ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

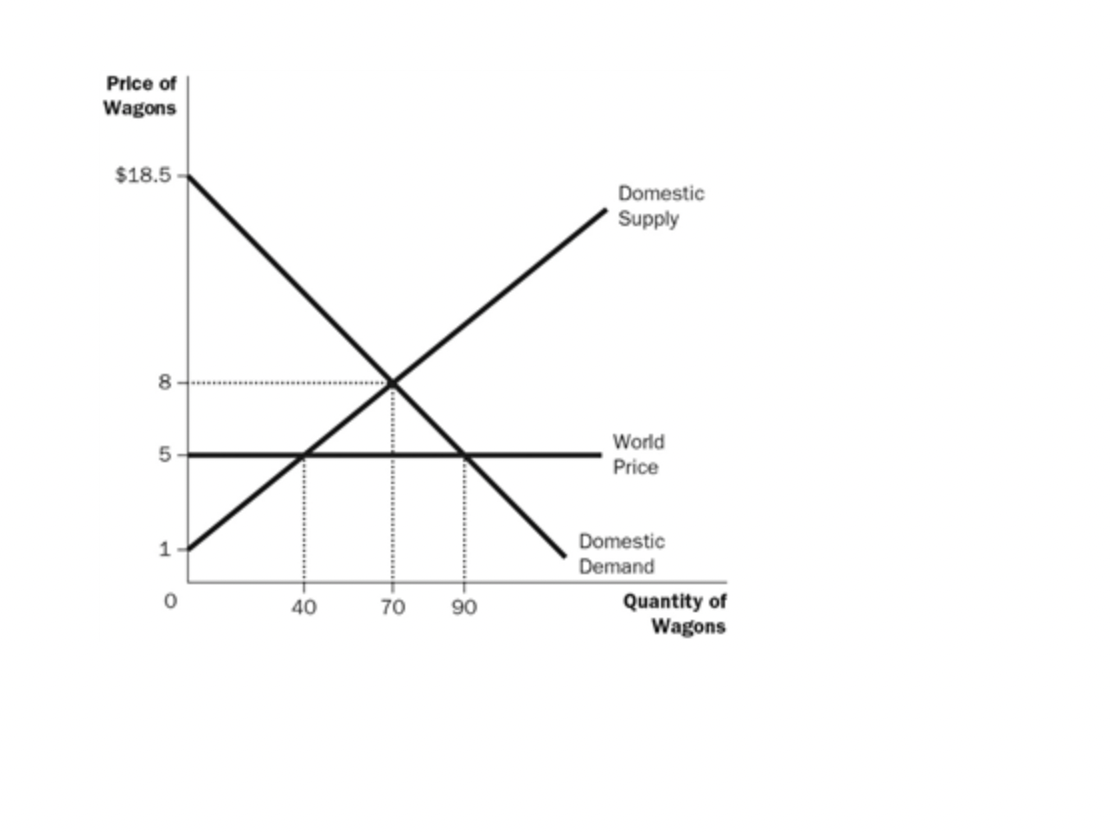

Transcribed Image Text:Price of

Wagons

$18.5

8

5

1

0

х

40

70

90

Domestic

Supply

World

Price

Domestic

Demand

Quantity of

Wagons

Transcribed Image Text:Refer to Figure 9-6. With free trade, what would producer surplus be?

$200

$160

$150

Another value (not listed here)

$80

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Price (dollars per sandwich) 0 | 2345678 2 5 6 7 Quantity supplied (sandwiches per week) 0 Quantity demanded 400 350 300 250 200 150 100 50 0 50 100 150 200 250 300 350 400 2. Calculate the Consumer Surplus and Producer Surplus generated by this market for sandwiches.arrow_forwardFigure 7-8 Price Equilibrium price A B C D Q₁ E F G Equilibrium quantity Supply Demand Quantityarrow_forwardQuestion 2: Suppose Qd= 100- 10P Qs = 10P a. Draw a graph using the supply and demand equation assuming no trade. Calculateequilibrium P, Q, consumer, producer and total surplus. b. Draw another graph assuming that trade is allowed. Calculate quantity domesticallyconsumed, domestically produced, imports, consumer surplus, producer surplus assumingworld price =$3. c. What happens to consumer surplus and producer surplus after trade? Does total surplusincrease or decrease after trade? Show your calculations. i need the the diagramarrow_forward

- Assume that a price floor of $320 has been implemented and there are no wasteful quality improvements. What are the total gains from trade (total surplus) with a price floor of $320? Hint: enter your answer as a number only with no $ sign Example: if the answer is $10,000, enter 10,000 2,400arrow_forwardSituation 4-1 During the winter of 1973-74, a general system of wage and price controls (including a price ceiling on gasoline) was in force in the United States. At the beginning of 1974, some oil-producing countries imposed an oil embargo (a legal prohibition on commerce) on the West. In the spring of 1974, price controls were abolished. Refer to Situation 4-1. If no price controls had been in place, the effect of the oil embargo on the equilibrium price and quantity of gasoline would have been a. an increase in price and a decrease in quantity. b. an increase in both price and quantity. c. a decrease in both price and quantity. d. a decrease in price and an increase in quantity.arrow_forwardSuppose Home is a small exporter of wheat. At the world price of 100 US dollars per tonne, Home growers export 20 tons of wheat. Now suppose the Home government decides to support its domestic producers with an specific export subsidy of 40 US dollars per tonne. Use Figure 1 to answer the following questions: Figure 1: Supply and Demand for Wheat at Home Home price 140 100 X 10 20 40 50 Supply Demand Quantity (a) Explain why consumer and producer surplus can be used to gauge the change in welfare caused by the export subsidy on individuals and firms.arrow_forward

- Refer to the table below. (2) Minimum Acceptable (1) Person Price Carlos Courtney Chuck Cindy Craig Chad $ 3 4 5 6 7 8 (3) Actual Price (Equilibrium Price) $7 7 7 7 7 7 If the six people listed in the table are the only producers in the market, and the equilibrium price is $7, how much producer surplus will the market generate? Instructions: Enter your answer as a whole number. Total producer surplus = $arrow_forwardThe price of green grapes increases from $1.90 to $2.30 per pound. When this happens, the amount of grapes sold drops from 500 pounds to 400 pounds. Assuming that the demand and supply of grapes held steady, what is the value of the loss of consumer surplus that occurred? $160 $40 $180 $200arrow_forwardMarkets are said to generate a benefit to society in the form of "gains from trade." These gains from trade can be calculated in the form of ___ A. the total surplus.B. the bargaining agreement.C. the producer surplus.D. the consumer surplus.arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education