ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

{kind=link}

Question

Referring to question 1: The amount of producer surplus in this market is $_____. Make sure you round your answer to two decimal places (and include the decimal point and two decimal places to the right in your answer, and if your answer requires a comma, put the comma in the appropriate place).

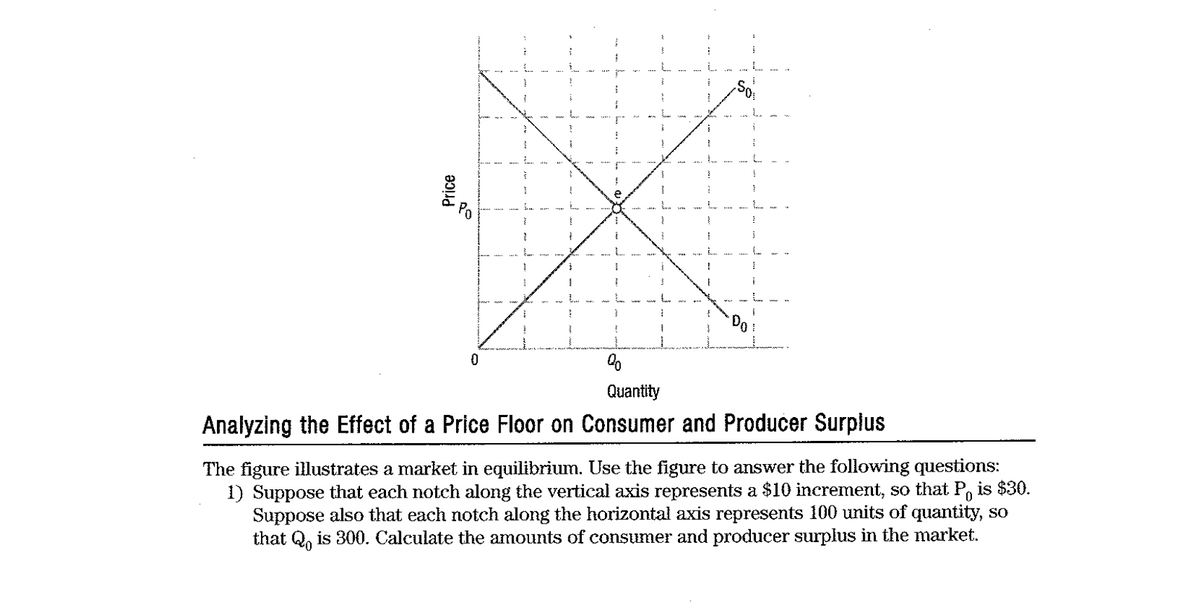

Transcribed Image Text:**Analyzing the Effect of a Price Floor on Consumer and Producer Surplus**

The figure illustrates a market in equilibrium. Use the figure to answer the following questions:

1) Suppose that each notch along the vertical axis represents a $10 increment, so that \( P_0 \) is $30. Suppose also that each notch along the horizontal axis represents 100 units of quantity, so that \( Q_0 \) is 300. Calculate the amounts of consumer and producer surplus in the market.

**Graph Explanation:**

- The graph features a standard supply and demand curve intersecting at a point marked \( (Q_0, P_0) \), suggesting market equilibrium.

- The vertical axis represents price, with \( P_0 \) labeled as the equilibrium price.

- The horizontal axis represents quantity, with \( Q_0 \) labeled as the equilibrium quantity.

- The supply curve is labeled as \( S_0 \) and slopes upward.

- The demand curve is labeled as \( D_0 \) and slopes downward.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Consider a market where demand and supply satisfy the following equations QD = 12 – 2 P,e Qs = 2P. a) Find the current equilibrium price and quantity. b) What is the total producer surplus if the market is in equilibrium? - The government is considering a minimum price policy to increase producer surplus.- c) Explain by means of graphs how the introduction of a price floor can increase producer surplus. d) Find the (optimal) price floor that maximizes producer surplus.arrow_forwardCan you help me with this please? Can you explain how to factor in consumer and producer surpluses With substitute and complement goods? arrow_forwardUSE TABLE #1: The calculation you used to find the producer surplus for the efficient market for electric automobiles is 1/2 x ($ ____________ - $__________ ) x ( _____ - ________ ). (Remember to use a comma, if a comma is needed and to include the decimal point and two numbers to the right of the decimal point).arrow_forward

- Please refer to the image below and answer question 10arrow_forwardPlease refer to the image below and answer question 13arrow_forwardUsing Supply and Demand to Analyze Markets-End of Chapter Problem Increases in demand generally result in increases in consumer surplus. However, this is not always the case. Of the following scenarios, which one is most likely to result in a decrease in consumer surplus? Supply is relatively elastic, and demand becomes highly inelastic when it increases. Supply and demand are both unit elastic and demand increases. Supply is inelastic, and demand becomes highly elastic when it increases. O Supply is relatively elastic, and demand becomes highly elastic when it increases.arrow_forward

- The standard measure of consumer surplus is a fair measure of the value of a good to consumers because it gives an equal weight to each individual consumer.” Is this statement true, false, or uncertain?arrow_forwardThe figure to the right illustrates the market for apples in which the government has imposed a price floor of $14 per crate. How many crates of apples will be sold after the price floor has been imposed? 14 million crates of apples per year. (Enter your response as an integer.) Will there be a shortage or surplus? If there is a shortage or surplus, how large will it be? There will be a surplus of 18 million crates of apples per year. (Enter your response as an integer.) Will apple producers benefit from the price floor? O A. Apple producers who are able to sell their apples at the $14 price per crate will benefit. O B. Apple producers who are not able to sell their apples will not benefit. O C. Total revenue for apple producers as a group will decrease from $220 million to $196 million. O D. Both a and b. O E. All of the above. Price 20- 18- 16- 14 12- 10- 8- 6- 4- 2- 0- 0 Supply Demand 4 8 12 16 20 24 28 32 36 40 Quantity (millions of crates per year)arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education