ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

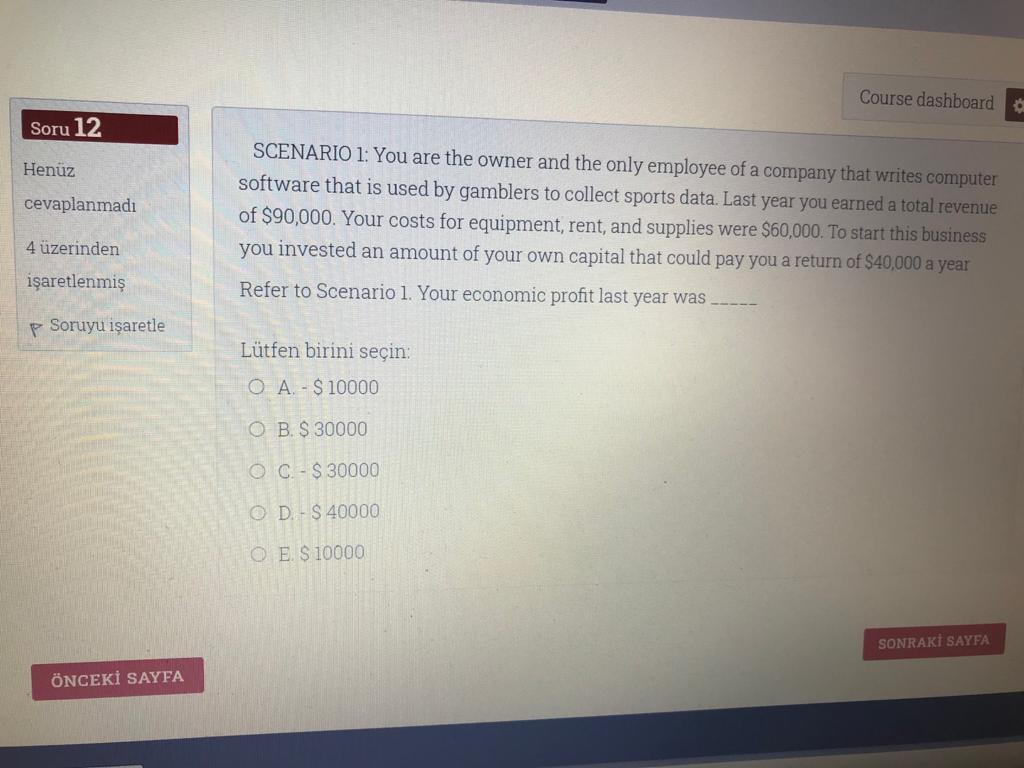

Transcribed Image Text:Course dashboard

Soru 12

SCENARIO 1: You are the owner and the only employee of a company that writes computer

software that is used by gamblers to collect sports data. Last year you earned a total revenue

Henüz

cevaplanmadı

of $90,000. Your costs for equipment, rent, and supplies were $60,000. To start this business

4 üzerinden

you invested an amount of your own capital that could pay you a return of $40,000 a year

işaretlenmiş

Refer to Scenario 1. Your economic profit last year was

P Soruyu işaretle

Lütfen birini seçin:

O A. - $ 10000

O B. $ 30000

O C -$ 30000

O D.-$ 40000

O E$10000

SONRAKİ SAYFA

ÖNCEKİ SAYFA

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Complete the following table by indicating key characteristics of each market structure. Market Structure Number of Firms Type of Product Entry Control of Price Monopoly Oligopoly Monopolistic Competition Perfect Competition For each of the following scenarios, determine which market structure best describes the scenario. Scenario Market Model Dozens of plain white socks producers use a widely known and readily available technology. Scholastic Inc. is the only company with the U.S. copyright to a popular series of books. Many small shops sell different styles of sweaters. Sweaters vary by price and quality. Four Internet providers offer similar services. Any new company would have to engage in a price war with the existing companies.arrow_forwardIn 1939, the box office records set by Gone with the Wind and The Wizard of Oz proved to Hollywood studios that investing in Technicolor was worth every penny. Nevertheless, a reversal of fortune hit the film industry as the United States entered World War II. Wartime shortages made celluloid nitrate more costly, so Hollywood studios reverted to primarily black and white. The few Technicolor musicals released only recovered their production costs. The graph shows Metro-Goldwyn-Mayer's (MGM) production of Technicolor movies before World War II. Modify the graph to describe the wartime period for MGM. Assume that nothing changes except the items discussed in the question.arrow_forwardAssume a firm's marginal costs are increasing at its current level of output. If a firm's marginal revenue is less than the marginal cost of producing the last unit of output chosen by the firm, then: Profits can be increased if the firm decreases output. The firm is certainly earning an economic profit but not as much as it could be. Profits can be increased if the firm increases output. The firm's economic profit is necessarily less than zero.arrow_forward

