FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

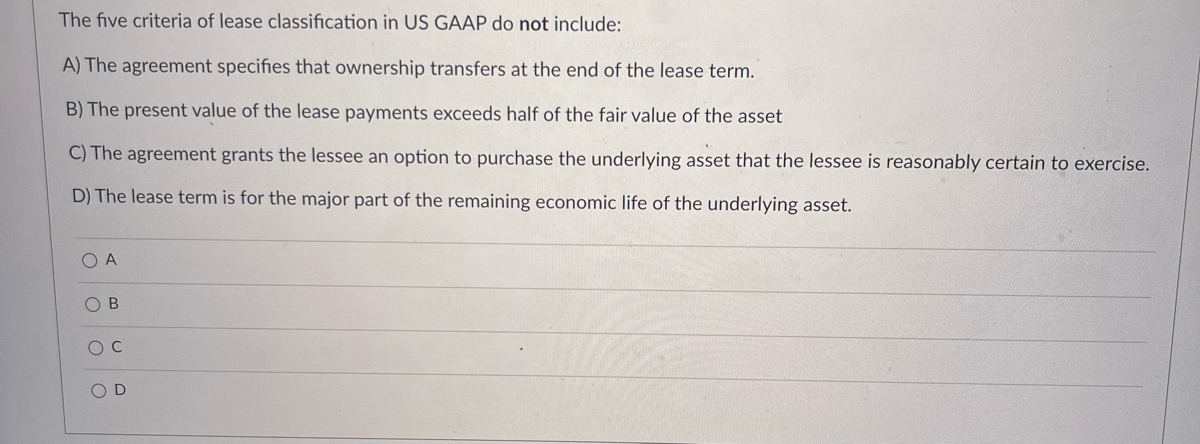

Transcribed Image Text:The five criteria of lease classification in US GAAP do not include:

A) The agreement specifies that ownership transfers at the end of the lease term.

B) The present value of the lease payments exceeds half of the fair value of the asset

C) The agreement grants the lessee an option to purchase the underlying asset that the lessee is reasonably certain to exercise.

D) The lease term is for the major part of the remaining economic life of the underlying asset.

O A

O B

O D

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- For which of the following conditions will the lessor classify a lease as a sales-type lease? a.The leased asset may be exchanged for a similar asset during the lease term. b.The present value of the sum of the lease payments is equal to or more than the fair value of the underlying asset. c.The lease term is less than one year. d.The lease term is half of the underlying asset’s economic life.arrow_forwardLease A does not contain a bargain purchase option, but the lease term is equal to 90 percent of the estimated economic life of the leased property. Lease B does not transfer ownership of the property to the lessee by the end of the lease term, but the lease term is equal to 75 percent of the estimated economic life of the leased property. How should the lessee classify these leases under U.S. GAAP? Lease A Lease B A.) Operating lease Capital lease B.) Operating lease Operating lease C.) Capital lease Capital lease D.) Capital lease Operating leasearrow_forwardUnder IFRS 16, lessors are required to account for lease receipts from operation leases as a. Income, on a straight-line basis over the lease term b. Revenue, on a reducing balance basis over the lease term c. Revenue, at the end of lease term d. Income, on inception date of the leasearrow_forward

- The methods of accounting for a lease by the lessor are Select one: a. operating and finance lease methods. b. none of these. c. operating and leveraged lease methods. d. operating, sales, and finance lease methods. Clear my choicearrow_forwardam. 104.arrow_forward(48) If, as part of the accounting for a lease, the lessee debits an asset and credits a liability, then the lease must be a(n): A. Finance Lease B. Operating Lease C. Operating lease or finance lease D. none of the abovearrow_forward

- Part 1: New Lease Accounting – using IFRS 16 Leases Effect Analysis. Which payments are to be included in the measurement of lease assets and lease liabilities? Also, discuss the pros and cons of excluding the following payments from the measurement. - Variable lease payments linked to future use or sales - Optional payments relating to lease-extension option when a lessee is not reasonably certain to exercise the option.arrow_forwardFor accounting purposes, which one of the following conditions would automatically cause a lease to be classified as a capital lease? Multiple Choice O O O The lessee can purchase the asset at fair market value at the end of the lease. The lease transfers ownership of the asset to the lessee by the end of the lease term. The lease term equals 60 percent or more of the asset's estimated economic life. The present value of the lease payments equals 75 percent of the asset's fair market value at lease inception. The lessor can renew the lease at the end of the lease term.arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education