ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

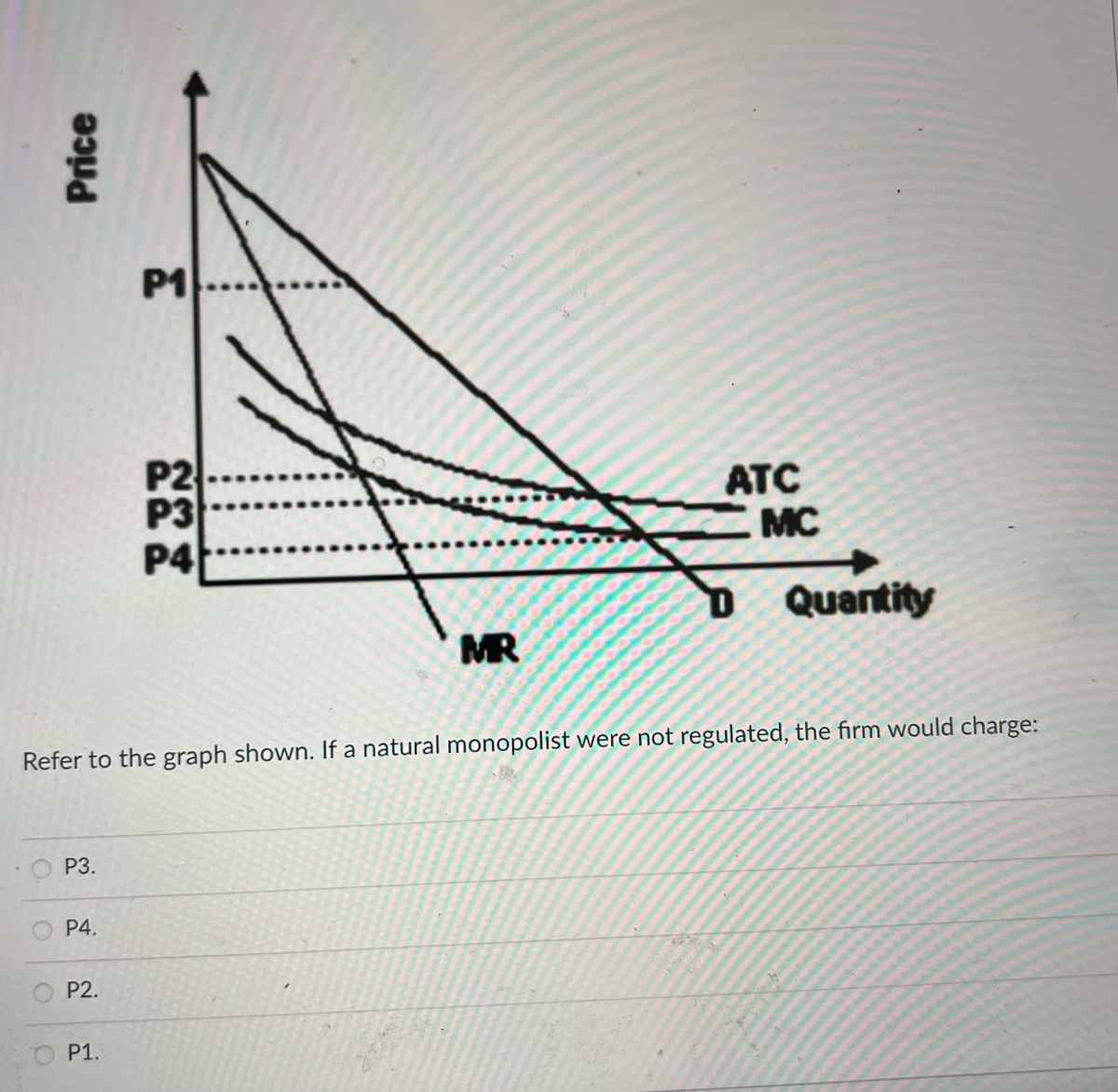

Transcribed Image Text:Price

P1

P2

P3

P4

Quantity

MR

Refer to the graph shown. If a natural monopolist were not regulated, the firm would charge:

P3.

P4.

P2.

P1.

