ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

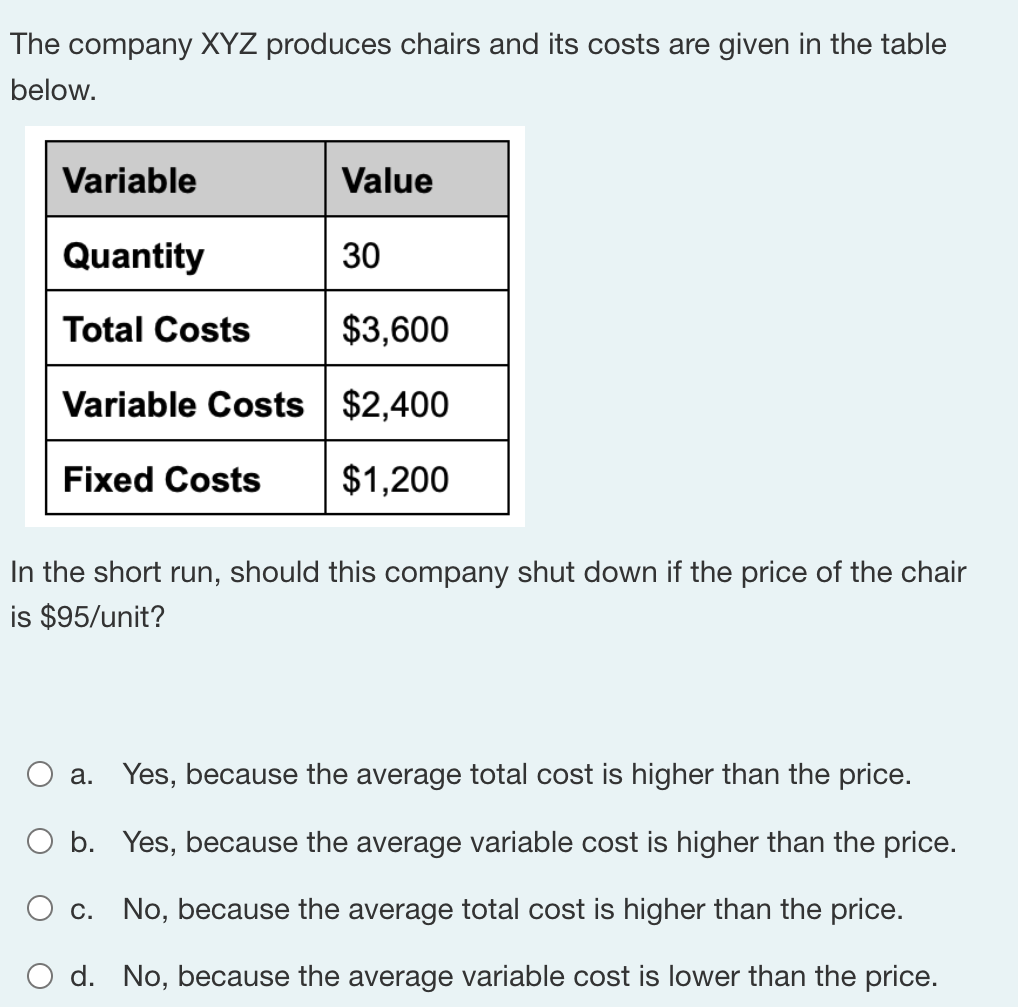

Transcribed Image Text:The company XYZ produces chairs and its costs are given in the table

below.

Variable

Quantity

Total Costs

Variable Costs

Fixed Costs

Value

30

$3,600

$2,400

$1,200

In the short run, should this company shut down if the price of the chair

is $95/unit?

a. Yes, because the average total cost is higher than the price.

b. Yes, because the average variable cost is higher than the price.

