FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Topic Video

Question

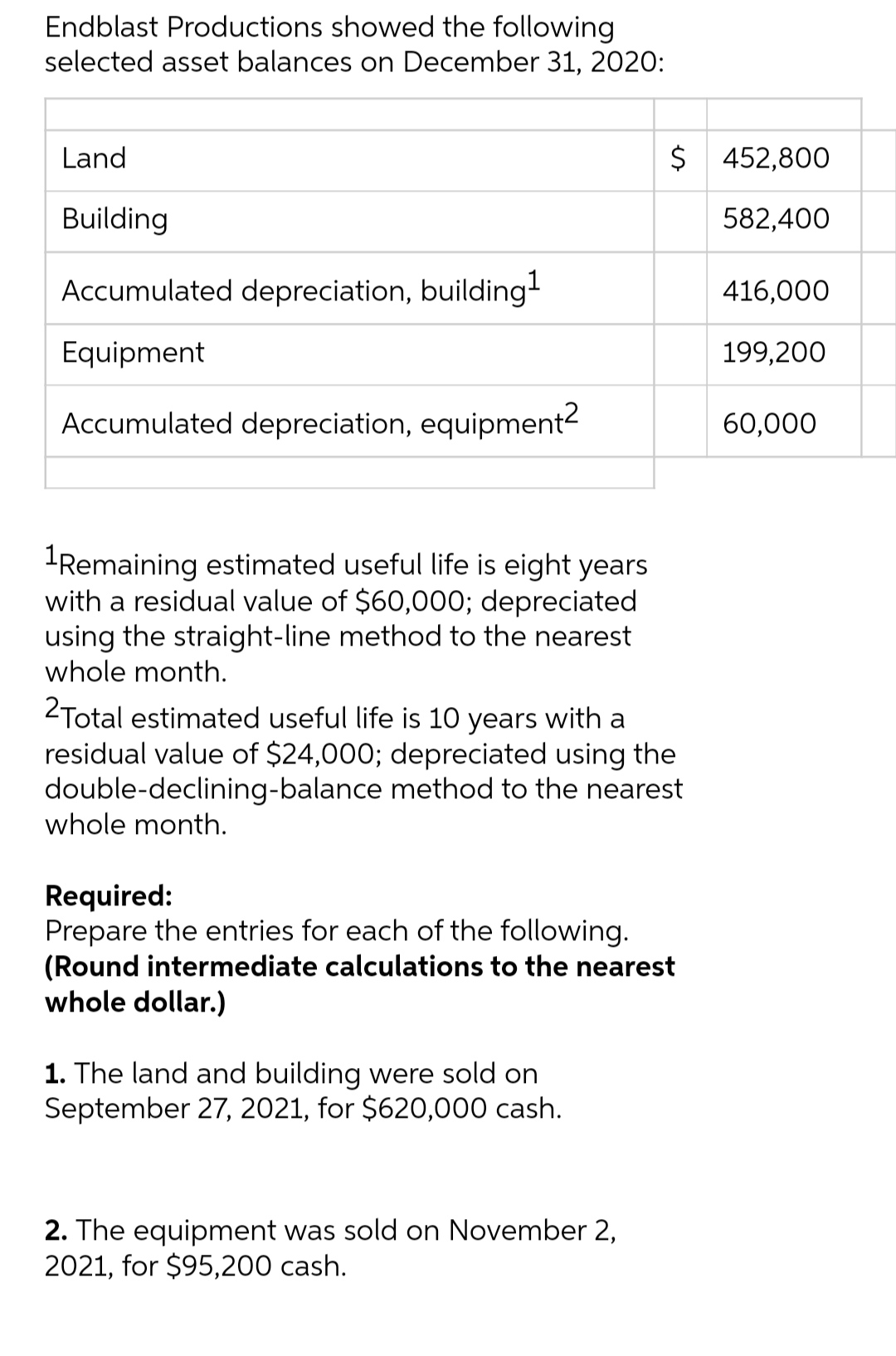

Transcribed Image Text:Endblast Productions showed the following

selected asset balances on December 31, 2020:

Land

Building

Accumulated depreciation, building¹

Equipment

Accumulated depreciation, equipment²

1Remaining estimated useful life is eight years

with a residual value of $60,000; depreciated

using the straight-line method to the nearest

whole month.

2Total estimated useful life is 10 years with a

residual value of $24,000; depreciated using the

double-declining-balance method to the nearest

whole month.

Required:

Prepare the entries for each of the following.

(Round intermediate calculations to the nearest

whole dollar.)

1. The land and building were sold on

September 27, 2021, for $620,000 cash.

2. The equipment was sold on November 2,

2021, for $95,200 cash.

