ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

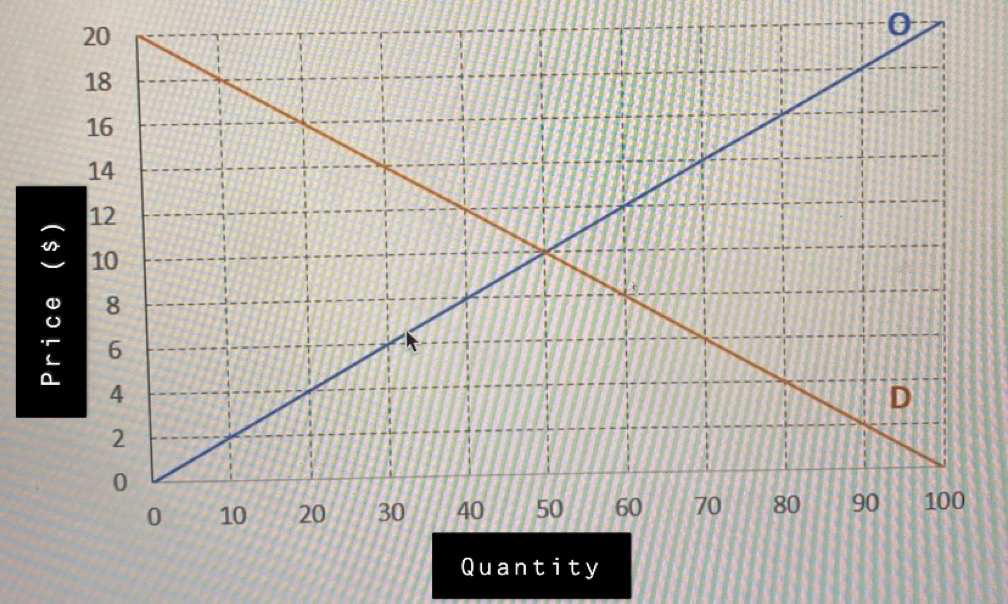

Refer to the figure below. What will happen if the market price is $14?

a) There will be a shortage of 20 units and producers will increase their

Production

• b) There will be a shortage of 40 units and producers will increase their

Production

• c) There will be a surplus of 40 units and prices will decrease

• d) There will be a surplus of 20 units and prices will decrease

Transcribed Image Text:Price ($)

20

18

16

14

12

10

8

6

4

2

0

0

10

20

30

40

50

Quantity

60

70

80

D

100

90

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- The table shows the demand and supply schedules for tacostacos. If the quantity demanded of tacos decreases by 400 per hour at each price, the new price of a taco is $2.00. Total surplus decreases by $_____?. Price (dollars per taco) Quantity demanded Quantity supplied (tacostacos per hour) 0 800 0 1.00 700 100 2.00 600 200 3.00 500 300 4.00 400 400 5.00 300 500 6.00 200 600 7.00 100 700 8.00 0 800 Note:- Do not provide handwritten solution. Maintain accuracy and quality in your answer. Take care of plagiarism. Answer completely. You will get up vote for sure.arrow_forwardAnswer The correct answer is: 375 The graph shows the schedule for hours of tutoring in economics. Price (per hour of tutoring) $25 20 15 10 7.50 2.50 100 200 300 400 500 600 700 800 900 Quantity (hours of tutoring per week) If the price increases from the equilibrium price of $10 to $15, total surplus will decrease, in numerals, byarrow_forwardNonearrow_forward

