Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

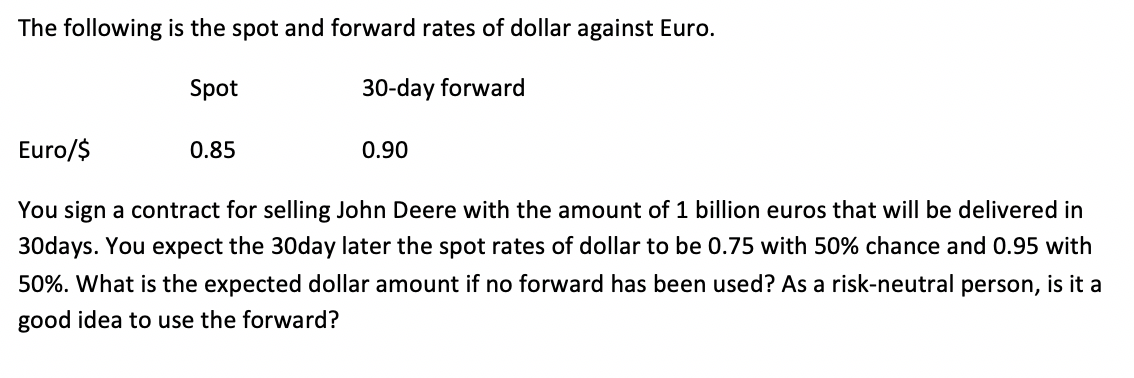

Transcribed Image Text:The following is the spot and forward rates of dollar against Euro.

Spot

30-day forward

Euro/$

0.85

0.90

You sign a contract for selling John Deere with the amount of 1 billion euros that will be delivered in

30days. You expect the 30day later the spot rates of dollar to be 0.75 with 50% chance and 0.95 with

50%. What is the expected dollar amount if no forward has been used? As a risk-neutral person, is it a

good idea to use the forward?

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- A software company Future PLC can invest in either Project C orProject D which have the same initial Year = 0 cost of £275mlm and cash-flows: Project C: £150mln (in Year=1), £250mln (in Year=2)Project D: perpetuity of £25mln (in Year=1) growing at an annual rateof g=7% The problem is, that the firm does not know the risk-adjusted discount rateof Project C but it does know that the cash flow betas are 55 (in Year=1) and 85 (in Year=2). It also knows that Project D has the same risk as a market portfolio, which has an annual return of rm = 15%. Risk-free treasury bonds have an annual return of rf = 5%. Which project should be chosen by the firm?arrow_forwardBak Assume that Richelle Corp imported goods from New York and needs 145,000 New York dollars 180 days from now. It is trying to determine whether to hedge its position. Richelle has developed the following probability distribution for the New York dollar Possible dollar value in 180 days HAE $.45 $0.40 $0.43 $0.51 $067 $0.81 $16.095 and 75% $4653 and 4.5% $3,789 and -89% Probability $3.356 and 35% 5% 10% 30% The 180-day forward rate of New York dollar is $0.63, and the spot rate is $0.59. Determine the expected additional cost of hedging. What is the probability that hedging will be more costly to the firm that not hedging? 30% 20% 5%arrow_forwardB. Projections for a new investment in lithium batteries are as follows: YEAR COST 0 1 2 3 4 01 5 6 £12,000 £0 £0 £0 £0 £0 BENEFIT £0 £2000 £4000 £6000 £6000 £2000 £0 £1000 What is the payback period on this investment?arrow_forward

- A. You want to invest in a riskless project in Sweden. The project has aninitial cost of SKr2.1 million and is expected to produce cash inflowsof SKr810,000 a year for 3 years. The project will be worthless afterthe first 3 years. The expected inflation rate in Sweden is 2 percentwhile it is 5 percent in the U.S. A risk-free security is paying 6percent in the U.S. The current spot rate is $1 = SKr7.55. What is thenet present value of this project in Swedish krona using the foreigncurrency approach? Assume that the international Fisher effect applies. B. In a recent e-news, you observe that the 6-month forward rate is $1.5031/ Euro. Further, if you invest the dollar, it fetches you interest atthe rate of 2% p.a. In comparison, the interest rate in Eurozone is 1%p.a. You also see that CAD 1.5513 are needed to purchase a Euro and CAD1.332 are needed to buy a US$. Is it possible for you to make an arbitrageprofit? If so, which of the arbitrage strategies will you employ andwhat will be…arrow_forwardA firm evaluates the following projects, when interest rates are 12% for every maturity: Year 0 1 2 с A B -200 -150 -50 150 125 40 150 125 30 If the projects are not mutually exclusive, the firm has a budget of $350 and you can take a project multiple times, what is the max value that you can bring to the firm? O a. $67 O b. O c. O d. O e. $124 Of $108 Og. $132 Oh. $122 $142 $115 $100arrow_forwardThe spot rate: USD 1.21/EUR 2-year USD YTM=0.11% 2-year EUR YTM= -0.72%. Suppose that you invest in the strategy known as the "carry trade". What will be your profit/loss if the spot rate in 2 years is USD 1.00/EUR. PROFIT = $1,100 or THERE IS NO ARBITRAGE OPPORTUNITY IS AN INCORRECT ANSWERarrow_forward

- Q1 Compare present value analysis, (minimum attractive rate of return is %8 annualy.) Alternative F Alternative Z First cost, TL Annual earning, TL Maintance cost every 5 year, 400.000 650.000 -same amount- wwww w 90.000 115.000 www m 25.000 30.000 TL Scrap value, TL lifetime, (years) 100.000 1.200.000 50 infinitearrow_forwardA. 6.36 The four alternatives described below are being evaluated. This question has three parts Part 2: If the proposals are mutually exclusive, which one should be selected at a MARR of 14.5% per year? Incremental Rate of Return, %, When Compared with Alternative Overall Initial Alternative Rate of A Investment, $ Return, % -60,000 11.7 -90,000 22.2 43.3 C -140,000 17.9 22.5 10.0 D -190,000 15.8 17.8 10.0 10.0 O B O A O C ODarrow_forwardM1arrow_forward

- Suppose that 1 Danish krone could be purchased in the foreignexchange market today for $0.16. If the krone appreciated 4% tomorrow against thedollar, how many krones would a dollar buy tomorrow?arrow_forwardPrblmarrow_forwardSub : FinancePls answer very fast.I ll upvote CORRECT ANSWER . Thank You A French company is considering a project in US. The project will cost $100M. The cash flows are expected to be $30M per year for 5 years. The current spot exchange rate is $1.20/ . The risk-free rate in the US is 1%, and the risk-free rate in Europe is 2%. The dollar required return on the project is 12%. Find the NPV in home currency using home currency approach. Please note correct answer is $7.1 million. please show detailed workings.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education