$ 452,800

582,400

416,000

199,200

60,000

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Funseth Farms Inc. purchased a tractor in 2018 at a cost of $34,800. The tractor was sold for $3,400 in 2021. Depreciation recorded through the disposal date totaled $30,000. (1) Prepare the journal entry to record the sale. (2) Now assume the tractor was sold for $11,200; prepare the journal entry to record the sale. (If no entry is required for a transaction/event, select "No journal entry required" in the first account field.) View transaction list Journal entry worksheet 2 Record the sale of the tractor for $3,400. Note: Enter debits before credits. Event 1 Record entry General Journal Clear entry Debit Credit View general journal >arrow_forwardTacurong, a resident citizen, won $1,000,000 from the US lottery. Is the lottery winning subject to final tax of 20%? Yes or No?arrow_forward1arrow_forward

- 7. On January 1, 2020 Gingerbread, Corp. purchased a reindeer merry-go-round as an attraction to draw customers during the holiday season. The following information is available: Invoice price $280,000 Shipping cost $4,000 Set-up cost $2,000 Insurance to cover years 2020 and 2021 $12,000 Necessary repair during set-up 500 Determine the amount to be record as the capitalized cost of the asset. a.286,000 b.280,000 c.286,500 d.298,500arrow_forwardOn March 1, 2021, Sage Hill Company acquired real estate on which it planned to construct a small office building. The company paid $100,000 in cash. An old warehouse on the property was razed at a cost of $7,900; the salvaged materials were sold for $1,800. Additional expenditures before construction began included $1,400 attorney's fee for work concerning the land purchase, $4,100 real estate broker's fee, $8,200 architect's fee, and $13,600 to put in driveways and a parking lot. Determine the amount to be reported as the cost of the land. Cost of the land $arrow_forwardVaughn Corporation owns machinery that cost $26,000 when purchased on July 1, 2021. Depreciation has been recorded at a rate of $3,120 per year, resulting in a balance in accumulated depreciation of $10,920 at December 31, 2025. The machinery is sold on September 1, 2026, for $6,760. Prepare journal entries to (a) update depreciation for 2026 and (b) record the sale. (Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter O for the amounts. List all debit entries before credit entries.) No. Account Titles and Explanation (a) (b) Debit Creditarrow_forward

- Dengerarrow_forwardOn May 1, 2020, Vaughn Manufacturing began construction of a building. Expenditures of $620400 were incurred monthly for 5 months beginning on May 1. The building was completed and ready for occupancy on September 1, 2020. For the purpose of determining the amount of interest cost to be capitalized, the weighted-average accumulated expenditures on the building during 2020 were O $2481600. O $3102000. O $517000. O $620400.arrow_forwardRayya Company purchases a machine for $151,200 on January 1, 2021. Straight-line depreciation is taken each year for four years assuming a seven-year life and no salvage value. The machine is sold on July 1, 2025, during its fifth year of service. Prepare entries to record the partial year’s depreciation on July 1, 2025, and to record the sale under each separate situation. (1) The machine is sold for $64,800 cash. (2) The machine is sold for $51,840 cash. 1. Record the depreciation expense as of July 1, 2025. 2. Record the sale of the machinery for $64,800 cash. 3. Record the machine sold for $51,840 cash. Note:- Do not provide handwritten solution. Maintain accuracy and quality in your answer. Take care of plagiarism. Answer completely. You will get up vote for sure.arrow_forward

- Following are descriptions of land purchases in four separate cases. Requireda. Determine the cost used for recording the land acquired in each case.b. Record the journal entry for each case on the date of the land’s acquisition. Note: Round your answers to the nearest whole dollar. Case One 1. At the midpoint of the current year, a $32,000 check is given for land, and the buyer assumes the liability for unpaid taxes in arrears of $800 at the end of last year and those assessed for the current year of $720. a. Determine the cost used for recording the land acquired.Cost of land $Answer b. Record the journal entry on the date of the Account NameDr.Cr. Answer Answer Answer To record land acquisition.arrow_forwardAt December 31, 2025, Blue Corporation reported the following plant assets. Land Buildings Less: Accumulated depreciation-buildings Equipment Less: Accumulated depreciation-equipment Total plant assets During 2026, the following selected cash transactions occurred. Apr. May June Date 1 Purchased land for $3,335,200. 1 Sold equipment that cost $909,600 when purchased on January 1, 2019. The equipment was sold for $257,720. 1 Sold land for $2,425,600. The land cost $1,516,000. July 1 Purchased equipment for $1,667,600. Dec. 31 Retired equipment that cost $1,061,200 when purchased on December 31, 2016. No salvage value was received. April 1 $26,520,000 11,934,000 60,640,000 7,580,000 May 1 Journalize the transactions. (Hint: You may wish to set up T-accounts, post beginning balances, and then post 2026 transactions.) Blue uses straight-line depreciation for buildings and equipment. The buildings are estimated to have a 40-year useful life and no salvage value; the equipment is estimated…arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education