ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

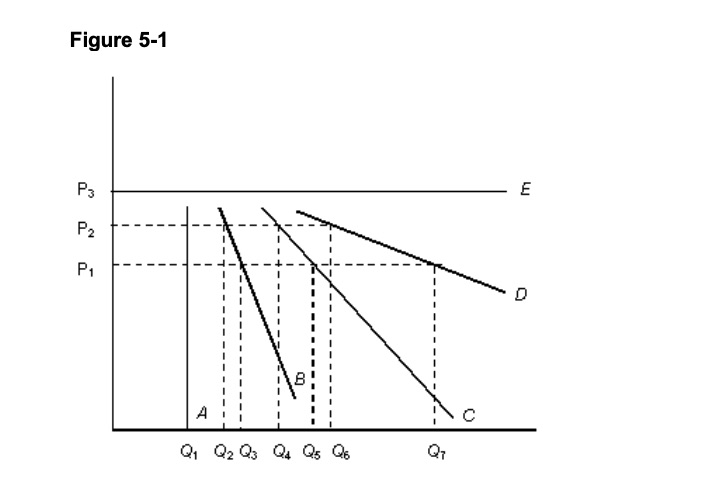

Refer to Figure 5-1. The

| a. |

consumers can purchase any quantity they want regardless of the |

|

| b. |

there is no change in quantity demanded as the price changes. |

|

| c. |

the smallest price change will cause consumers to change their consumption by a huge amount. |

|

| d. |

the smallest price increase will cause consumers to switch to the producer with the lowest prices |

|

| e. |

|

Transcribed Image Text:Figure 5-1

P3

P2

P1

Q, Q2 Q3 Q4 Qs Q6

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Match each of the terms to their definition or description. Cross-Price Elasticity Elasticity Income elasticity Price Elasticity of Demand A. the effect that a change in price of one good has on the quantity demanded of another good. B. responsiveness of quantity demand to a change in price C. a measure of responsiveness D. the effect that a change in income has on quantity demand for a goodarrow_forwardConsider the supplier of a product that is an inferior good. For instance, an aluminum supplier for a canned goods producer. During a recession during which average incomes fall, which of the following best describes what would happen to the profit-maximizing price of the supplier? a. The supplier’s profit-maximizing price would decrease due to an increase in demand. b. The supplier’s profit-maximizing price would increase due to an increase in demand. c. The supplier’s profit-maximizing price would decrease due to a reduction in demand. d. The supplier’s profit-maximizing price would increase due to a reduction in demand.arrow_forwardUse the figure below to answer the following question 16 14 12 10 Price 9 Quantity 8. Figure 4.3.3 Figure 4.3.3 shows the market for a good. At the market equilibrium, demand for the good is and supply of the good is 1) elastic; perfectly inelastic 2) unit elastic; perfectly elastic 3) inelastic; perfectly elastic 4) unit elastic; unit elastic 5) elastic; perfectly elastic 6. 2.arrow_forward

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education