ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

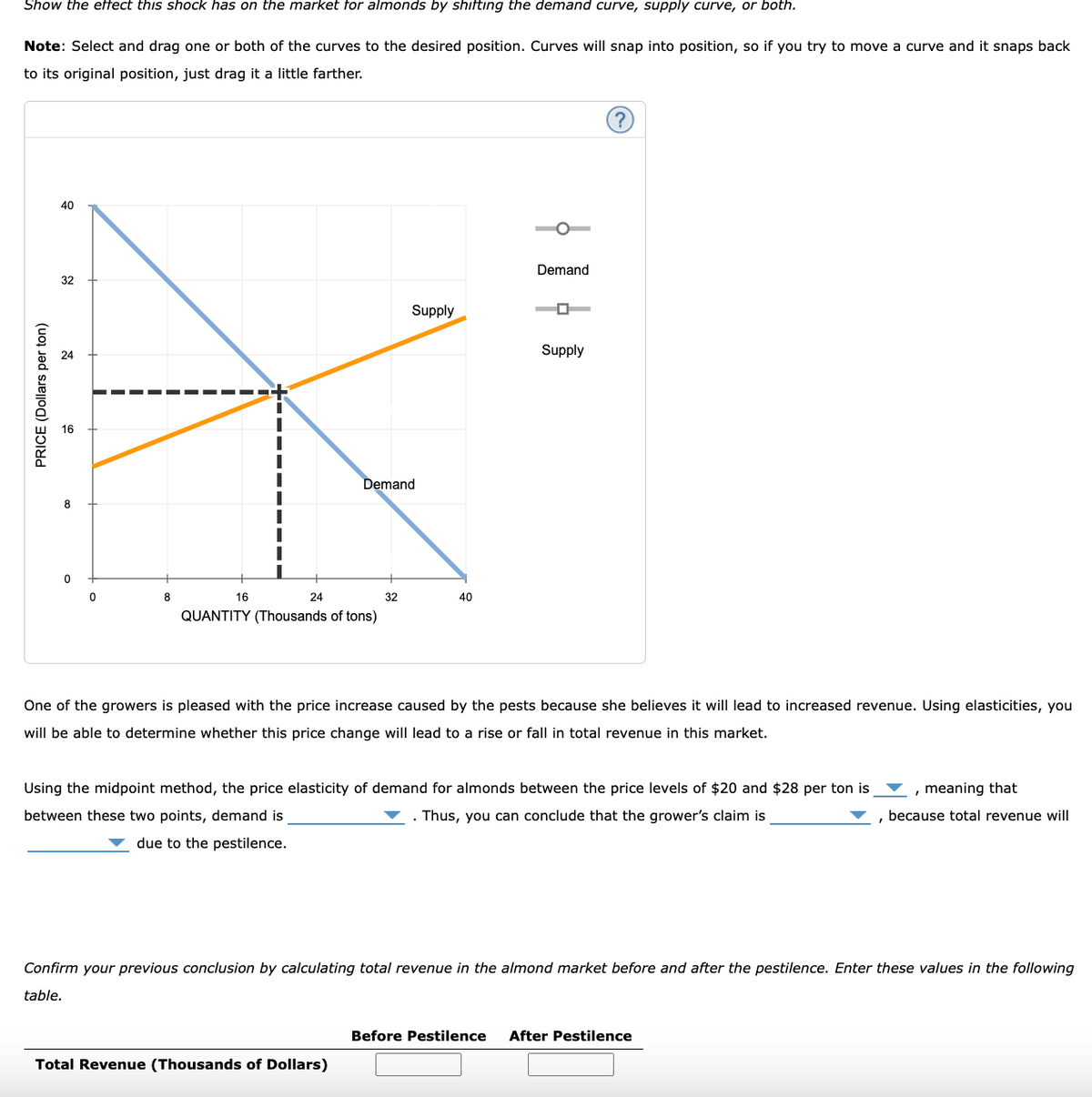

Transcribed Image Text:Show the effect this shock has on the market for almonds by shifting the demand curve, supply curve, or both.

Note: Select and drag one or both of the curves to the desired position. Curves will snap into position, so if you try to move a curve and it snaps back

to its original position, just drag it a little farther.

