ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

Transcribed Image Text:Expert Q&A

Done

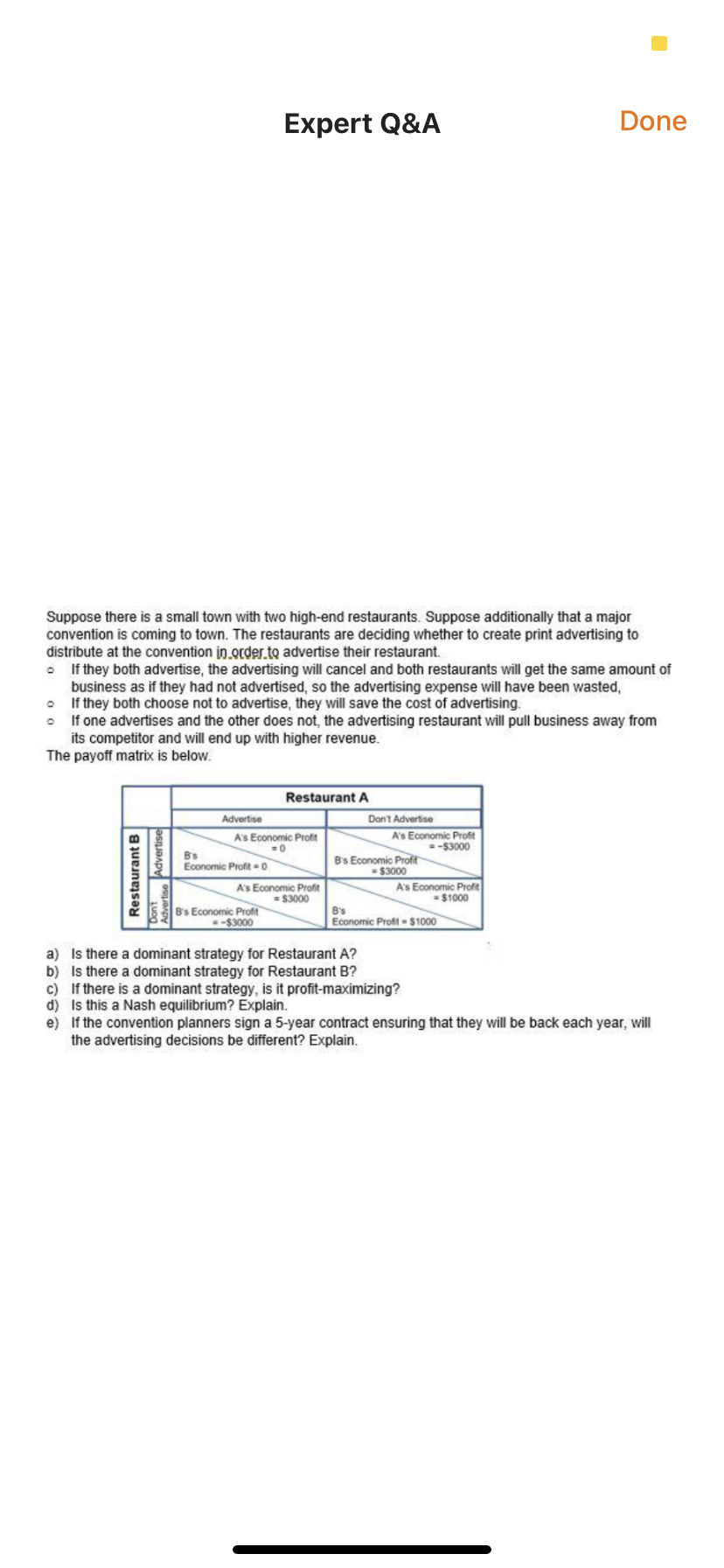

Suppose there is a small town with two high-end restaurants. Suppose additionally that a major

convention is coming to town. The restaurants are deciding whether to create print advertising to

distribute at the convention in.order.to advertise their restaurant.

If they both advertise, the advertising will cancel and both restaurants will get the same amount of

business as if they had not advertised, so the advertising expense will have been wasted,

If they both choose not to advertise, they will save the cost of advertising.

• If one advertises and the other does not, the advertising restaurant will pull business away from

its competitor and will end up with higher revenue.

The payoff matrix is below.

Restaurant A

Advertise

Dont Advertise

A's Economic Profit

=-$3000

A's Economic Profit

B's

Economic Profit = 0

B's Economic Profit

-$3000

A's Economic Profit

= $3000

A's Economic Profit

= $1000

B's Economic Profit

-$3000

B's

Economic Proft - $1000

a) Is there a dominant strategy for Restaurant A?

b) Is there a dominant strategy for Restaurant B?

c) If there is a dominant strategy, is it profit-maximizing?

d) Is this a Nash equilibrium? Explain.

e) If the convention planners sign a 5-year contract ensuring that they will be back each year, will

the advertising decisions be different? Explain.

