ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

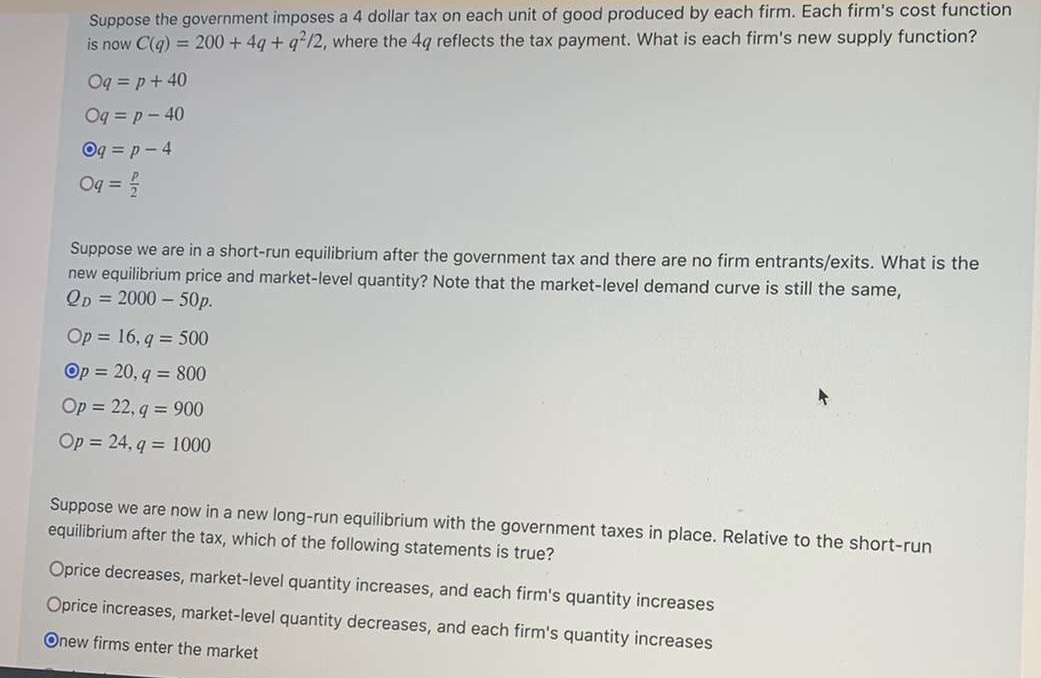

Transcribed Image Text:Suppose the government imposes a 4 dollar tax on each unit of good produced by each firm. Each firm's cost function

is now C(g) = 200 +4g + q*/2, where the 4q reflects the tax payment. What is each firm's new supply function?

Oq = p+ 40

Oq = p- 40

Og = p - 4

Oq =

Suppose we are in a short-run equilibrium after the government tax and there are no firm entrants/exits. What is the

new equilibrium price and market-level quantity? Note that the market-level demand curve is still the same,

Qp = 2000 – 50p.

Op = 16, q = 500

Op = 20, q = 800

Op = 22, q = 900

Op = 24, q = 1000

Suppose we are now in a new long-run equilibrium with the government taxes in place. Relative to the short-run

equilibrium after the tax, which of the following statements is true?

Oprice decreases, market-level quantity increases, and each firm's quantity increases

Oprice increases, market-level quantity decreases, and each firm's quantity increases

Onew firms enter the market

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- d) What will be the deadweight loss? e) What will be the firm’s maximum profits? f) How much would the firm would save in additional costs, if it had decided to supply all of that output at the point of equilibrium?arrow_forwardFind the consumer and producer surpluses by using the demand and supply functions, where p is the price (in dollars) and x is the number of units (in millions). Demand Function: p = 1220 − 21x Supply Function: p = 40xarrow_forwardDemand for apartments in town is D (x) =860 – 3x, and the supply is S (x) =500+9x, %3D where x is the number of apartments, in hundreds, and D (x) and S(x) are the rent in dollars per month, per apartment. The equilibrium point is (30, 770). Suppose a maximum rent of $644 per month is imposed by the town council. Find the deadweight loss. $ 1176 $ 1152 $ 16 $ 3072arrow_forward