PRICE (Dollars per ton)

40

32

32

Supply

Demand

24

24

16

8

0

8

16

24

Demand

QUANTITY (Thousands of tons)

32

40

Supply

One of the growers is pleased with the price increase caused by the pests because she believes it will lead to increased revenue. Using elasticities, you

will be able to determine whether this price change will lead to a rise or fall in total revenue in this market.

Using the midpoint method, the price elasticity of demand for almonds between the price levels of $20 and $28 per ton is

between these two points, demand is

. Thus, you can conclude that the grower's claim is

due to the pestilence.

meaning that

because total revenue will

Confirm your previous conclusion by calculating total revenue in the almond market before and after the pestilence. Enter these values in the following

table.

Total Revenue (Thousands of Dollars)

Before Pestilence After Pestilence

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 1 steps with 1 images

Knowledge Booster

Similar questions

- If demand is elastic, a drought around the world would the total revenue that farmers receive from the sale of grain. Why would a drought only in Kansas most likely reduce the total revenues that Kansas farmers receive? A drought in Kansas would significantly raise the worldwide price of grain. A drought in Kansas would significantly lower the worldwide price of grain. OA drought in Kansas is not significant enough to affect the worldwide price of grain.arrow_forwarddemand of a product: q(p)= 10000 -1000ln(1+10)p please help in solving 1. how to compute the elasticity of demand when the price is $575 and 2. the decrease in demand in a % with 5 decimal places if the price goes up by 15%arrow_forwardPrice per Pound (dollars) $16 14 12 10 8 6 4 2 Quantity of Cheese Demanded (pounds) between $14 and $16 between $2 and $8 over the entire range of prices between $2 and $4 3 4 5 6 7 8 9 10 Refer to the table above, over what range of prices is the demand elastic?arrow_forward

- If the absolute value of the price elasticity of demand is 0.2, this means that: 1) a 20 percent decrease in price causes a 1 percent increase in quantity demanded 2) a 0.2 percent decrease in price causes a 1 percent increase in quantity demanded 3). a 5 percent decrease in price causes a 1 percent increase in quantity demanded 4) a 0.2 percent decrease in price causes a 0.2 percent increase in quantity demanded 5). a 100 percent decrease in price causes a 200 percent increase in quantity demandedarrow_forwardDemand and Supply Schedule for Good Y: Unit price of y Quantity demanded of y Quantity supplied of y Price elasticity of demand of y (2 decimals) Price elasticity of supply of y (2 decimals) $100 10 40 n/a n/a $90 11 35 $80 12 30 $70 13 25 $60 14 20 $50 15 15 $40 16 10 $30 17 5 $20 18 1 $10 19 0arrow_forwardCalculating elasticity Draw a set of coordinate axes on a piece of graph paper. Label the horizontal axis from 0 to 50 units and the vertical axis from $0 to $20 per unit. Draw a demand curve that intersects the vertical axis at $10 and the horizontal axis at 40 units. Draw a supply curve that intersects the vertical axis at $4 and has a slope of 1. Make the following calculations for these curves, using the midpoint formula: a. What is the price elasticity of demand over the price range $5 to $7? b. What is the price elasticity of demand over the price range $1 to $3?arrow_forward

- 22arrow_forwardA product costs $13. When the price increases by $4, the quantity demanded decreases by 20 units. Assuming that the price elasticity of demand is unitary when the price equals $13, calculate the corresponding quantity demanded. If the price has increased from $13 to $17, and the quantity demanded decreased by 20 units, calculate the percentage change in price:arrow_forwardA 30 %fall in the price of salt leads to 45 %rise in its demand. Calculate the price elasticity of demand. Comment on the commodity.arrow_forward

- Explain the concept of price elasticity of supply and its significance in determining how producers respond to changes in price. Discuss the implications of different price elasticities on market stability and the role of time in price elasticity.arrow_forwardIf the price elasticity of demand for a product is equal to 0.5 then a decrease in price of 10 percent will increase quantity demanded by A. 0.5 % B. 5 % C. 20 % D. 0.05 %arrow_forwardThe demand equation is 4,750,000 -1700P and the supply equation is -1,250,000 + 1300P. Solve for the equilibrium price and quantity.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education