FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Topic Video

Question

None

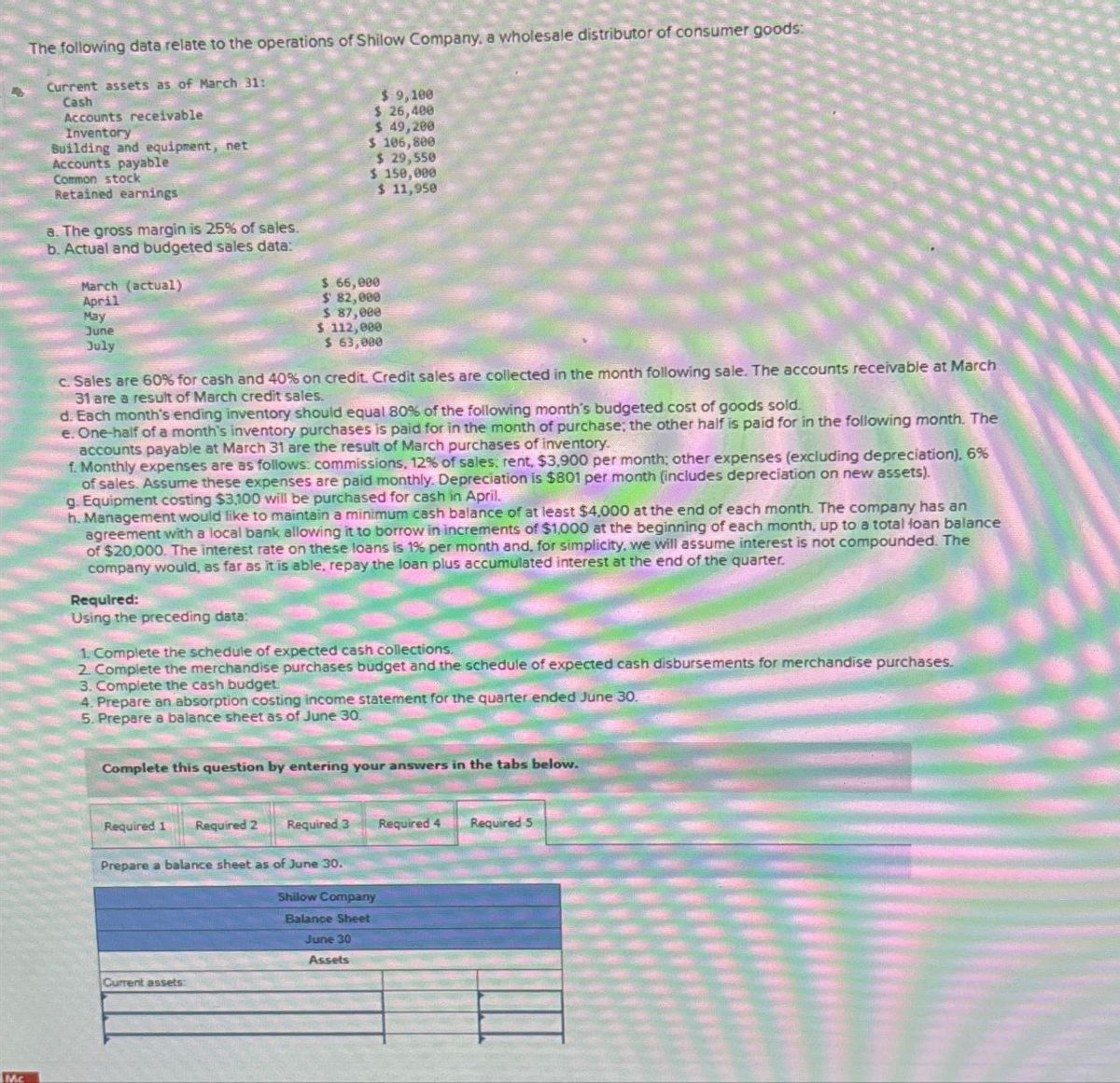

Transcribed Image Text:The following data relate to the operations of Shilow Company, a wholesale distributor of consumer goods:

Current assets as of March 31:

Cash

Accounts receivable

Inventory

Building and equipment, net

Accounts payable

Common stock

Retained earnings

a. The gross margin is 25% of sales.

b. Actual and budgeted sales data:

March (actual)

April

May

June

July

$ 9,100

$ 26,400

$ 49,200

$ 106,800

$ 29,550

$ 150,000

$ 66,000

$82,000

$ 87,000

$112,000

$ 63,000

$ 11,950

c. Sales are 60% for cash and 40% on credit. Credit sales are collected in the month following sale. The accounts receivable at March

31 are a result of March credit sales.

d. Each month's ending inventory should equal 80% of the following month's budgeted cost of goods sold.

e. One-half of a month's inventory purchases is paid for in the month of purchase; the other half is paid for in the following month. The

accounts payable at March 31 are the result of March purchases of inventory.

f. Monthly expenses are as follows: commissions, 12% of sales, rent, $3,900 per month; other expenses (excluding depreciation). 6%

of sales. Assume these expenses are paid monthly. Depreciation is $801 per month (includes depreciation on new assets).

g. Equipment costing $3,100 will be purchased for cash in April.

h. Management would like to maintain a minimum cash balance of at least $4,000 at the end of each month. The company has an

agreement with a local bank allowing it to borrow in increments of $1,000 at the beginning of each month, up to a total loan balance

of $20,000. The interest rate on these loans is 1% per month and, for simplicity, we will assume interest is not compounded. The

company would, as far as it is able, repay the loan plus accumulated interest at the end of the quarter.

Required:

Using the preceding data:

1. Complete the schedule of expected cash collections.

2. Complete the merchandise purchases budget and the schedule of expected cash disbursements for merchandise purchases.

3. Complete the cash budget

4. Prepare an absorption costing income statement for the quarter ended June 30.

5. Prepare a balance sheet as of June 30.

Complete this question by entering your answers in the tabs below.

MC

Required 1 Required 2

Required 3 Required 4

Required 5

Prepare a balance sheet as of June 30.

Shilow Company

Current assets:

Balance Sheet

June 30

Assets

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 5 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education