ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

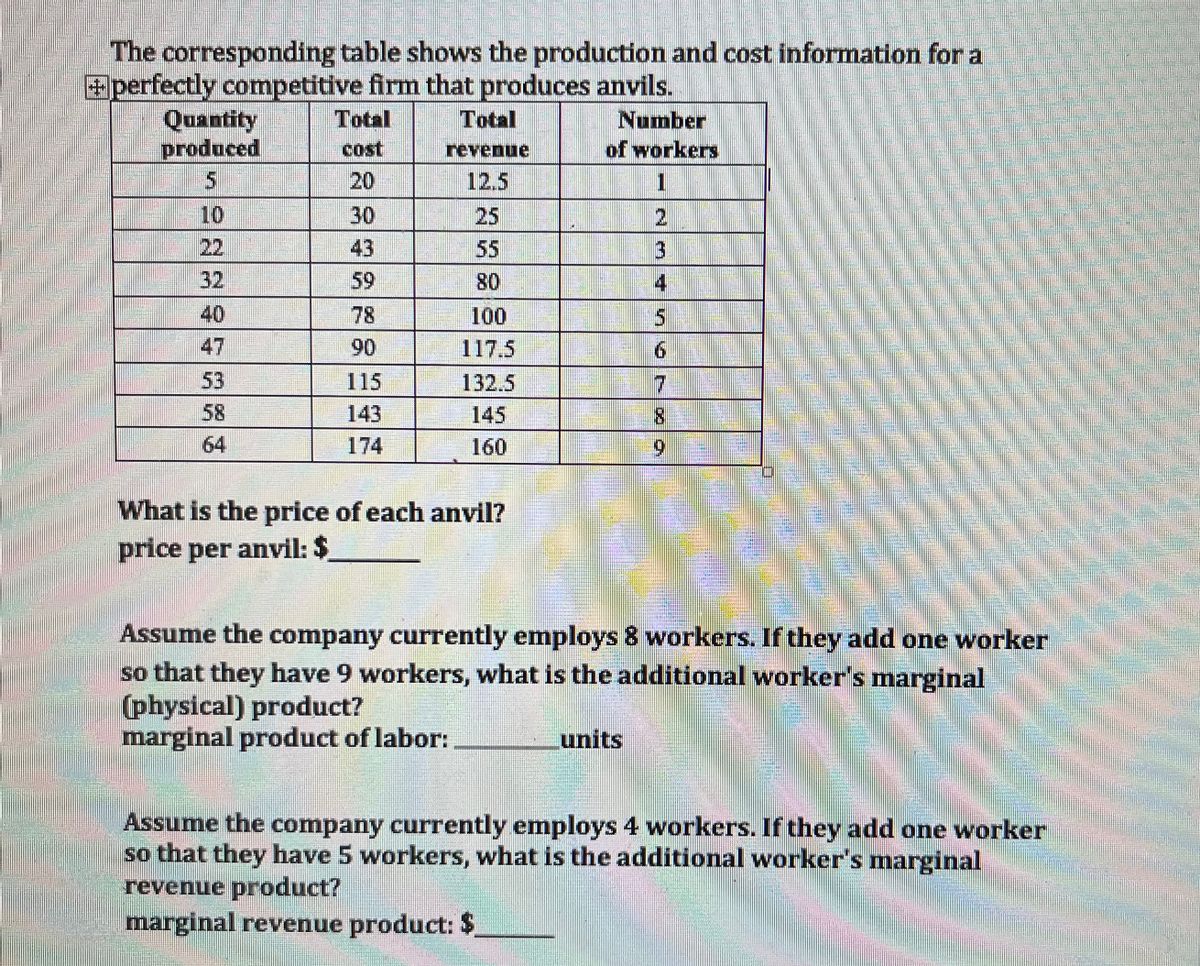

Transcribed Image Text:The corresponding table shows the production and cost information for a

+perfectly competitive firm that produces anvils.

