Related questions

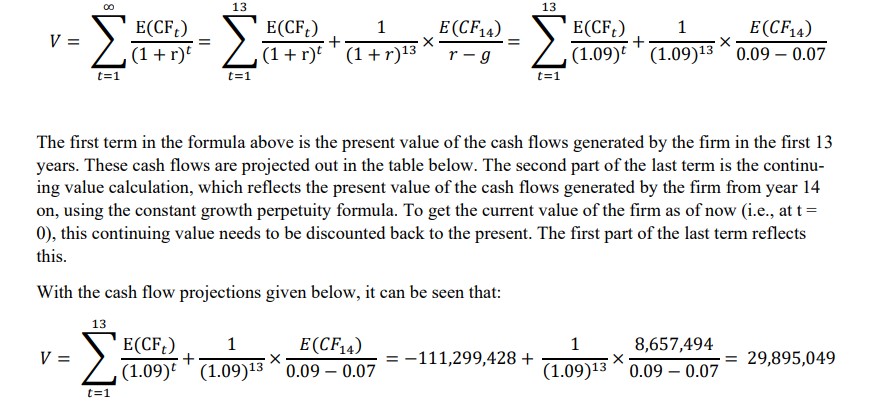

Suppose you are asked to value a small start-up company that is expected to generate a Free Cash

Flow of - $100 million next year, and - $50 million in the following year (year 2), before the firm

turns profitable in year 3. Its first positive cash flow is equal to $2 million, and cash flows are expected to grow at a rate of 15% per year for 10 years (until year 13). Then, between year 13 and 14,

the growth rate drops to 7% and stays there forever. Value the start-up company if the relevant discount rate is equal to 9%.

My question is when calculating the perpetuity with a cosntant growth rate, why we muliply:

1/(1+r)^13 * E(CF_14)/0,09-0,07

Why does this make sense?

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps with 2 images

- You are building a free cash flow to the firm model. You expect sales to grow from $1.6 billion for the year that just ended to $1.84 billion five years from now. Assume that the company will not become any more or less efficient in the future. Assume that the company will grow at a constant rate for 5 years, and then at a constant rate of 2.334672% for year 5 and onward after that. Use the following information to calculate the value of the equity on a per-share basis. a. Assume that the company currently has $528 million of net PPSE. b. The company currently has $176 million of net working capital. c. The company has operating margins of 10 percent and has an effective tax rate of 30 percent. d. The company has a weighted average cost of capital of 9 percent. This is based on a capital structure of two-thirds equity and one-third debt. e. The firm has 2 million shares outstanding. Do not round intermediate calculations. Round your answer to the nearest cent. Sarrow_forwardConsider the case of Morose Otter Hydraulic Manufacturers Inc.: Morose Otter Hydraulic Manufacturers Inc. is expected to generate a free cash flow (FCF) of $210,000 this year, and the FCF is expected to grow at a rate of 18% over the following two years (FCF2 and FCF3). After the third year, however, the company's FCFS are expected to grow at a constant rate of 8% per year, which will last forever (FCF4 - ). If Morose Otter's weighted average cost of capital (WACC) is 16%, complete the following table and compute the current value of Morose Otter's operations. Round all dollar amounts to the nearest whole dollar, and assume that the firm does not have any nonoperating assets in its balance sheet and that all FCFS occur at the end of each year. Year CF PV(FCF,) FCF1 $181,034 V $184,156 ▼ $210,000 FCF2 $247,800 $292,404 V $315,796 ▼ $3,157,960 v FCF3 $187,331 FCF4 Horizon Value4- 00 $2,180,141 ▼ $3,081,485 ▼ Voparrow_forwardDemo Inc. is expected to generate a free cash flow (FCF) of $8,715.00 million this year (FCF1 = $8,715.00 million), and the FCF is expected to grow at a rate of 25.00% over the following two years (FCF2 and FCF). After the third year, however, the FCF is expected to grow at a constant rate of 3.90% per year, which will last forever (FCF4). Assume the firm has no nonoperating assets. If Demo Inc.'s weighted average cost of capital (WACC) is 11.70%, what is the current total firm value of Demo Inc.? (Note: Round all intermediate calculations to two decimal places.) $156,455.46 million $26,304.04 million $207,691.99 million $187,746.55 million Demo Inc.'s debt has a market value of $117,342 million, and Demo Inc. has no preferred stock. If Demo Inc. has 600 million shares of common stock outstanding, what is Demo Inc.'s estimated intrinsic value per share of common stock? (Note: Round all intermediate calculations to two decimal places.) $64.19 $71.71 $ 65.19 $195.57arrow_forward