ATC

MC

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- 5arrow_forwardThere is an unregulated firm with a natural monopoly. The table below shows quantity of goods to be produced, price, total revenue, total cost, marginal revenue, marginal cost, and average cost. Quantity Price Total Revenue Marginal Revenue Total Cost Marginal Cost Average Cost 11 $18.00$18.00 $18.00$18.00 $18.00$18.00 $17.00$17.00 $17.00$17.00 22 $17.00$17.00 $34.00$34.00 $16.00$16.00 $33.00$33.00 $16.00$16.00 $16.50$16.50 33 $15.00$15.00 $45.00$45.00 $11.00$11.00 $45.00$45.00 $12.00$12.00 $15.00$15.00 44 $12.00$12.00 $48.00$48.00 $3.00$3.00 $55.00$55.00 $10.00$10.00 $13.75$13.75 55 $10.00$10.00 $50.00$50.00 $2.00$2.00 $63.00$63.00 $8.00$8.00 $12.60$12.60 66 $8.00$8.00 $48.00$48.00 −$2.00−$2.00 $70.20$70.20 $7.20$7.20 $11.70$11.70 77 $6.50$6.50 $45.50$45.50 −$2.50−$2.50 $77.00$77.00 $6.80$6.80 $11.00$11.00 88 $5.00$5.00 $40.00$40.00 −$5.50−$5.50 $84.80$84.80 $7.80$7.80 $10.60$10.60 Determine how many goods the…arrow_forwardMONOPOLISTIC COMPETITION 1. Suppose that the cost of production is given by the following function: CT = 100 + Q2 and that the demand is given by P = 80 - Q. a. Determine the level of maximization.b. Determine the value of CT and ITc. Check that the IMg = CMg CT (Total cost) IMg (marginal income) CMg (marginal cost) Algebraically if the demand curve in the monopoly is a function of quantity, the demand curve is a straight line. P = a - bQWhere a is the ordinate to the origin, b the slope and Q the quantitySo if IT = P x QWe have that (a - bQ) Q = aQ - bQ2IT = aQ - bQ2And therefore the marginal income is the derivative of IT or what is equal to the variation of total income between the variation of the quantity.Therefore the IMg = derive the quantity in the function aQ - bQ2IMg = a - 2bQ Consider these functions when conducting monopoly exercises.arrow_forward

- microeconomicsarrow_forwardThe figure shows what type of market? >>Please add an explanation of how natural monopoly differs in graph vs. normal monopoly.arrow_forward16 The following table shows a monopolist's demand curve and the cost information for the production of its good. What will their profits equal? Quantity Price per Unit Total Cost 10 $100 $100 20 $80 $400 30 $60 $800 40 $40 $1,400 50 $20 $2,400 A $1,000 BO $1,600 CO $1,200 DO $800arrow_forward

- I know that profit maximization for both a competitive and monopolistic market is MC=MR, however MR=P is applicable only in a competitive market and this is a monopoly. How do I solve this?arrow_forward1) Are monopolists guaranteed of making economic profits?. pleas explain.2) Explain the long run equilibrium situation for a monopolistically competitive industry. Give two examples of industries that fit under this category.arrow_forwardThere is an unregulated firm with a natural monopoly. The table below shows quantity of goods to be produced, price, total revenue, total cost, marginal revenue, marginal cost, and average cost. Quantity Price Total Revenue Marginal Revenue Total Cost Marginal Cost Average Cost 11 $15.00$15.00 $15.00$15.00 $15.00$15.00 $14.00$14.00 $14.00$14.00 22 $14.00$14.00 $28.00$28.00 $13.00$13.00 $26.00$26.00 $12.00$12.00 $13.00$13.00 33 $13.00$13.00 $39.00$39.00 $11.00$11.00 $36.00$36.00 $10.00$10.00 $12.00$12.00 44 $12.00$12.00 $48.00$48.00 $9.00$9.00 $44.00$44.00 $8.00$8.00 $11.00$11.00 55 $10.20$10.20 $51.00$51.00 $3.00$3.00 $47.00$47.00 $3.00$3.00 $9.40$9.40 66 $8.90$8.90 $53.40$53.40 $2.40$2.40 $51.00$51.00 $4.00$4.00 $8.50$8.50 77 $7.00$7.00 $49.00$49.00 −$4.40−$4.40 $56.00$56.00 $5.00$5.00 $8.00$8.00 88 $5.40$5.40 $43.20$43.20 −$5.80−$5.80 $62.00$62.00 $6.00$6.00 $7.75$7.75 Determine how many goods the firm will…arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education