- Suppose that in 2018, you inherited from your grandfather a small planetarium that had been closed for several years. Your planetarium has a maximum capacity of 75 people and all the equipment is in working order. You decide to reopen the planetarium on the weekends as a new laser-tag venture called Shoot for the Stars, and much to your delight it has become an instant success, with admission tickets selling out quickly for each day you are open. Describe some of the decisions that you must make in the short run. What might you consider to be your “fixed factor”? What alternative decisions might you be able to make in the long run? Explainarrow_forwardThe Hokey Pokey, a children's day care center is thinking about changing the nature of its business. It is considering shutting down the day care center, and re-opening their business as an adult night club called the Hanky Panky. The Hokey Pokey currently makes $500 in profits. However, re-opening as the Hanky Panky will increase their profits from $500 to $1500. Friendly's Ice Cream which is currently located next to the Hokey Pokey is concerned because this move would reduce its profits by $1200. This would occur because they lose many of the families who currently come to the restaurant (some of which have their kids in the day care center.) but very few adult night club patrons are looking for ice cream According to economic theory, will the efficient outcome still likely occur, if there were many more surrounding stores with similar objections to the Hanky Panky? A) Yes, because the Coase Theorem will still apply as parties will bargain to the…arrow_forwardDesmond works as an accountant making $80,000 per year. He is considering leaving his job to open an artisanal cheese shop. He estimates that he will need to spend $20,000 per year on space, $10,000 per year on supplies and $40,000 per year on staff. The shop will earn will earn $120,000 per year in revenue. Assuming his estimates are accurate, what will Desmond's accounting profit be? Assuming his estimates are accurate, what will Desmond's economic profit be? Please enter your solution without commas, dollar signs, or cents.arrow_forward

- Looking at the Table, Profit, Cost and Revenue Functions, Quant is the quantity of output, C(Q) is the Total Cost of production for corresponding quantities of output, R(Q) is the corresponding Total Revenue at each level of output Q, if all output is sold and PRF(Q) is the Total Profit for each corresponding output level. PRF(Q) is calculated as R(Q)-C(Q). Using this information, does the company make its highest profit where R(Q) is highest? a. No, because the highest possible revenue may be at an output level where the cost of output may exceed the revenue generated at that output level. In this problem, the highest profit is at output level 15 Ob. Yes, because there is no way that cost can exceed revenue when revenue is maximized. Cc. No, because the highest possible revenue may be at an output level where the cost of output may exceed the revenue generated at that output level. In this problem, the highest profit is at output level 10 or 12 or in between. Od. Yes, because the…arrow_forwardNew entry increases your |e| from 2 to 5. If you previously maximized profits at a price of $16, your new profit maximizing is $10 $16 $8 $6.40 **please show your math**arrow_forward7arrow_forward

- Katie's Quilts is a small retailer of quilts and other bed linen products. Katie currently purchases quilts from a large producer for $100 each and sells them in her store at a price that does not change with the number of quilts that she sells. Katie is considering vertically integrating by making her own quilts. If the fixed cost of vertically integrating is $25,000 and she can produce quilts at Homework: Homework 7 (Lecture 6) Save Score: 0 of 1 pt 6 of 10 (8 complete) HW Score: 80%, 8 of 10 pts Text Question 4.2 Ques $50 per quilt, her total cost of producing quilts, q, herself is C=25,000+50q. How many quilts does Katie need to sell for vertical integration to be a profitable decision? For vertical integration to be profitable, Katie must sell at least nothing quilts. (Enter your response rounded to the nearest whole number.)arrow_forwardPQ 18.02 (and 18.03) Two businesses in a market can decide to increase the amount of stores they operate. If neither business adds new stores they will each earn $10 million in profit; if both add new stores they will each earn $4 million in profit; and if one adds new stores while the other does not, the business adding new stores earns profit of $10 million and the other earns profit of $5 million. If these businesses are not colluding we would expect: Select an answer and submit. For keyboard navigation, use the up/down arrow keys to select an answer. a both may or may not add new stores. b one business will add new stores and the other will not. c both will add new stores. d neither will add new stores.arrow_forwardEconomicsarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education