A First Course in Probability (10th Edition)

10th Edition

ISBN: 9780134753119

Author: Sheldon Ross

Publisher: PEARSON

expand_more

expand_more

format_list_bulleted

Related questions

Question

1

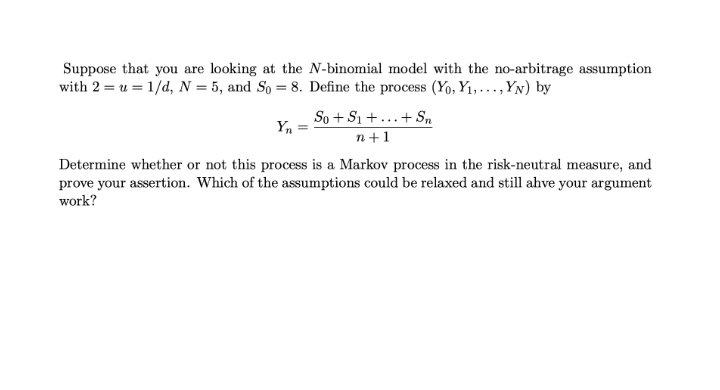

Transcribed Image Text:Suppose that you are looking at the N-binomial model with the no-arbitrage assumption

with 2 = u = 1/d, N = 5, and So = 8. Define the process (Yo, Y1,. .., YN) by

So + S1 +...+ Sn

n+1

Yn

Determine whether or not this process is a Markov process in the risk-neutral measure, and

prove your assertion. Which of the assumptions could be relaxed and still ahve your argument

work?

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps with 31 images

Knowledge Booster

Similar questions

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- A First Course in Probability (10th Edition)ProbabilityISBN:9780134753119Author:Sheldon RossPublisher:PEARSON

A First Course in Probability (10th Edition)

Probability

ISBN:9780134753119

Author:Sheldon Ross

Publisher:PEARSON