FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Topic Video

Question

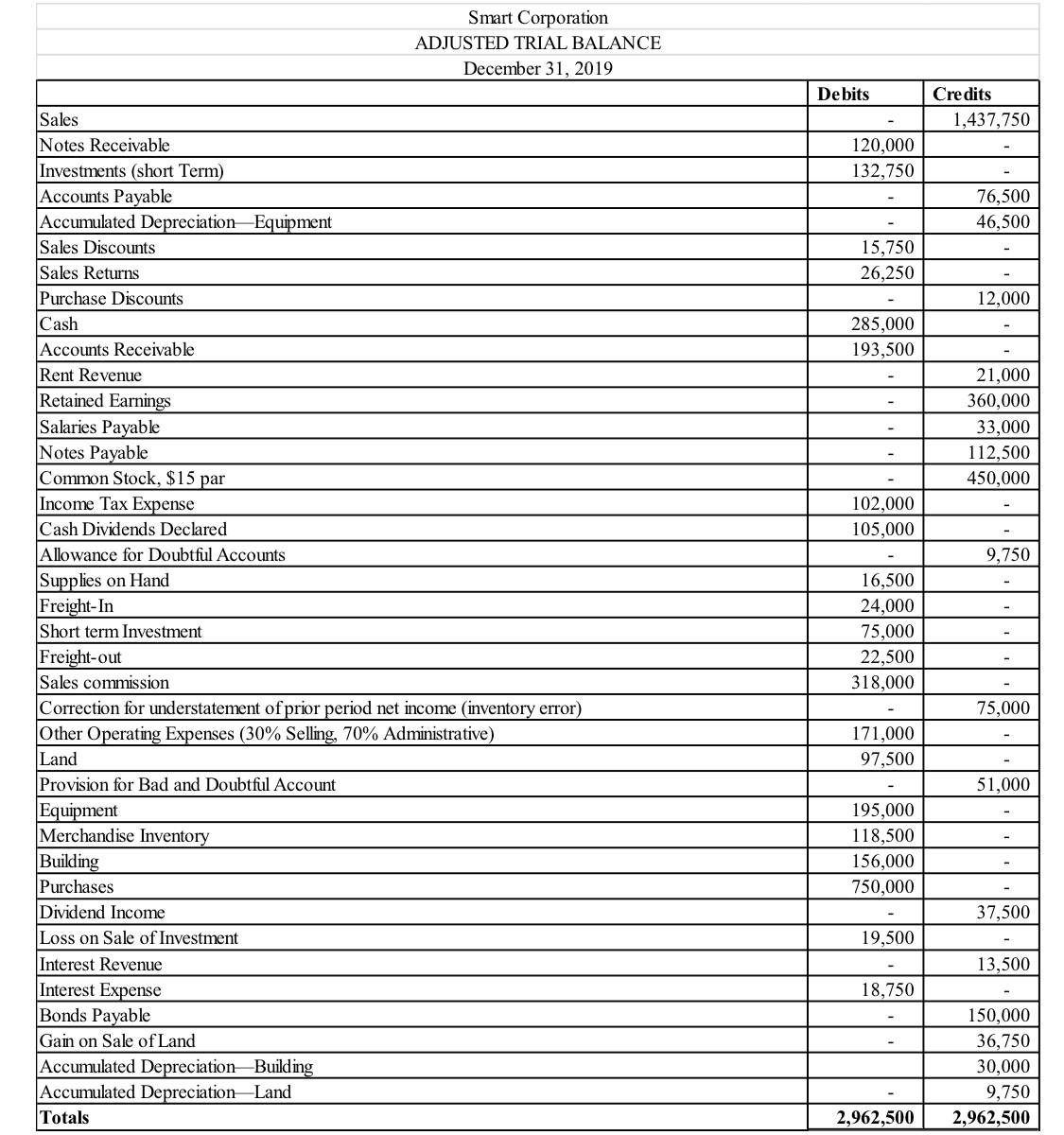

The company uses the periodic inventory system. A physical count of inventory on December 31 resulted in an inventory amount of $50,000.

Instructions:

3. Prepare a Statement of Financial Position as at December 31, 2019.

a. Report Form

b. Account Form

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 4 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- The records of Earthly Goods provided the following Information for the year ended December 31, 2020. At Cost At Retail $ 521, 35e $ 977,150 4,138, 245 January 1 beginning inventory 6,448, 700 129, 350 5,595,700 49,600 Purchases Purchase returns Sales 62, 800 Sales returns Requlred: 1. Prepare an estimate of the company's year-end inventory by the retall method. (Round all calculations to two decimal places.) EARTHLY GOODS Estimated Inventory December 31, 2020 At Cost At Retail Goods available for sale: Goods available for sale Cost to retail ratio Estimated ending inventory at costarrow_forwardA company uses a perpetual system to record inventory transactions. The company purchases inventory on account on February 9, 2021, for $50,000 and then sells this inventory on account on March 7, 2021, for $70,000. Record the transactions for the purchase and sale of the inventory. (If no entry is required for a particular transaction/event select "No Journal Entry Required" in the first account field.)arrow_forwardPlease help mearrow_forward

- Recording Inventory Purchases and Sales on Account Record the entries for the following transactions for Shoppers Inc. Shoppers uses a perpetual inventory system and records sales taxes payable at the point of sale. a. On January 1, 2020, Shoppers Inc. purchased merchandise for resale for $56,000 on credit terms 1/15, n/30. Shoppers Inc. incurred a shipping charge of $288 on the purchase, which was immediately paid. Shoppers Inc. uses the gross method to record purchases. b. Shoppers Inc. sells $22,400 of inventory during the first week of January 2020, to customers for $40,000, with a sales tax rate of 5%. Of the total sales for the week, 30% are cash sales, and 70% are credit sales (n/30). c. On January 14, 2020, Shoppers Inc. pays the balance for purchases on account. d. Assume instead that Shoppers Inc. sells $24,000 of inventory during the first week of January 2020 to customers for $44,800, which includes a 5% sales tax. Of the total sales for the week, 30% are cash sales, and…arrow_forwardThe units of an item available for sale during the year were as follows: Jan 1 Inventory 15 units at 122 April 15 Purchase 140 units at 116 September 9 Purchase 26 units at 122 There are 31 units of the item in the physical inventory at December 31. The periodic inventory system is used. Determine the inventory cost using the last-in, first-out (LIFO)arrow_forwardRapid Resources, which uses the FIFO inventory costing method, has the following account balances at July 31, 2025, prior to releasing the financial statements for the year: Merchandise Inventory, ending $ Cost of Goods Sold Net Sales Revenue Date 16,500 71,000 122,000 Jul. 31 Requirement 1. Prepare any adjusting journal entry required from the given information. (Record debits first, then credits. Select the explanation on the last line of the journal entry. For situations that do not require an entry, make sure to select "No entry required" in the first cell in the "Accounts" column and leave all other cells blank.) Accounts and Explanation Credit Rapid has determined that the current replacement cost (current market value) of the July 31, 2025, ending merchandise inventory is $13,500. Read the requirements. Debit 4arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education