ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

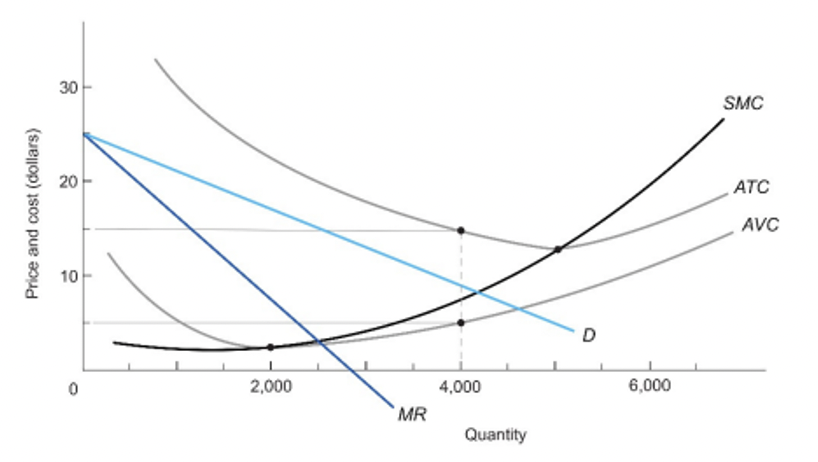

- The figure below shows

demand , marginal revenue, and short-run costcurves for a

a. How much should the firm produce? What

b. What is the firm’s

c. If the firm shuts down in the short run, how much will it lose?

Transcribed Image Text:Price and cost (dollars)

30

20

10

2,000

MR

4,000

Quantity

D

6,000

SMC

ATC

AVC

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 5 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- If you were managing a monopoly, and small entrant tried to enter your market, explain why it might make sense to cut prices so low that you would suffer losses for a time.arrow_forwardDiscuss the economic factors that lead to the development of monopolies. Examples of monopolies include electric utilities, railroads.arrow_forwardA perfectly competitive firm is expected to make a $0 economic profit in the long-run. What type(s) of profit would you expect a monopolist to earn in the long-run? Why the difference?arrow_forward

- ssume there is no price discrimination: Matthew, Rachel, Janice, and Mandy own the only ice company in town (they have a monopoly on the ice market). Matthew wants to sell as much ice as possible without losing money. Rachel wants the ice company to bring in as much revenue as possible. Janice wants to maximize total surplus and Many wants to make the largest possible profit. Use ONE clearly-labelled graph of the ice company’s marginal revenue, demand, and cost curves to show the price and quantity (i.e., ice) each person desires. Provide explanation.arrow_forwardWhat are the economic benefits of perfect competition compared to a monopoly?arrow_forward28. The following is a graph of a non-price discriminating monopoly in the short run. (a) What is the profit-maximizing level of output? (b) What is the economic profit? (c) What is the long- run equilibrium of this firm? £ P1 supernormal profit Q1 MR MC AC D=ARarrow_forward

- Explain how a monopoly arises and distinguish between a single-price monopoly and a price-discriminating monopoly.arrow_forwardCorrectly illustrate the following monopolies: a. A monopoly is producing at the profit-maximizing output and is earning an economic profit. b. A monopoly is producing at the profit-maximizing output and is earning normal profits.arrow_forward↑ Price Price Panel B NECK D Quantity Panel A Price D Panel C D Use the figure above. Which of the following statements is correct? All the answers are correct. Price Panel B represents the typical demand curve for a perfectly competitive firm. Panel A represents the typical demand curve for a monopoly. Panel D. ⒸPanel A represents the typical demand curve for a perfectly competitive market. Darrow_forward

- Use the cost and revenue data to answer the questions. Quantity Price Total Revenue Total Cost 10 90 15 80 20 70 25 60 30 50 35 40 900 1200 1400 1500 1500 1400 675 825 1025 1250 1500 1850 What is marginal revenue when quantity is 25? What is marginal cost when quantity is 15? If this firm is a monopoly, at what quantity will profit be maximized? If this is a perfectly competitive market, which quantity will be produced? $ 20 $ 90 Incorrect quantity: 6 Incorrect quantity: 8 Incorrectarrow_forwardResearch the difference between pure competition and monopoly pricing. Compare and contrast the differences between the two and then explain which you would prefer if you were a shipper (you’re paying the bill) and why? Also, consider your answer if you were the carrier (you’re getting paid) and explain how you might feel differently and why?arrow_forwardWhat are the key characteristics of perfect competition? How does monopoly differ from perfect competition? Which market achieves economic efficiency? Write an example of perfect competition, and one for monopoly.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education