Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

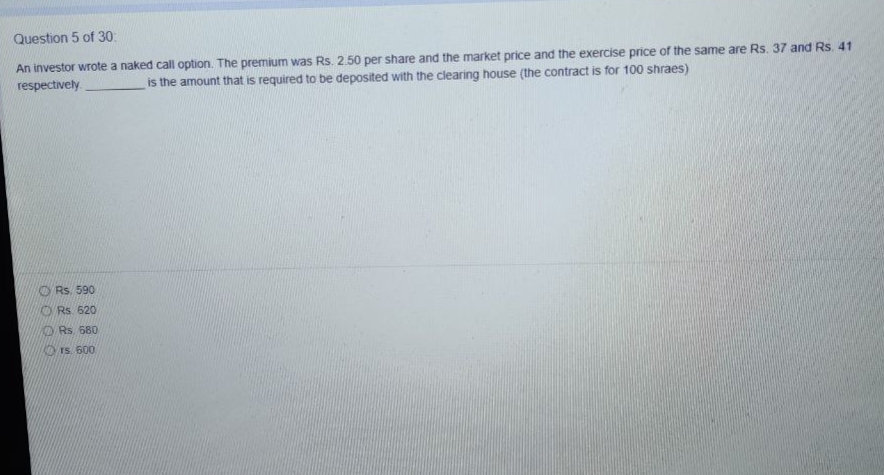

Transcribed Image Text:Question 5 of 30:

An investor wrote a naked call option. The premium was Rs. 2.50 per share and the market price and the exercise price of the same are Rs. 37 and Rs. 41

respectively

is the amount that is required to be deposited with the clearing house (the contract is for 100 shraes)

Rs. 590

O Rs 620

ORs. 680

rS. 600

O O O O

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Q.22 You are considering an investment in 30 year bond issued by Toy Company. The bonds have no special covenants and the 1 yr T bills are currently earning 5.25% The following information is available: Real risk free rate = 2.25% Default Risk Premium = 1.25% Liquidity risk premium = 0.50% Maturity Risk Premium = 2.00% What is the inflation premium?arrow_forward13 You purchased four call option contracts with a strike price of $25.20 and an option premium of $.84. You held the option until the expiration date. On the expiration date, the stock was selling for $22.50 a share. What is the total profit or loss on your option position? Skipped eBook Mc Graw Hill Multiple Choice O O O O O -$336 -$744 $1,416 $744 -$1,416arrow_forwardvi.2arrow_forward

- Close Hend reeks 103 103 103 103 Maximum gain Terminal value Net gain Calls Strike Price Expiration Volume Last 5.20 February March 72 41 8.40 April 16 July 8 100 100 100 100 10.68 14.30 Puts Volume Last 50 29 10 2 2.40 4.90 6.60 10.10 Suppose you buy 30 March 100 put option contracts. What is your maximum gain? On the expiration date, Hendreeks is selling for $84.60 per share. How much is your options investment worth? What is your net gain? Note: Do not round intermediate calculations.arrow_forwardQuestion 2 Let 5-532,0-30%,r-65%, and 6-1% (continuously compounded). Compute the Black-Scholes price for a $35-strike European put option with 9 months until expiration Selected Answe Answers $4.02 $4.02 $2.63 $5.6) Od 34:21 11.00arrow_forward6- A put option (with shares as the underlying asset) was originally purchased for $1.44 and is now trading for $2.82. The exercise price is $34 and the underlying share is currently trading for $31.64. What is the intrinsic value of the option? a. $2.82 b. $0.00 c. $2.36 d. $1.44arrow_forward

- helpparrow_forwardWich blank woting all diectors p for electics same time in one 20. A bank with long-term fixed-rate assets fundded with short-term rate-sensitive labilities could do which of the following to limit their interest rate risk? L Buy a cap II. Buy an interest rate swap II1. Buy a floor IV. Sell an interest rate swap A. I and II only B. III cely C. I and IV only D. II and IIl only E. IIl and IV cnly at a floating rate of interest. What kind of risk does the subsidiary have? What kind of vwap Be specific. 21. A U.S. firm has a European subsidiary that earns euros. The subsidiary has berowed delarsarrow_forwardPlease answer fast please arjent help please ASAP pls answer fastarrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education