- A perfectly competitive market is characterized by the following inverse demand function and inverse supply function where Q is output and P is the price in dollars. Demand: P = 100 – QD Supply: P = 10 + QS Suppose that a price ceiling of $30 is set by the government. Calculate the consumer surplus, the producer surplus, and the deadweight loss as a result of the government price ceilingarrow_forwardShow that any linear inverse supply that passes through the origin (i.e., an inverse supply with the functional form p = c Q with c > 0) has a price elasticity of supply equal to one. Show that any linear inverse supply curve with a positive intercept (i.e., having the functional form p = k + c Q with c, k > 0) must be elastic.arrow_forwardAssume the aggregate demand and supply of a good are given by: Qd(p)=16−p & Qs(p)=3p−4 a.) Where p equals the price of the good. If there are no taxes imposed on the consumption or production of the good, what will be the competitive equilibrium quantity?arrow_forward

- Caprica Corporation is a large conglomerate that has interests in various industries such as mining, oil refining, chemicals, and consumer goods. In the chemical industry, Caprica produces and sells Kalocin, a substance used in the production of most analgesic drugs. Caprica recently acquired the only firm that controls the extraction of a key raw material used to produce Kalocin. Jane Harris, an industry expert, expects the total surplus in the domestic market for Kalocin to fall following this acquisition. Her colleague, Brian Hall, disagrees. He feels that the acquisition will in fact increase efficiency in the market. Which of the following, if true, will most strengthen Jane's argument? O A. The net benefit accruing to Caprica will increase following the acquisition. ⒸB. Caprica's per-unit revenue before the acquisition was equal to the cost of producing an extra unit of Kalocin. O C. The demand for analgesic drugs is expected to increase in the coming year. O D. A Sri Lankan firm…arrow_forwardRent controls force landlords to price apartments below the equilibrium price level. An immediate effect is a shortage (excess demand) of apartments, because the quantity of apartments demanded is greater than the quantity supplied at the regulated price. When cities prevent landlords from charging market rents, which of the following are common long-run outcomes? Check all that apply. The future supply of rental housing units increases. Efficient use of housing space results. Nonprice methods of rationing emerge. The quantity of available rental housing units falls. Note:- Please avoid using ChatGPT and refrain from providing handwritten solutions; otherwise, I will definitely give a downvote. Also, be mindful of plagiarism. Answer completely and accurate answer. Rest assured, you will receive an upvote if the answer is accurate.arrow_forwardThe inverse supply function for coal is PS = 2 + QS. The inverse demand function for coal is PD = 20 - 2QD. By how much does consumer surplus increase when a $3 subsidy to consumption is introduced? (Assume that no tax was in place before the subsidy is introduced).arrow_forward

- qD = 100 – 0.5p, qS = 2p – 20 What is the price elasticity of supply? Is the situation modeled here more likely to be reflecting a short- or long-run equilibrium? Why?arrow_forwardSuppose that a certain product has the following demand and supply functions. Demand: Supply: p = -0.049 + 45 0.049 + 20 p = A $5 tax per item is levied. Determine the supply function when tax is added. p = Find the market equilibrium point after the tax. C (q, p) = =arrow_forwardRent controls force landlords to price apartments below the equilibrium price level. An immediate effect is a shortage (excess demand) of apartments, because the quantity of apartments demanded is greater than the quantity supplied at the regulated price. When cities prevent landlords from charging market rents, which of the following are common long-run outcomes? Check all that apply. The future supply of rental housing units increases. Efficient use of housing space results. Nonprice methods of rationing emerge. The quantity of available rental housing units falls. Step by step with explanation answer.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education