MATLAB: An Introduction with Applications

6th Edition

ISBN: 9781119256830

Author: Amos Gilat

Publisher: John Wiley & Sons Inc

expand_more

expand_more

format_list_bulleted

Related questions

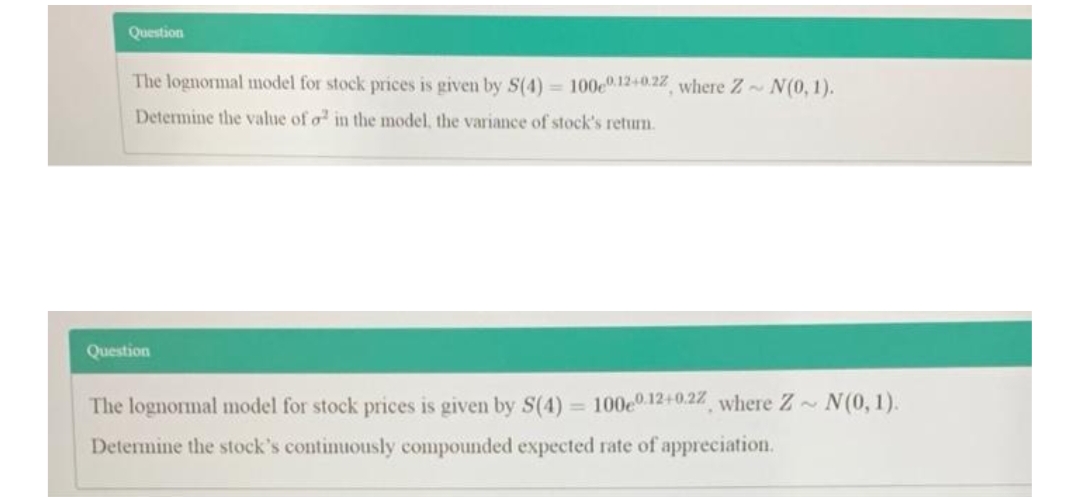

Question

Transcribed Image Text:Question

The lognormal model for stock prices is given by S(4) = 100e12+0.22, where Z N(0, 1).

Determine the value of o in the model, the variance of stock's retum.

Question

The lognormal model for stock prices is given by S(4) = 100e0 12+0.22 where Z N(0, 1).

%3D

Determine the stock's continuously compounded expected rate of appreciation.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Similar questions

- A survey was conducted and asked: "Do you consider your health to be poor?" This was coded as 1 for "yes" and 0 for "no." The effect of age (in years) and sex (1 male, 0 = female) on the outcome was examined using logistic regression. The fitted logistic model is: = logit(ô) = −0.544 + ß * sex + 0.0331 * age (a) What are the odds of responding "yes" for a female subject who is 60 years old? (b) What is the estimated odds ratio corresponding to the age variable? Interpret this estimate. (c) Suppose that, based on the data from the survey, the odds of responding "yes" for males are 3.79% greater than the odds for females, adjusting for age. What is the value of Â? (d) If we only wanted to assess the association between survey response (yes/no) and sex, what other method(s) (that we have learned in this class) could we have used (name at least one)? In your own words, explain why we cannot use the same method(s) if we want to consider the effects of both sex and age on survey response.arrow_forwardWhat do you mean by Generalized method of moments? illustrate regression model with exogenous variables Z?arrow_forwardun a regression analysis on the following data set, where yy is the final grade in a math class and xx is the average number of hours the student spent working on math each week. hours/weekx Gradey 8 55.2 8 62.2 8 53.2 10 70 13 83.2 15 78 17 100 18 87.2 20 100 20 100 State the regression equation with constants accurate to 2 decimal places.ˆyy^ = x + What is the predicted value for the final grade when a student spends an average of 7 hours each week on math?arrow_forward

