)? Of exactly how much?arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education