Quantity

produced

10

22

40

53

30

43

59

90

115

143

revenue

80

100

117.5

132.5

145

160

What is the price of each anvil?

price per anvil: $

Number

of workers

1

2

3

4

5

6

7

8

9

Assume the company currently employs 8 workers. If they add one worker

so that they have 9 workers, what is the additional worker's marginal

(physical) product?

marginal product of labor:

units

Assume the company currently employs 4 workers. If they add one worker

so that they have 5 workers, what is the additional worker's marginal

revenue product?

marginal revenue product: $

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 5 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- 20) - Google Chrome "mod/quiz/attempt.php?attempt%3=1579003&cmid%3812962&page%3D2 em (Academic 20- MC ATC AVC 16 4. 5 10 15 20 25 30 35 40 45 50 Quantity (units per day) The above figure shows the cost curves for a perfectly competitive firm. If all firms in the market have th same cost curves and the price equals $16 per unit Select one: O a. over time, the price will fall as new firms enter the market. O b. over time, firms will leave this market. O c. the market is in its long-run equilibrium. O d. the firm is making zero economic profit. o search hp Price and cost (dollars per unit)arrow_forwardQuestion 4 For a firm, the production function represents the relationship between OOO implicit costs and explicit costs. quantity of inputs and total cost. quantity of inputs and quantity of output. quantity of output and total cost. iz Instructions Question 5 Grace is a self-employed artist. She can make 20 pieces of pottery per week. She is considering hiring her sister Kate to work for her. Both she and Kate can make 35 pieces of pottery per week. What is Kate's marginal product? O 15 pieces of pottery O22.5 pieces of pottery O 35 pieces of pottery O 55 pieces of potteryarrow_forwardA television production firm is able to produce TVs according to the short-run production table below. With the hiring of which worker would the diminishing marginal product begin? Total Output Number of of Televisions Workers per day 0 0 30 2 70 3 125 185 225 250 260 255 240 01 4 5 6789arrow_forward

- O Macmillan Learning One feature of production in the short run is diminishing marginal returns. The graph shows a total product curve for Barry's Ball Bearings. Identify the sections of the graph that illustrate increasing (IMR), diminishing, (DMR) and negative marginal returns (NMR). Output per hour 13 12 11 10 9 8 7 6 5 4 3 2 1 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 Labor units IMR Answer Bank DMR NMRarrow_forwardThe total cost of Mr plow a snow removal business is given in the table belowarrow_forwardshows the long-run average costs for three firms. Quantity Ali's Hats 1 2 3 4 5 6 7 $110 60 90 115 150 220 300 Bodi's Bats $110 80 70 70 70 70 90 Cody's Mats $110 90 80 70 50 20 30 a) In which industry, Hats, Bats or Mats, would there likely be many small firms? Industry: (Click to select) · b) In which industry, Hats, Bats or Mats, would there likely be firms of many different sizes? Industry: (Click to select) - c) Which industry Hats Bats or Mats, would likely be dominated by a few large firms? Industry (Click to select) Hats Bats Matsarrow_forward

- The table below shows ABC firm short-run production function. The company hires workers at a wage rate of $400 a day and his total fixed cost is $1000. Labor (workers) Total product (output) 0 0 1 12 2 25 3 30 4 44 5 50 Calculate the average total cost of producing 25 Calculate total cost of producing 47 units. Calculate average variable cost if 30 units are produced. Calculate the marginal product of producing 44 units. Calculate average product of the 4th workerarrow_forwardQuestion When do firms decide to shut down production in the short run? Explain it. How is the short run average cost curve and the long run average cost curve shaped? What is the difference between them? Graphical representation of the short-run total cost curve showing total cost, fixed cost, variable cost: and The marginal cost and average total cost:arrow_forwardConsider the same firm from the Monday assignment but now let's call that cost schedule total variable cost. Q 1 2 3 4 5 6 7 8 9 TVC 12 20 24 28 34 42 52 64 78 And let's imagine that there is fixed costs of 18 which is sunk in the short run. a. Show this firm's average total cost, average variable cost and marginal cost on a graph. Indicate the efficient scale (I don't think the book uses the words "efficient scale" but it's the quantity where profit would be zero when P=MC. We will discuss what I mean by "efficient scale but probably not before Thursday. By "indicate" I mean give the quantity and MC. I don't need every point to be exactly to scale, I just care about the general shape of the curves, where things cross and the location and…arrow_forward

- Use the following table to answer the next question. Output 0 1 2 3 4 5 Total Cost $5 9 12 15 20 27 The average total cost of producing 4 units of output is $ type your answer... Marginal cost is equal to average total cost between type your answer... and type your answer... units of output.arrow_forwardThe table below shows the weekly cost of producing cowboy hats. Complete the table by filling in the missing values. Instructions: Round your answers to 1 decimal place. Cowboy Hat Production Costs Total Fixed Cost (dollars) $2,000 Total Variable Cost (dollars) Total Cost (dollars) $2,000 Average Fixed Cost (dollars) Average Variable Cost (dollars) Average Total Cost (dollars) Output $0 10 300 24 $4 $230 20 2,460 23 123 30 660 66.7 22 40 2,900 72.5 50 1,200 24arrow_forwardPlease answer all parts and show your work!arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education