FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Topic Video

Question

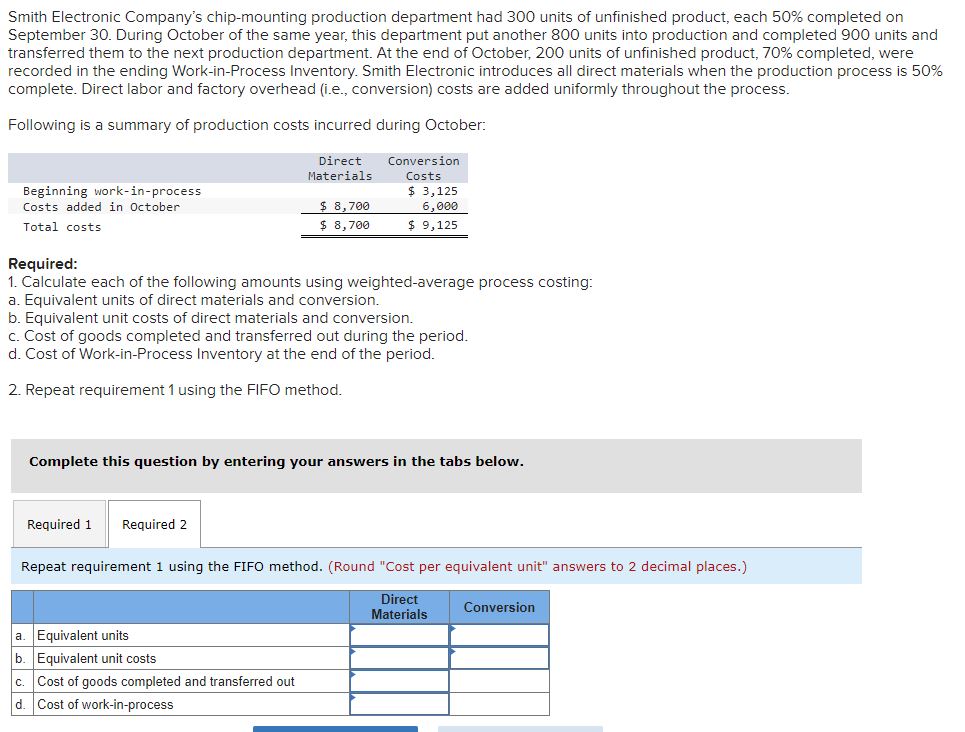

Transcribed Image Text:Smith Electronic Company's chip-mounting production department had 300 units of unfinished product, each 50% completed on

September 30. During October of the same year, this department put another 800 units into production and completed 900 units and

transferred them to the next production department. At the end of October, 200 units of unfinished product, 70% completed, were

recorded in the ending Work-in-Process Inventory. Smith Electronic introduces all direct materials when the production process is 50%

complete. Direct labor and factory overhead (i.e., conversion) costs are added uniformly throughout the process.

Following is a summary of production costs incurred during October:

Beginning work-in-process

Costs added in October

Total costs

Direct

Materials

Required 1 Required 2

$8,700

$8,700

Conversion

Costs

Required:

1. Calculate each of the following amounts using weighted-average process costing:

a. Equivalent units of direct materials and conversion.

b. Equivalent unit costs of direct materials and conversion.

c. Cost of goods completed and transferred out during the period.

d. Cost of Work-in-Process Inventory at the end of the period.

2. Repeat requirement 1 using the FIFO method.

a. Equivalent units

b. Equivalent unit costs

c. Cost of goods completed and transferred out

d. Cost of work-in-process

$ 3,125

6,000

$9,125

mplete this question by entering your answers in the tabs below.

Repeat requirement 1 using the FIFO method. (Round "Cost per equivalent unit" answers to 2 decimal places.)

Direct

Materials

Conversion

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 6 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Smith Electronic Company’s chip-mounting production department had 300 units of unfinished product, each 50% completed on September 30. During October of the same year, this department put another 900 units into production and completed 1,000 units and transferred them to the next production department. At the end of October, 200 units of unfinished product, 70% completed, were recorded in the ending Work-in-Process Inventory. Smith Electronic introduces all direct materials when the production process is 50% complete. Direct labor and factory overhead (i.e., conversion) costs are added uniformly throughout the process. Following is a summary of production costs incurred during October: Direct Materials Conversion Costs Beginning work-in-process $ 3,712 Costs added in October $ 9,900 6,400 Total costs $ 9,900 $ 10,112 Required: 1. Calculate each of the following amounts using weighted-average process costing:a. Equivalent units of direct materials and…arrow_forwardAt the start of June, the Polishing Department of Corona Counters, Inc. had 15,000 units in beginning inventory. During the month, it received 25,000 units from the Machining Department. It started and completed 17,000 units and transferred 32,000 units to the Packaging Department. It had 8,000 units in ending Work-in-Process Inventory. Direct materials are added at the beginning of the process. Units in beginning Work-in-Process Inventory were 50% complete in respect to conversion costs. Units in ending Work-in-Process Inventory were 40% complete with respect to conversion costs. Prepare the production cost report for the Polishing Department for the equivalent units of production for the month of June. Use the FIFO method.arrow_forwardSmith Electronic Company's chip-mounting production department had 300 units of unfinished product, each 50% completed on September 30. During October of the same year, this department put another 900 units into production and completed 1,000 units and transferred them to the next production department. At the end of October, 200 units of unfinished product, 70% completed, were recorded in the ending Work-in-Process Inventory. Smith Electronic introduces all direct materials when the production process is 50% complete. Direct labor and factory overhead (i.e., conversion) costs are added uniformly throughout the process. Following is a summary of production costs incurred during October: Beginning work-in-process Costs added in October Total costs Direct Materials $ 8,200 $ 8,200 Required: 1. Calculate each of the following amounts using weighted-average process costing: a. Equivalent units of direct materials and conversion. b. Equivalent unit costs of direct materials and conversion.…arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education