O c. No, because the average total cost is higher than the price.

d. No, because the average variable cost is lower than the price.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps with 6 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- The industry in the figure below consists of many firms with identical cost structures, and the industry experiences constant scale. Consider a change in demand from D₁ to D2, which increases price from $20 to $30 in the short run. Price $50 $40 $30 $20 $10 0 10 20 Market 30 D₁ 40 Quantity S₁ D₂ 50 60 70 Tools LRS O S₂ Instructions: Enter your answers as a whole number. a. Draw the new short-run market supply curve that will occur in response to the increase in demand and increase in price. Instructions: Use the tool provided 'S2' and be sure your supply curve includes the new equilibrium price and quantity. b. Draw the long-run supply curve. Instructions: Use the tool provided 'LRS' and plot only the endpoints over the entire range of output (0-60). The new equilibrium price is $ 20 and the new equilibrium quantity is 40.arrow_forwardWhat does it mean to be operating a firm in the "long run?" What does it mean to be operating a firm in the "short run"? What are the practical implications for managing a business if you are in "short run?arrow_forwardNonearrow_forward

- Last answer was wrong. Don't give incorrect answers plzarrow_forwardSee attached imagearrow_forwardIn perfect competition, if the marginal cost increases which way does the curve shift? what are some things that would increase the marginal cost curve and if the MC curve shifts then does the ATC curve?arrow_forward

- Brody's firm produces trumpets in a perfectly competitive market. The table below shows Brody's total variable cost. He has a fixed cost of $240, and the price per trumpet is $60.-Calculate the average total cost of producing 6 trumpets. Show your work. -Calculate the marginal cost of producing the 11th trumpet. -What is Brody's profit-maximizing quantity? Use marginal analysis to explain your answer. -At the profit-maximizing quantity you determined in part (c), calculate Brody's profit or loss. Show your work. -Brody also produces saxophones at a loss in a perfectly competitive market. Draw a correctly labeled graph for Brody's firm showing the following at a market price of $200. -Brody's profit-maximizing quantity of saxophones -Brody's loss, completely shaded Quantity Total Variable cost 6 $120 7 $145 8 $165 9 $220 10 $290 11 $390arrow_forwardThe owner of Tie-Dyed T-shirts, a perfectly competitive firm, hires you to give him economic advice. He tells you that the market price for his shirts is $15 and that he is currently producing 200 shirts at an AVC of $10 and an ATC of $20. What would you recommend that he do? O a. Tell him that you cannot make any recommendations until you know what his fixed costs are. O b. Continue producing in the short run, as his loss from production is less than his fixed costs, but exit the industry in the long run if there are no changes in economic conditions. Oc Shut down in the short run, as he is incurring a loss, and leave the industry in the long run, if there are no changes in economic conditions. O d. Continue to produce in the short run, even though he is earning a loss, and expand production in the future hoping to increase market share and total revenue.arrow_forwardWhat will happen when variable costs rise in a perfectly competitive industry? Selected answer will be automatically saved. For keyboard navigation, press up/down arrow keys to select an answer. a b C Question 5 d The number of firms will eventually increase, but the existing firms will cut back production in the short run. The number of firms will eventually decrease and the existing firms will cut back production in the short run. The number of firms will eventually decrease, but the existing firms will expand production in the short run. The number of firms will eventually increase and the existing firms will expand production in the short run. Barrow_forward

- answer quicklyarrow_forward,arrow_forwardWhich of the following best explains why a firm would not stop producing if the loss is less than its fixed costs? O Fixed costs are paid regardless of whether something or nothing is produced, and the firm receives enough revenue per unit to cover ATC and some MC. O Fixed costs are paid regardless of whether something or nothing is produced, and the firm receives enough revenue per unit to cover ATC and some FC. O Fixed costs are paid regardless of whether something or nothing is produced, and the firm receives enough revenue per unit to cover AVC and some FC. O Fixed costs are paid regardless of whether something or nothing is produced, and the firm receives enough revenue per unit to cover AVC and some MC.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education