ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

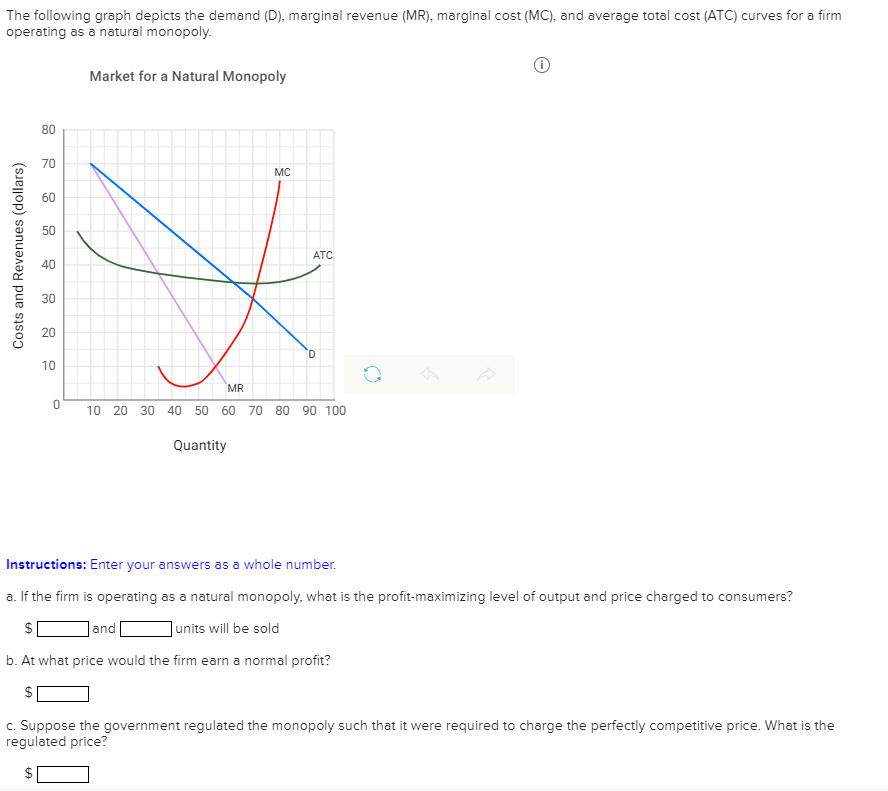

Transcribed Image Text:The following graph depicts the demand (D), marginal revenue (MR), marginal cost (MC), and average total cost (ATC) curves for a firm

operating as a natural monopoly.

Costs and Revenues (dollars)

80

70

60

50

40

30

20

10

0

Market for a Natural Monopoly

MC

Quantity

and

ATC

MR

10 20 30 40 50 60 70 80 90 100

D

B

↑

Instructions: Enter your answers as a whole number.

a. If the firm is operating as a natural monopoly, what is the profit-maximizing level of output and price charged to consumers?

$

units will be sold

b. At what price would the firm earn a normal profit?

c. Suppose the government regulated the monopoly such that it were required to charge the perfectly competitive price. What is the

regulated price?

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 5 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Consider the following firms. Would you regard any of them as a monopoly? Why or why not? Could you use the monopoly model in analyzing the choices of any of them? Explain. the best restaurant in town your barber or beautician your local cable company your campus bookstore Microsoft Amtrak the United States Postal Servicearrow_forwardWhat is the profit maximizing quantity of output for this pure monopoly?arrow_forwardThe graph illustrates an industry in which many firms operating in perfect competition are taken over by one firm that operates as a single-price monopoly. Draw the following shapes: 1) the consumer surplus arising from monopoly. Label it CS. 2) the deadweight loss arising from monopoly. Label it DWL 3) the loss of consumer surplus that is a gain to the monopoly as producer surplus. Label it Monopoly's gain. Indicate whether each of the following statements is true or false. At the competitive equilibrium, marginal social benefit equals marginal social cost. At the competitive equilibrium, the sum of consumer surplus and producer surplus is maximized. At the long-run competitive equilibrium, firms produce at the lowest possible long-run average cost. 30- 25- 20 15- 10- 5- Price and cost (dollars per haircut) 0+ 0.0 MR 1.0 2.0 3.0 4.0 Quantity (thousands of haircuts) MSC 5.0arrow_forward

- Dogarrow_forwardThe following graph shows the D, MR, and MC curves facing a Monopoly. If this firm finds itself producing 225 units, what should the firm do to its output level? $14 $12 $10 $6 $2 $0. 50 100 A. Decrease output to 200 units B. Increase output to 250 units C. Decrease output to 175 units D. No Change 150 200- 250 MC D MR 300 350arrow_forwardWhat is the difference between a monopoly's marginal revenue curve and a perfect competitor's marginal revenue curve? Please explain the difference in these markets by drawing the graphs.arrow_forward

- DeBeers has a monopoly on the production of diamonds. Use the following graph showing the demand, MR and cost curves of DeBeers to answer the questions below. How many carats of diamonds does DeBeers produce to maximize its annual profit? What price does it charge? How much annual profit does it make? If DeBeers was producing at the allocatively efficient level of output, how many carats of diamonds would it produce? What price would it charge? Suppose that the government decided to regulate DeBeers monopoly and imposes a price ceiling of $50 per carat of diamonds. How many carats of diamonds would DeBeers produce? What price would it charge? What profit would it make?arrow_forwardProvide an example of a product or service that operates as a monopoly. Explain your answer. What barrier to entry helped create this monopoly?arrow_forwardWhat are the entry barriers to Monopoly? Using the case of an electricity company operating a power plant identify at least two and explain briefly.arrow_forward

- 12. You’ve been hired as a consultant by a monopoly. You discover that the demand curve facing the monopoly is given by P = 80-Q and MC = 3Q. The firm is currently charging a price of $60. Using this information and a carefully drawn and labeled diagram and assuming that the firm should remain open, explain what the firm should do and why.arrow_forwardDescribe two different fundamental ways that a firm can try to move towards being a monopolyarrow_forwardWatch the video below on price gouging. Do you think this issue is related to the characteristics of a monopoly? Yes, how? If no,arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education