ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

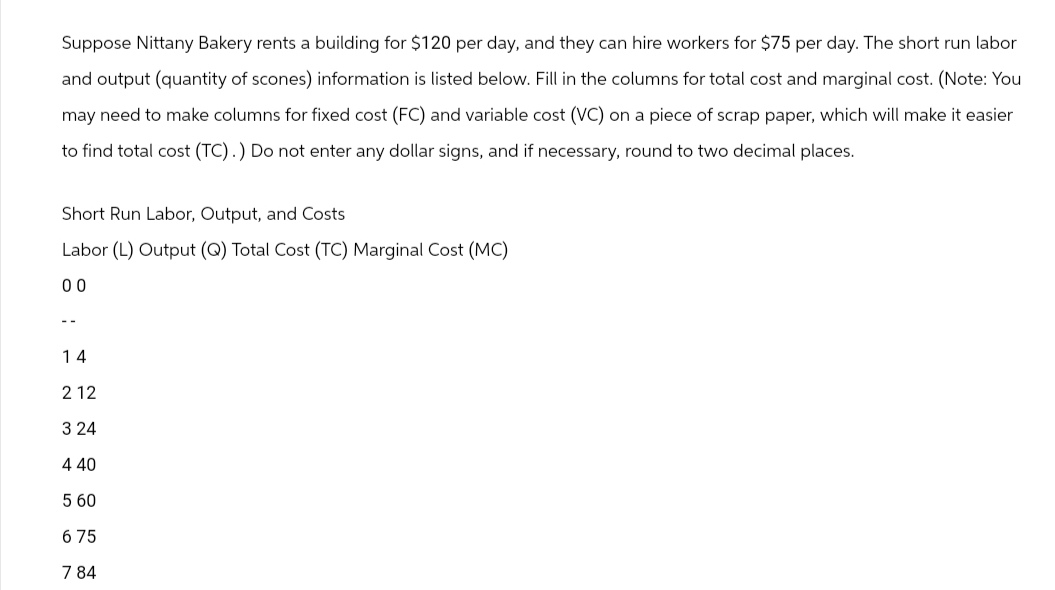

Transcribed Image Text:Suppose Nittany Bakery rents a building for $120 per day, and they can hire workers for $75 per day. The short run labor

and output (quantity of scones) information is listed below. Fill in the columns for total cost and marginal cost. (Note: You

may need to make columns for fixed cost (FC) and variable cost (VC) on a piece of scrap paper, which will make it easier

to find total cost (TC).) Do not enter any dollar signs, and if necessary, round to two decimal places.

Short Run Labor, Output, and Costs

Labor (L) Output (Q) Total Cost (TC) Marginal Cost (MC)

00

--

14

212

3 24

440

5 60

675

7 84

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps with 7 images

Knowledge Booster

Similar questions

- After running a successful pineapple business, Diddy looks for a new business venture. Now he wants to run gold mining business named "Diddy Bling Bling" which produces/sells raw gold. For simplicity, two types of inputs are required to produce raw gold (workers and gold mine). In short- run production, the size of gold mine is fixed while the number or workers can vary. After consulting his business consultant, Diddy computes the following cost table. The quantity of raw gold (kilograms) Averaged Total Cost (gold mine size=small) Averaged Total Cost (gold mine size-medium) Averaged Total Cost (gold mine size-Large) 1 700 1400 1800 2 600 1300 1700 3 500 1200 1600 4 400 1100 1500 5 300 1000 1400 6 400 900 1300 7 500 800 1200 8 610 600 1100 9 700 500 1000 10 800 400 900 11 900 375 800 12 1100 250 700 13 1200 400 600 14 1300 490 500 15 1400 600 400 16 1500 700 350 17 1600 800 300 18 1700 900 350 19 1800 1000 400 20 1900 1100 500 21 2000 1200 600 22 2100 1300 700 Draw Diddy Bling Bling's…arrow_forwardConsider the following cost function (C): C= 0.25q3 - 4q? + 75q + F. The equation for average cost (AC) is: AC = |. (Properly format your expression using the tools in the palette. Hover over tools to see keyboard shortcuts. E.g., a superscript can be created with the ^ character.) The equation for variable cost (VC) is: Vc=. (Properly format your expression using the tools in the palette.) The equation for marginal cost (MC) is: MC =. (Properly format your expression using the tools in the palette.)arrow_forwardAverage total cost decreases when marginal cost is average total cost. less than greater than equal toarrow_forward

- Craig and Javad run a paper company. Each week they need to produce 1,000 reams of paper to ship to their customers. The paper plant's longrun production function is Q = 4KL, where Q is the number of reams produced, K is the quantity of capital rented, and L is the quantity of labor hired. The weekly cost function for the paper plant is C = 20K + 4L, where C is the total weekly cost. (a) What ratio of capital to labor minimizes Craig and Javad's total costs? (b) How much capital and labor will Craig and Javad need to rent and hire in order to produce 1,000 reams of paper each week? (c) How much will hiring these inputs cost them?arrow_forwardQuestion 6: For each of the total cost functions, write the expressions for the average cost, average fixed cost, average variable cost, and marginal cost: 1. TC (Q) = 5Q 2. TC (Q) = 120 +6Q 3. TC (Q) = 6Q² 4. TC (Q) = 140 +5Q²arrow_forwardCalculate total costs at 4 units of output. Do not put a dollar sign in your answer. (The 6 columns are Quantity, Total Fixed Cost, Total Variable Cost, Total Cost, Average Total Cost, and Marginal Cost. The Quantity and Total Variable Cost columns have been filled in along with the first row for Total Fixed Cost. Average Total Costs and Marginal Costs are not calculated at a quantity of 0.) Quantity Total Fixed Cost Total Variable Cost Total Cost Average Total Cost Marginal Cost 0 15 0 XXXXX XXXXX 1 25 2 40 3 50 4 55 5 65 Calculate average total costs at 2 units of output. Calculate average total cost at 5 units of output. Calculate marginal cost at 4 units of output (moving from 3 units to 4 units). Can you tell if this is the short run or long run? Can you tell at which level of output profits will be maximized?arrow_forward

- Douglas Fur is a small manufacturer of fake-fur boots in New York City. The following table shows the company’s total cost of production at various production quantities.arrow_forwardIn Figure 2-a, the average variable cost curve is curve Group of answer choices A D C Barrow_forwardLet F be the fixed cost of production, let VC be the variable cost of production, C be the total cost, MC be the marginal cost, AFC, the average fixed cost, AVC, the average variable cost, and AC, the average cost. Complete the following cost table. (Enter numeric responses rounded to two decimal places.) Output (q) 1 2 3 4 5 6 7 8 9 10 F $250 250 250 250 250 250 250 250 250 с MC AFC AVC AC $266 $16 $250.00 $16.00 $266.00 12 125.00 14.00 139.00 8 83.33 12.00 4 62.50 10.00 72.50 298 50.00 59.60 8 310 12 41.67 10.00 51.67 76 326 35.71 10.86 46.57 96 346 20 12.00 43.25 41.11 27.78 13.33 120 370 24 148 28 25.00 14.80 VC $16 28 278 36 286 40 48arrow_forward

- Assume quantities need not be integers. Marginal cost is MC(q) = 6 + (9/10) * q. Total cost is TC = 456 at q=5. What is the fixed cost of production?arrow_forwardMarginal cost is defined as the change in total cost when: a) Total fixed cost increases b) Total variable cost decreases c) One more unit of output is produced d) Average cost decreasesarrow_forwardFor each lettered space in the following table, determine the appropriate dollar amount.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education