ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

thumb_up100%

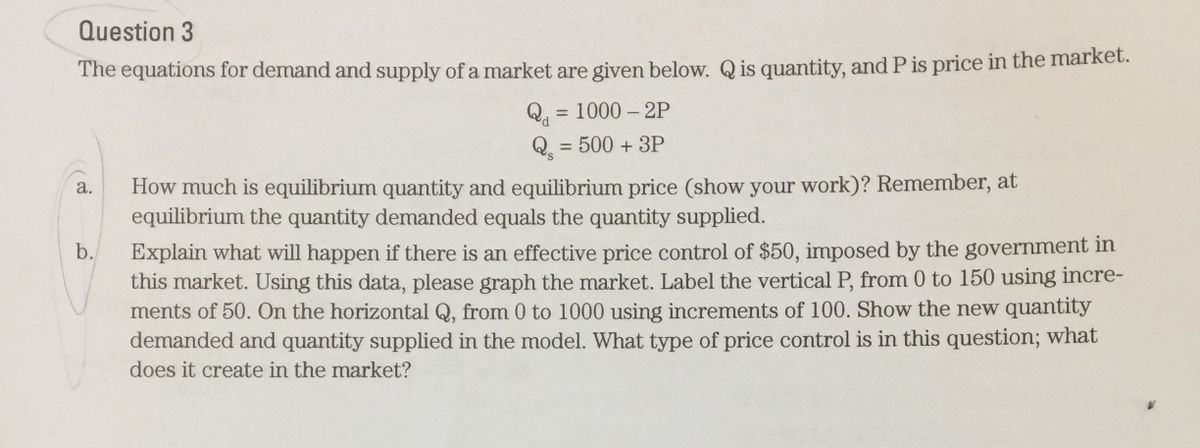

Transcribed Image Text:Question 3

The equations for demand and supply of a market are given below. Q is quantity, and P is price in the market.

Qa

= 1000 - 2P

%3D

Q = 500 + 3P

%3D

How much is equilibrium quantity and equilibrium price (show your work)? Remember, at

equilibrium the quantity demanded equals the quantity supplied.

a.

Explain what will happen if there is an effective price control of $50, imposed by the government in

this market. Using this data, please graph the market. Label the vertical P, from 0 to 150 using incre-

ments of 50. On the horizontal Q, from 0 to 1000 using increments of 100. Show the new quantity

demanded and quantity supplied in the model. What type of price control is in this question; what

b.

does it create in the market?

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps with 1 images

Knowledge Booster

Similar questions

- help please answer in text form with proper workings and explanation for each and every part and steps with concept and introduction no AI no copy paste remember answer must be in proper format with all workingarrow_forwardThe table shows the demand and supply schedules for hot chocolate. What is the market equilibrium in the hot chocolate market? The equilibrium price is $a cup. The equilibrium quantity is cups a day. Price (dollars per cup) 1.10 1.45 1.80 2.15 2.50 Quantity demanded Quantity supplied (cups per day) 200 175 150 125 100 110 130 150 170 190arrow_forwardDemand Schedule Supply ScheduleP Q P Q10 30 10 809 35 9 748 40 8 687 45 7 626 50 6 565 55 5 504 60 4 443 65 3 382 70 2 321 75 1 261. Graph the demand and supply schedules (above). What are the (approximate) Price and Quantity in this market?arrow_forward

- 2. Consider the Table below representing the number of 21-inch colour TV's individuals are willing to purchase in Ndola and Kitwe: Price Quantity Demanded-Kitwe Quantity Demanded- Ndola К350 100 75 К325 150 100 К300 200 125 K275 250 150 K250 300 175 a) Plot these data, with price (P) on the vertical axis and quantity (Q) on the horizontal axis. Connect the points for quantity demanded in Ndola and Kitwe. Lebel the Ndola line D1 and the Kitwe line D2). b) Find the increase in the quantity of TV units purchased in Ndola and Kitwe when the price of TV's is lowered from K300 to K275. c) Find the slope of the Demand lines D1 and D2 when the price is lowered from кз00 to K275. d) What does the difference in the slope of demand lines D1 and D2 indicate? e) Obtain the National demand schedule if Kitwe and Ndola were the only cities in the country. f) Explain what will happen to demand for TVs if one of the following happen i) ii) iii) Price of DSTV increases There is a wage freeze in the…arrow_forward1. Use the graph below to answer the questions that follows: Price Dollars per gallon GH¢9.00 GH¢7.00 GH¢4.00 12,000 18,000 30,000 Quantity (gallons per day) d. Suppose imposition of maximum price legislation reduced the price oil from the equilibrium price to the maximum price control price. Calculate: Price elasticity of demand Price elasticity of supply i. ii. e. From your calculation, which of the two curves is more elastic? Explain your answer.arrow_forwardHi, may I please get help with question (d), (e), (f)? I already got answers for the first 3.arrow_forward

- Help me answer questions 1 and 2! Please and thank youarrow_forwardAbove is the supply and demand graph in a market. Answer the following questions based on the graph: 3.1. What are the equilibrium price and quantity in the market? 3.2. What are the quantity supplied, quantity demanded, and price at a shortage of 400 units? 3.3. Whar are the quantity supplied, quantity demanded, and price at a surplus of 200 units?arrow_forwardAnalyze the following statements and categorize them into Determinants of Demand(DD) or Determinants of Supply (DS)._________6. There is a change in Quantity Supplied because of the increasing cost ofproduction.arrow_forward

- Question attahed in imagearrow_forwardQ2- Price $ 10.00 20.00 30.00 40.00 50.00 60.00 70.00 Quantity Demanded 28 24 20 16 12 8 4 Quantity Supplied 0 3 6 9 12 15 18 Use the information in the table above to: a. find the equilibrium price and quantity. b. Graph the demand and supply curves and identify the equilibrium price and quantity.arrow_forwardPlease do Carrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education