ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

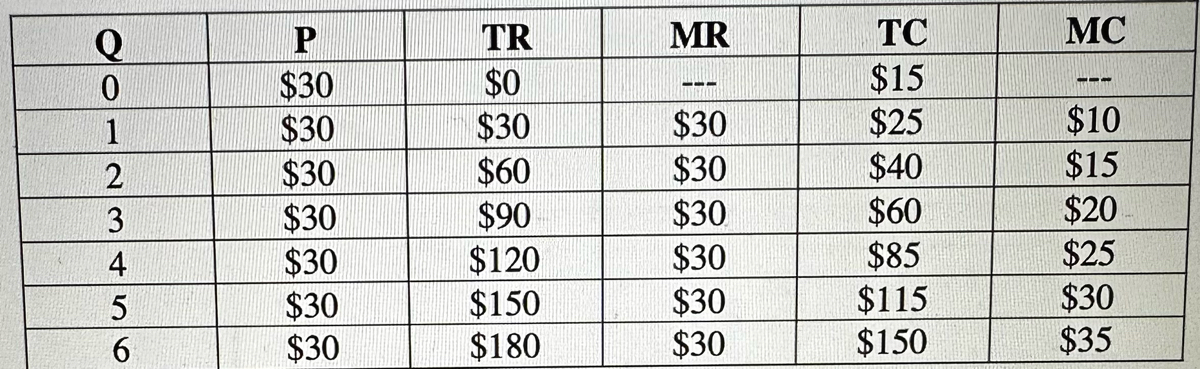

The firm is perfectly competitive is evident from its a)increasing marginal cost b)increasing total cost c)zero economic profits d)constant marginal revenue e)absence of marginal values at Q=0. Using the table below

Transcribed Image Text:Q

0

1

2

3

4

5

6

P

$30

$30

$30

$30

$30

$30

$30

TR

$0

$30

$60

$90

$120

$150

$180

MR

111

$30

$30

$30

$30

$30

$30

TC

$15

$25

$40

$60

$85

$115

$150

MC

111

$10

$15

$20

$25

$30

$35

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Advanced Microeconomics, Production Theory: Perfect Competitionarrow_forwardUse the following table to answer the next question. The table shows the total costs associated with varying levels of output produced by a perfectly competitive firm. Output 0 1 2 3 4 Total Cost $1,400 1,600 2,000 2,600 3,500 4,800 If the product sells for $800 a unit, the firm's profit-maximizing output isarrow_forwardThe supply curve for a competitive firm is: a)it’s entire MC curve b)the upward-sloping portion of its MC curve c)it’s MC curve above the minimum point of the AVC curve d)it’s MC curve above the minimum point of the ATC curve e)it’s MR curvearrow_forward

- A perfectly competitive firm will be operating at its shutdown point if it operates at the minimum point on its ________ cost curve. a ) average total b ) marginal c ) total d ) average variablearrow_forwardMatch the words from the list below to complete the following statement A price taker firm will maximise by changing output, until equals marginal cost. average cost output total revenue marginal revenue marginal cost profitarrow_forwardUse the values for a perfectly competitive firm below to answer the questions: Price Quantity Total Cost Fixed Cost Variable Cost $10 2,000 $24,000 $8,000 $16,000 (A) Should this firm shut down in the short run? (B) Assume this firm's total costs do not change in the long run. Should this firm exit in the long run? (C) Are your answers to (a) and (b) different? Explain in one to four sentences.arrow_forward

- Problems: Question #6: The Phantom Farms bakery produces pumpkin pies according to the following short run cost schedules. Assume the pumpkin pie industry is perfectly competitive and that the bakery can only produce and sell whole pies. AVC = ATC = MC = Quantity (pies) TFC = total TVC = total TC = total fixed cost variable cost average average total marginal cost variable cost cost cost (i) same as (i) 1 14 18 14.0 18 14 2 same as (i) (ii) 28 12.0 14 10 3 same as (i) 38 42 12.7 (v) 14 4 same as (i) 60 (iii) 15.0 16 22 same as (i) 86 90 17.2 18 (vi) same as (i) 116 120 (iv) 20 30 Fill in the five missing cost numbers indicated in the table above. (i) (ii) (iii) (iv) (v) (vi) If the price of pumpkin pies is $22 per pie, how many pies should Phantom Farms produce in the short run? What profit or loss does the firm earn? Explain how you arrived at this answer. Illustrate Phantom Farms' choice with a graph and indicate profits or losses. 3arrow_forwardThe demand curve facing a perfectly competitive firm is: a)the same as the market demand b)downward-sloping and less flat than the market demand curve c)downward-sloping and flatter than the market demand curve d)perfectly horizontal e)perfectly verticalarrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education