ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

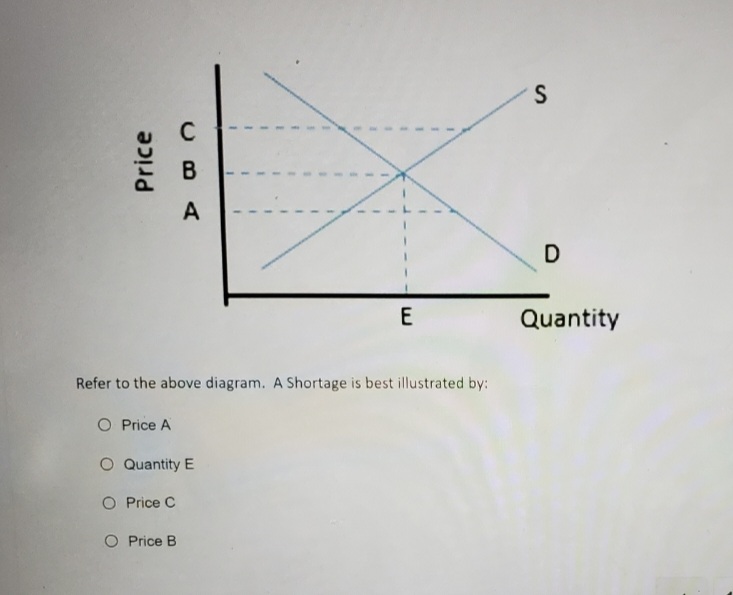

Transcribed Image Text:Price

C

B

A

Refer to the above diagram. A Shortage is best illustrated by:

O Price A

O Quantity E

O Price C

O Price B

E

S

D

Quantity

Expert Solution

arrow_forward

Step 1

Market equilibrium refers to the set of economic variables (often price and quantity) that the economy is generally driven toward by supply and demand. The concept of economic equilibrium can also be used to describe a wide range of elements, including interest rates or overall consumer spending. The point of equilibrium denotes a theoretical state of rest where all economic activities that "should" occur have actually happened, given the initial conditions of all significant economic variables.

Step by stepSolved in 4 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- The graph shows the market for concert tickets. Draw a horizontal line at a price at which there is a shortage of concert tickets. Label it Price. Draw an arrow that shows the amount of the shortage. When does a shortage occur? How does the price change to reach equilibrium? A shortage occurs at a given price when The price to reach equilibrium. O A. supply is greater than demand; falls B. the quantity demanded is greater than the quantity supplied; rises OC. demand is greater than supply, rises OD. the quantity supplied is greater than the quantity demanded; falls 600- 500- 400- 300- 200 100- 10- 0 Price (dollars per ticket) Quantity (millions of concert tickets per year) D (6,100) >>> Draw only the objects specified in the question. L Carrow_forwardThe following supply and demand schedule provides data regarding Burger King's Whopper burgers. Plot the supply and demand curves and answer the questions below. Whopper Burgers Price Quantity Demanded Quantity Supplied 4 7. 4 6. 2 What would explain a new equlibrium price and quantity at 7 dollars for 4 Whoppers? a. The price of ground beef increases twofold X b. Burger King engineers invent a new flame broiler that it three times more efficient at cooking burger patties C. Another Baby Boom occurs in the aftermath of the COVID pandemic d. The price of Big Macs drops significantly N Oarrow_forwardExplain how each of the following events changes the demand for or supply of jeans. A. People's incomes increase. B. A new technology becomes available that reduces the time it takes to manufacture a pair of jeans. C. The price of the cloth (denim) used to make jeans falls. D. Jeans come back into fashion. E. The price of a pair of jeans falls. F. The wage rate paid to garment workers rises. G. Many jeans producers go out of business. H. The price of a denim skirt halves. A. Event G decreases supply and event H increases demand. B. Event B decreases supply and event G increases demand. O C. Event C increases demand and event D increases supply. D. Event E increases demand and event F decreases supply. OE. Event A increases demand and event B increases supply.arrow_forward

- 24 of 100 Suppose that there is a freeze in California that damages the avocado crop. The effect on the market for avocados will be a in the equilibrium price. of the supply curve and a(n). DOOO leftward shift; decrease leftward shift; increase a rightward shift; increase rightward shift; decreasearrow_forwardDescribe how the change in price affect the quantity demanded, draw a demand curve on price-quantity plane and show the movement.arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education