Restaurant B

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 5 steps with 3 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- A small town has a duopoly in its tattoo market. Two firms, "Thread the Needle" and "Ink about it" are both competitors. Daily profit is listed in the payoff matrix. The green payouts belong to "Thread the Needle" and the red, "Ink about it". Why does the outcome where they both advertise yield the same profits for both firms than if they didn't advertise? A because advertising doesn't actually work B because advertising increases the average total costs and negatively impact total profit C because one firm is larger than the other firm D because of a collusive agreement between the firmsarrow_forward8. Collusive outcome versus Nash equilibrium Consider a remote town in which two restaurants, All-You-Can-Eat Café and GoodGrub Diner, operate in a duopoly. Both restaurants disregard health and safety regulations, but they continue to have customers because they are the only restaurants within 80 miles of town. Both restaurants know that if they clean up, they will attract more customers, but this also means that they will have to pay workers to do the cleaning. If neither restaurant cleans, each will earn $13,000; alternatively, if they both hire workers to clean, each will earn only $10,000. However, if one cleans and the other doesn't, more customers will choose the cleaner restaurant; the cleaner restaurant will make $18,000, and the other restaurant will make only $6,000. Complete the following payoff matrix using the information just given. (Note: All-You-Can-Eat Café and GoodGrub Diner are both profit-maximizing firms.) All-You-Can-Eat Café Cleans Up Doesn't Clean Up $ GoodGrub…arrow_forward4. Farmer Andy and Farmer Betty are the only two farmers that grow heirloom tomatoes for sale at the local farmer's market and compete as Cournot duopolists. The inverse demand curve for heirloom tomatoes at the market is P = 140 - 5Q where P is the %3D price per pound of tomatoes and Q is the number of pounds of tomatoes in hundreds per week; Q = qA + qB. Both Andy and Betty have a cost of growing tomatoes of w = 10, r = 20, and both have K = 1 in the short run. They both have a production function of q = L0.5KO.5. They will both earn profits of --.arrow_forward

- The table below shows the payoffs for two firms competing through advertisement. Firm A and Firm B can each choose to advertise, or to not advertise. A's Strategy Advertise Don't Advertise Table 14.2 B's Strategy Advertise A's profit $100 million B's profit $100 million A's profit $50 million B's profit $200 million What is Firm A's dominant strategy? Don't Advertise A's profit $200 million B's profit $50 million C. Advertise d. Firm A does not have a dominant strategy A's profit $75 million B's profit $75 million a. Don't advertise b. Indeterminate from this information, as no information is provided on Firm A's risk preference.arrow_forwardTwo duopolists are sharing a market in which they are contemplating whether to compete or to cooperate. If they cooperate and behave like a monopolist they will share the monopolist profit of $1800. If they compete each will get a profit of $800 but if one them cooperates while the other chooses to compete the one who cooperates gets $700 while the one who competes will end up with $1000. Set-up the game, explain the process and show the Nash-equilibrium reached when the game is played.arrow_forwardConsider an oligopolistic industry with N competing firms. Suppose that these firms have no fixed costs and that they all have the same marginal costs. Each firm must choose what quantity to produce independently of each other, and all firms must choose at the same time. If we decrease the number of firms in this industry (to, for example N−1), the market price Group of answer choices A. increases B. decreases C. remains unchanged D. becomes nil E. none of the abovearrow_forward

- Note:- Do not provide handwritten solution. Maintain accuracy and quality in your answer. Take care of plagiarism. Answer completely. You will get up vote for sure.arrow_forwardRestaurant B Advertise Don't Advertise 25 (A) Paragraph V 25 (B) 20 (A) 60 (B) Restaurant A Advertise a) Does Restaurant A have a dominant strategy? If yes, what is it? Explain. a) Does Restaurant B have a dominant strategy? If yes, what is it? Explain. B I U ✓ A 60 (A) 20 (B) 50 (A) 50 (B) GO Don't Advertise + < 11.arrow_forward14. Aside from advertising, how can monopolisticallycompetitive firms increase demand for their products? 17. Would you expect the kinked demand curve to bemore extreme (like a right angle) or less extreme (like anormal demand curve) if each firm in the cartel producesa near-identical product like OPEC and petroleum?What if each firm produces a somewhat differentproduct? Explain your reasoning.arrow_forward

- 24 If oligopolies compete hard against each other, which of the following will likely occur? A They will start acting like imperfect competitors. They will start acting like monopolistic competitors. The costs for all will be driven up. DO They will all experience zero profits.arrow_forwardF16arrow_forwardPlease no written by hand and no emagearrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education