- Daniel Sawyer, the CEO of the Sawyer Group, is initiating planning for the company's operations next year, and he wants you to forecast the firm's additional funds needed (AFN). The firm is operating at full capacity. Data for use in your forecast are shown below. Based on the AFN equation, what is the AFN for the coming year? Dollars are in millions. Last year's sales = S0 $350 Last year's accounts payable $40 Sales growth rate = g 30% Last year's notes payable $50 Last year's total assets = A0* $320 Last year's accruals $30 Last year's profit margin = PM 5% Target payout ratio 60% Select the correct answer. a. $69.3 b. $72.7 c. $62.5 d. $65.9 e. $76.1arrow_forwardKinkead Inc. forecasts that its free cash flow in the coming year, i.e., at t = 1, will be −$10 million, but its FCF at t = 2 will be $20 million. After Year 2, FCF is expected to grow at a constant rate of 4% forever. If the weighted average cost of capital is 14%, what is the firm's value of operations, in millions? a. $167 b. $158 c. $193 d. $175 e. $18arrow_forwardI attached the image of the question.arrow_forward

- We are predicting for the end of this fiscal year: Skunk Products' EBIT is $1000, its tax rate is 35%, depreciation is $100, capital expenditures are $200, accounts receivable increase by $100, and accounts payable decrease by $100. What is the free cash flow to the firm? The FCFF will grow at 3%, WACC is 10%. What is the value of the company's assets? FCFF1 = $arrow_forwardsomeone solve this but not use excelarrow_forwardA firm's financial managers are evaluating two potential investments with a cost of $10,000 each. They forecast returns of $3,000 per year for 5 years for Investment A and $4,000 per year for 5 years for Investment B. The returns are more uncertain for B than for A. Which of the following is true? Investment A is better than B according to shareholder wealth maximization criterion. Investment B is better than A according to shareholder wealth maximization criterion. Investment A is better than B according to the profit maximization criterion. Investment B is better than A according to the profit maximization criterion.arrow_forward

- Kinkead Inc. forecasts that its free cash flow in the coming year, i.e., at t = 1, will be -$18 million, but its FCF at t = 2 will be $40 million. After Year 2, FCF is expected to grow at a constant rate of 5% forever. If the weighted average cost of capital is 14%, what is the firm's value of operations, in millions? Year: 1 2 Free cash flow: ($18) $40 (Round your answer to 2 decimal places.)arrow_forwardDaniel Sawyer, the CEO of the Sawyer Group, is initiating planning for the company's operations next year, and he wants you to forecast the firm's additional funds needed (AFN). The firm is operating at full capacity. Data for use in your forecast are shown below. Based on the AFN equation, what is the AFN for the coming year? Dollars are in millions. Last year's sales = S0 $350 Last year's accounts payable $40 Sales growth rate = g 30% Last year's notes payable $50 Last year's total assets = A0* $780 Last year's accruals $30 Last year's profit margin = PM 5% Target payout ratio 60%arrow_forwardA firm is considering a new inventory system that will cost $120,000. The system is expected to generate positive cash flows over the next four years in the amounts of $35,000 in year 1, $55,000 in year 2, $65,000 in year 3, and $40,000 in year 4. The firm’s required rate of return is 9%. What is the payback period of this project? 1.95 years 2.46 years 2.99 years 3.10 years Based on the information from Question 47. What is the net present value (NPV) of the project? $28,830.29 $30,929.26 $36,931.43 $39,905.28 Based on the information from Question 47, what is the internal rate of return (IRR) of this project? 14.03% 17.56% 19.26% 21.78% Based on the information from Question 47, what is the profitability index (PI) of this project? 0.87 1.11 1.31 1.83.arrow_forward

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education