- Log(Wagei) = α + β1Educationi + β2Femalei + β3Non Whitei + β4Educationi × Femalei + εi For males, and holding other variables constant, the regression output from the linear regression model above implies that an extra year of education is associated with what percent change in wages?arrow_forwardWhat happened to the standard error of educ after adding KWW to the model? Discuss. Do you agree or disagree with the following statement? “If the log of the dependent variable appears in the regression, changing the unit of measurement of any independent variable affects both the slope and intercept coefficients”. Discuss by providing the resource.arrow_forwardSuppose you obtain the following regression model, E[y]=20+53*x +33*x^2. What is the impact of a 63 unit change of x on the expected value of y when x is at its mean of 54?arrow_forward

- Which of the following is FALSE? * The residuals in a regression model are assumed to have a zero mean. Data point below the regression line, the residual is negative. The residuals in a regression model are assumed to have increasing mean. The regression model assumes the residuals are normally distributed.arrow_forward(15) 5. (TRUE, FALSE) In regression, the coefficient of determination gives the proportion of the variability in the dependent variable that is explained by the regression equation.arrow_forwardSuppose you obtain the following regression model, E[y]=20+47*x +88*x^2. What is the impact of a 64 unit change of x on the expected value of y when x is at its mean of 57?arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- MATLAB: An Introduction with ApplicationsStatisticsISBN:9781119256830Author:Amos GilatPublisher:John Wiley & Sons Inc

Probability and Statistics for Engineering and th...StatisticsISBN:9781305251809Author:Jay L. DevorePublisher:Cengage Learning

Probability and Statistics for Engineering and th...StatisticsISBN:9781305251809Author:Jay L. DevorePublisher:Cengage Learning Statistics for The Behavioral Sciences (MindTap C...StatisticsISBN:9781305504912Author:Frederick J Gravetter, Larry B. WallnauPublisher:Cengage Learning

Statistics for The Behavioral Sciences (MindTap C...StatisticsISBN:9781305504912Author:Frederick J Gravetter, Larry B. WallnauPublisher:Cengage Learning  Elementary Statistics: Picturing the World (7th E...StatisticsISBN:9780134683416Author:Ron Larson, Betsy FarberPublisher:PEARSON

Elementary Statistics: Picturing the World (7th E...StatisticsISBN:9780134683416Author:Ron Larson, Betsy FarberPublisher:PEARSON The Basic Practice of StatisticsStatisticsISBN:9781319042578Author:David S. Moore, William I. Notz, Michael A. FlignerPublisher:W. H. Freeman

The Basic Practice of StatisticsStatisticsISBN:9781319042578Author:David S. Moore, William I. Notz, Michael A. FlignerPublisher:W. H. Freeman Introduction to the Practice of StatisticsStatisticsISBN:9781319013387Author:David S. Moore, George P. McCabe, Bruce A. CraigPublisher:W. H. Freeman

Introduction to the Practice of StatisticsStatisticsISBN:9781319013387Author:David S. Moore, George P. McCabe, Bruce A. CraigPublisher:W. H. Freeman

MATLAB: An Introduction with Applications

Statistics

ISBN:9781119256830

Author:Amos Gilat

Publisher:John Wiley & Sons Inc

Probability and Statistics for Engineering and th...

Statistics

ISBN:9781305251809

Author:Jay L. Devore

Publisher:Cengage Learning

Statistics for The Behavioral Sciences (MindTap C...

Statistics

ISBN:9781305504912

Author:Frederick J Gravetter, Larry B. Wallnau

Publisher:Cengage Learning

Elementary Statistics: Picturing the World (7th E...

Statistics

ISBN:9780134683416

Author:Ron Larson, Betsy Farber

Publisher:PEARSON

The Basic Practice of Statistics

Statistics

ISBN:9781319042578

Author:David S. Moore, William I. Notz, Michael A. Fligner

Publisher:W. H. Freeman

Introduction to the Practice of Statistics

Statistics

ISBN:9781319013387

Author:David S. Moore, George P. McCabe, Bruce A. Craig

Publisher:W. H. Freeman