ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

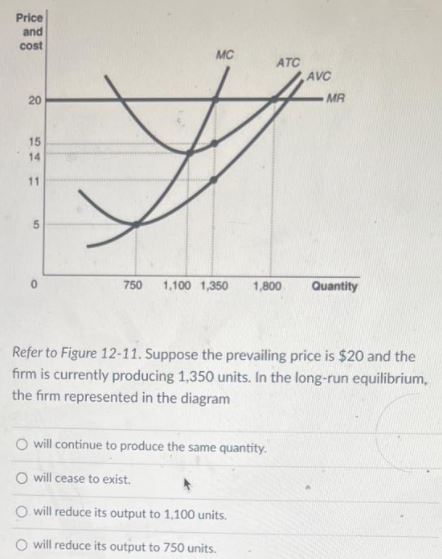

Transcribed Image Text:Price

and

cost

MC

ATC

AVC

20

MR

15

14

11

750

1,100 1,350

1,800

Quantity

Refer to Figure 12-11. Suppose the prevailing price is $20 and the

firm is currently producing 1,350 units. In the long-run equilibrium,

the firm represented in the diagram

will continue to produce the same quantity.

O will cease to exist.

O will reduce its output to 1,100 units.

O will reduce its output to 750 units.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Suppose that the perfectly competitive tuna Industry is In long-run equilibrium at a price of $3 per can of tuna and a quantity of 600 million cans per year. Suppose the Surgeon General Issues a report saying that eating tuna is bad for your health. The Surgeon General's report will cause consumers to demand Shift the supply curve, the demand curve, or both on the following diagram to illustrate these short-run effects of the Surgeon General's announcement. Note: Select and drag one or both of the curves to the desired position. Curves will snap into position, so if you try to move a curve and it snaps back to its original position, just drag it a little farther. Supply X Demand 400 600 800 QUANTITY (Millions of cans) 0 0 In the long run, some firms will respond by 5 0 200 0 200 Demand 1000 Shift the supply curve, the demand curve, or both on the following diagram to Illustrate both the short-run effects of the Surgeon General's announcement and the new long-run equilibrium after firms…arrow_forwardthe orange square points on the marginal cost curve from low to high(16,12) (24,20),(30,36),(32,44),(34,52),(38,72)arrow_forwardLasguns are produced by identical firms in a perfectly competitive market. Each firm's Total Cost function is TC=579+12q+q^2 and Marginal Cost function is MC=12+2q. What quantity does each firm produce in the long-run equilibrium?arrow_forward

- Consider what happens in the long run when demand falls in a constant cost industry. For instance, think about the market for pizza in a small city after the city's biggest textile mill shuts down. The accompanying graph begins in a long-run equilibrium. Move the appropriate curve or curves on the graph to illustrate the fall in demand and the resulting change that returns the market to long-run equilibrium. Finally, move point E to the new equilibrium position. Price of pizza Market for Pizza E Also, answer the following questions about the market's response to this fall in demand. a. The marginal cost of production is lowest at the short-run equilibrium b. When firms cut prices, they often do so in dramatic ways. The local pizza shops are most likely to offer "Buy one, get one free" in the short-run equilibrium c. The market price is less than the firm's average cost of production in the .The market price is equal to the average cost of production in the d. Restating the previous…arrow_forwardConsider the perfectly competitive market for copper. Assume that, regardless of how many firms are in the Industry, every firm in the industry is Identical and faces the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph. COSTS (Dollars per pound) PRICE (Dollars per por 100 90 80 70 60 50 40 30 20 100 10 50 0 80 70 60 50 40 30 20 10 0 The following diagram shows the market demand for copper. 0 Use the orange points (square symbol) to plot the initial short-run industry supply curve when there are 20 firms in the market. (Hint: You can disregard the portion of the supply curve that corresponds to prices where there is no output since this is the Industry supply curve.) Next, use the purple points (diamond symbol) to plat the short-run industry supply curve when there are 30 firms. Finally, use the green points (triangle symbol) to plot the short-run Industry supply curve when there are 40 firms. MC D 0 5 10 ATC H AVC D 0 15…arrow_forwardOperation managementarrow_forward

- After serving as President of the United States for eight years, Dena has retired from politics and has decided to become a wheat farmer. The market for wheat is perfectly competitive and the current market price for wheat is $10 per bushel. Dena is currently producing 8 bushels (Dena can only produce this good in whole units). Her total cost at 8 units of output is $88 and her variable cost at 8 units of output is $64. Dena knows that if she produces a 9th unit her total cost will become $97, and if she produces a 10th unit her total cost will become $110. Dena’s goal is to maximize her profits. Based on this information, identify whether each of the following would be true or false and briefly explain your reasoning. Dena is currently losing money in the short-run and she would be better off if she shutdown and produced zero. Dena is not currently profit maximizing at 8 units of output and she could increase her profits if she expanded output by one unit. Dena would increase her…arrow_forwardpshotic 166& 5. Profit maximization and shutting down in the short run Suppose that the market for microwave ovens is a competitive market. The following graph shows the daily cost curves of a firm operating in this market. 100 90 80 ATC 70 60 40 30 AVC 20 10 MC 5 10 15 20 25 30 35 40 45 50 QUANTITY (Thousands of ovens) Σ 50 PRICE (Dollars per oven)arrow_forward7. Short-run supply and long-run equilibrium Consider the perfectly competitive market for steel. Assume that, regardless of how many firms are in the industry, every firm in the industry is identical and faces the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph. COSTS (Dollars per ton) 100 90 80 70 60 50 40 ATC 30 20 10 + MC AVC 0 0 5 10 15 20 25 30 35 40 45 50 QUANTITY OF OUTPUT (Thousands of tons) The following diagram shows the market demand for steel. ⑦? Use the orange points (square symbol) to plot the short-run industry supply curve when there are 20 firms in the market. (Hint: You can disregard the portion of the supply curve that corresponds to prices where there is no output since this is the industry supply curve.) Next, use the purple points (diamond symbol) to plot the short-run industry supply curve when there are 30 firms. Finally, use the green points (triangle symbol) to plot the short-run industry…arrow_forward

- Long Run Equilibrium Consider a perfect competitive market with n identical firms. The cost functions of an individual firm are: The market demand is given by TC=q³ - 4q² + 74q MC=3q² - 8q+74. P= 120-Q a) In the above space draw two graphs one for the market and one for the firm to show the long run equilibrium b) In the long run, each firm will produce q.. i.e. the firm is operating at its minimum c) The long run equilibrium price must be P=. d) Thus the total amount purchased will be Q= e) This means there is enough room for n=. f) No more entry will take place because.. g) Show all equilibrium values on your graph ..firms Because. because..arrow_forwardShow what happens in the short run on both graphs when a new medical study shows soybeans to be highly carcinogenic. On the market graph, you will shift a curve or curves. On the firm's graph, use Price 2 to draw a new price line for the firm. On both graphs, indicate the new equilibrium point with point B. Now, show the changes that get both graphs back to long‑run equilibrium. Use shift(s) for the market and Price 3 for the firm. Indicate the new long‑run equilibrium with point C.arrow_forwardConsider the following figure for a perfectly competitive firm. Price, Costs MC K ATC E F AVC R J P = MR Q1 Q2 Q3 Q4 Q5 Output The figure above shows a perfectly competitive firm. To maximize profits or minimize losses, the firm will produce units and its profit/loss is given by Q3; Area of the rectangle JEKQ Zero ; Area of the rectangle IEKM Q3; Area of the rectangle JIMQ Zero ; Area of the rectangle JEKQarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education