ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

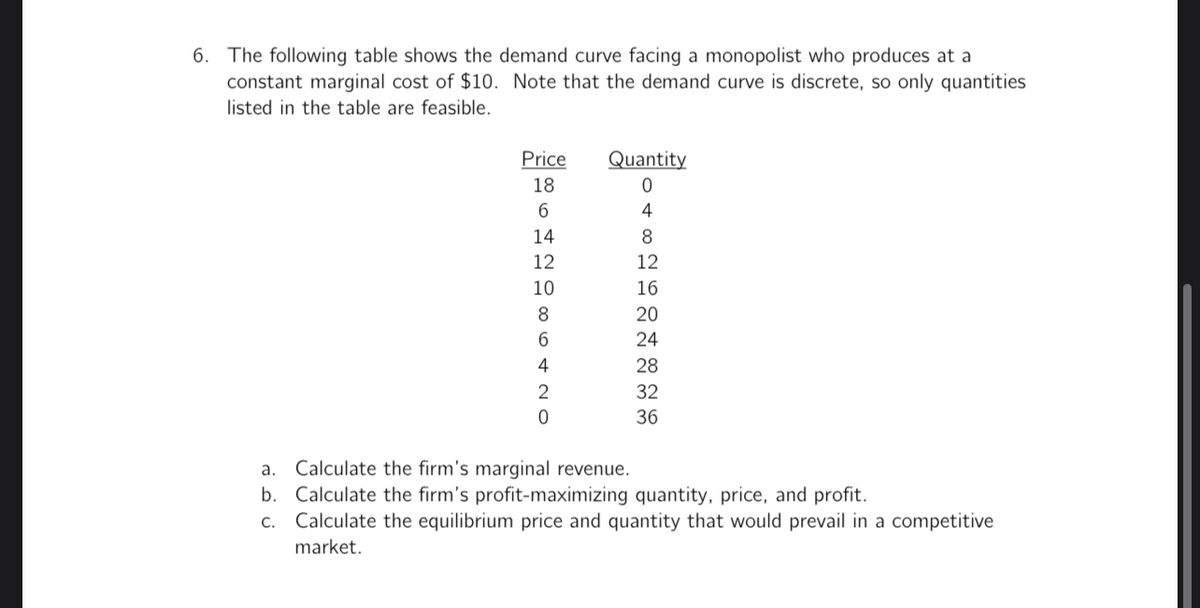

Transcribed Image Text:6. The following table shows the demand curve facing a monopolist who produces at a

constant marginal cost of $10. Note that the demand curve is discrete, so only quantities

listed in the table are feasible.

Price

18

6

14

12086420

Quantity

0

4

CONDH500+

12

16

20

24

28

32

36

a. Calculate the firm's marginal revenue.

b.

Calculate the firm's profit-maximizing quantity, price, and profit.

c. Calculate the equilibrium price and quantity that would prevail in a competitive

market.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 5 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Find the economic profit of a monopolist using the following information: Demand: p = 110-2Q Fixed cost: FC = 120 Marginal cost: MC = 10arrow_forwardThe accompanying graph depicts the marginal revenue (MR), demand (D), and marginal cost (MC) curves for a monopoly a. Place point Pi at the profit maximizing price and quantitvy assuming that the monopolist can only charge a single price. 100 95 90 85 80 75 70 65 2 60 b. What are the profits of the firm if it charges a single price? 50 45 Suppose the monopolist able to successfully price discriminate between two groups by charging one group $60 and charging $35 to the other group. c. What are the firm's profits if it charges the two prices as mentioned above? 35 30 25 20 15 10 MR 0 5 10 15 20 25 30 35 40 45 50 55 60 65 70 75 80 85 90 95100 Quantityarrow_forwardExplains it correctlyarrow_forward

- only question #4 pleasearrow_forwardWhich of the following is a common practice of single-price monopolists? * two-part tariffs advance purchase restrictions volume discounts differentiating customers based on their price elasticity of demand operating where marginal revenue equals marginal costarrow_forwardHow, if at all, will a monopolist respond to a rise in the price of an input? (provide explanation with graphs)arrow_forward

- Consider the following cost and demand information for a monopolist. Demand is Qm = 34 - 1*Qm, Total Cost is TC = 20 + 2*Qm + .5*Qm2. At the profit-maximizing quantity, marginal revenue and marginal cost are equal to $........?arrow_forwardThere are two types of consumers: one half of consumers are type 1 (low type) and the other half are type 2 (high type). Type l's demand curve is q1 = 8 – P, while type 2's demand is given by q2 = 12 – P. Consider a monopolist selling its product to these consumers. Assume that the marginal cost is equal to zero. 1.1. Suppose that the firm can charge only one price, P, for each unit. (1) What is the market demand, Q? (Note: Q should be equal to q1 + q2.) What should be P that maximizes the monopoly's profit? For the profit- (2) maximizing P, will both types of consumers purchase the product, or only high type con- sumers purchase? (3) Given the price in (2), what is the resulting social surplus?arrow_forwardThe supply curve for a monopolist is always positively sloped.arrow_forward

- The following table (see MS Word/PDF version of Take-Home Quiz #5 handout, page 1) shows a market demand a monopolist is facing. Use the table to answer questions #4 thru #6. Average Marginal Marginal Rev. Total Economic Quantity Price Total Rev. Rev. Cost Cost Profit (Q) (P) (TR) (AR) (MR) (MC) (TC) (II) === =====%3D ====== =====3= 1 35 35 11 11 24 64 32 29 11 22 42 3 29 11 4 17 11 23 11 11 6. 120 11 7 17 -1 11 -7 11 9 99 11 -13 11 10 80 8. 11 [Extra Credit 2 pts] Fill all blanks in the Table 1 on the Quiz #5 handout. You will receive extra credit if you submit the completed table via email. Q4. If the monopolist sells 8 units of its product, how much total revenue (TR) will it receive from the sale? 40 O 87 O 104 O 112 O 164arrow_forwardHow will the price and output of a monopolist compare with perfect competitionarrow_forwardAnswer multiple choicearrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education