- You are given the following market data for Venus automobiles in Saturnia. Demand: P = 35,000 - 0.5Q Supply: P = 8,000 + 0.25Q where P = Price and Q = Quantity. a. b. C. Calculate the equilibrium price and quantity. Calculate the consumer surplus in this market. Calculate the producer surplus in this market. Use the editor to format your answerarrow_forwardHomework 2 Q1) Assume a market of a specific good. The demand and supply equation is as shown below: Pp = 70 – 3QD Ps = 5 + 2Qs Find the equilibrium price 2. Find the equilibrium quantity 3. Find the demand price elasticities at the equilibrium 1. 4. Find the supply price elasticities at the equilibrium 5. Find the Consumer Surplus 6. Find the Producer Surplusarrow_forwardA baker will supply 17 jumbo cinnamon rolls to a cafe at a price of $3.91 each. If she is offered $3.15, then she will supply 4 fewer rolls to the cafe. The cafe's demand for jumbo cinnamon rolls is given by p = D(x) = -0.48x + 8.05. What is the equilibrium point? ___ rolls at a price of $ ___ eacharrow_forward

- This is the market for HOT CHOCOLATE, which is a normal good and is produced with cocoa beans. We know that hot tea is a substitute for hot chocolate and whipped cream is a complement. Quantity Surplus or Price Quantity Supplied Demanded Shortage $5 6,000 10,000 $4 8,000 8,000 $3 10,000 6,000 $2 12,000 4,000 $1 14,000 2,000 1. Complete the table above finding a Shortage or a Surplus. Draw a graphical illustration of the market and find the equilibrium price and equilibrium quantity. For the remaining questions, explain by words or show graphically how equilibrium price and equilibrium quantity of hot chocolate would change (due to changes in Supply or Demand) if: 2. The price of cocoa beans falls; 3. The price of tea falls; 4. Consumer income falls because of a recession.arrow_forwardOver the past few year's consumer tastes and the number of buyers in the market for a game called 'pickle ball' have increased dramatically. Thus, the demand for tickets to pickle ball events has increased. Before this all started the equilibrium price of a ticket to a pickle ball event was negative. This means that: A few years ago, there would have been a surplus of tickets even at a price of zero, now the invisible hand has pushed prices to greater than zero. A) A few years ago, the quantity of tickets demanded was less than quantity supplied. B) Pickle ball event tickets resembled the market for recyclable cardboard a few years ago C) Greater demand for pickle ball tournament tickets will lead to a greater demand - and higher pay - for professional pickle ball players. D) All of the above. E) B and D onlyarrow_forwarda) In the market for sugary drinks, the current equilibrium price is $10 and the equilibrium quantity is 30. The demand choke price is $50 and the supply choke price is $5 (a) Draw a demand and supply diagram, and shade the regions that represent consumer and producer welfare. Calculate the Total welfare in this market b) In this market, you now know that E D = −0.4 and E S = 1.2. Redraw your diagram in part (a) with the correct sloping curves. In this part you do not have to shade the welfare regions. All you need to do is redraw the diagram with the same equilibrium price and quantity, and choke prices but adjust the slope of each curve to reflect their respective elasticity c) If a tax was to be implemented in this market, what percentage of the burden is borne by the buyer? d) The government plans to discourage the consumption of sugary drinks and as such, they implemented a $1 tax on every bottle produced. In this situation, the suppliers are taxed directly but they hope to pass…arrow_forward

- In a market, if the price of a good is set below the equilibrium price, what will happen? a) Shortage b) Surplus c) Equilibrium d) Price ceilingarrow_forward01. What would be the impact in this market, of a price floor set at $10 a) A market surplus of 7 b) A market surplus of 10 c) A market surplus of 21 d) There would be no impact e) A market shortage of 7 f) A market shortage of 10 g) A market shortage of 21 02. What would be the impact in this market, of a price floor set at $13 a) A market surplus of 7 b) A market surplus of 10 c) A market surplus of 21 d) There would be no impact e) A market shortage of 7 f) A market shortage of 10 g) A market shortage of 21arrow_forwardIf the economy goes into a recession and incomes fall, what happens in markets? Prices of inferior goods go up because the demand for them increases Prices of normal goods go up because the demand for them increases Prices of all goods go down None of the other answers is correct Suppose the demand curve is given by P=10-Q and the supply curve by Q=P If the price in the market is given by $7, then The market is in equilibrium There is a a surplus in the market There is a shortage in the market Increasing the price will result in an increase in the quantity demandedarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education