ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

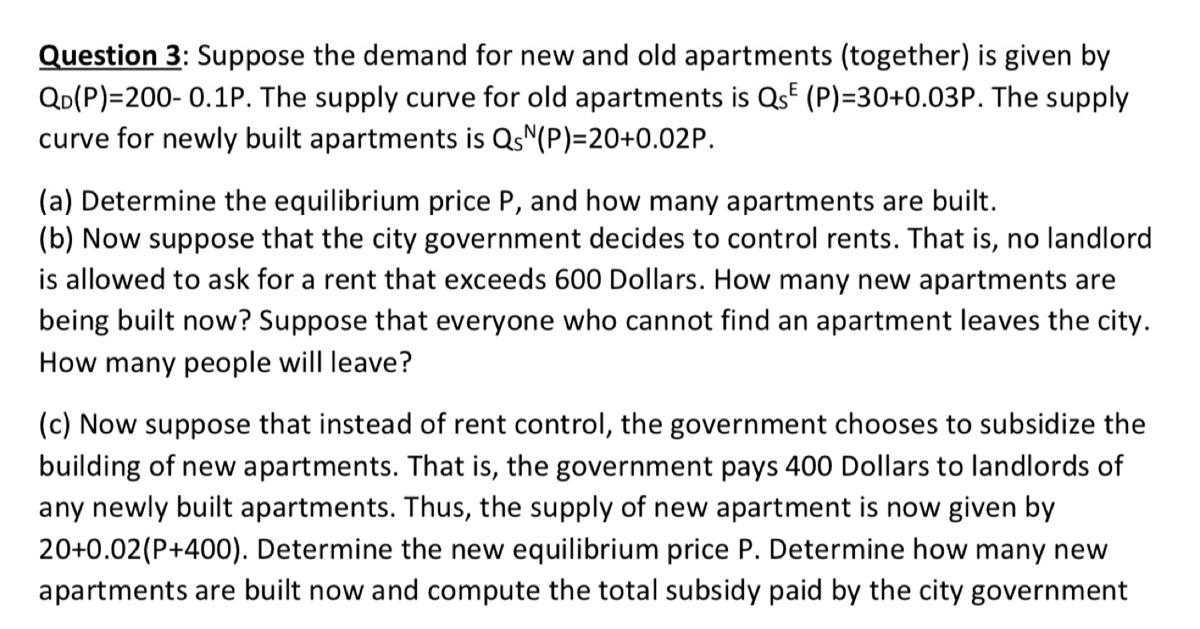

Transcribed Image Text:Question 3: Suppose the demand for new and old apartments (together) is given by

QD(P)=200- 0.1P. The supply curve for old apartments is Qs (P)=30+0.03P. The supply

curve for newly built apartments is QsN(P)=20+0.02P.

(a) Determine the equilibrium price P, and how many apartments are built.

(b) Now suppose that the city government decides to control rents. That is, no landlord

is allowed to ask for a rent that exceeds 600 Dollars. How many new apartments are

being built now? Suppose that everyone who cannot find an apartment leaves the city.

How many people will leave?

(c) Now suppose that instead of rent control, the government chooses to subsidize the

building of new apartments. That is, the government pays 400 Dollars to landlords of

any newly built apartments. Thus, the supply of new apartment is now given by

20+0.02(P+400). Determine the new equilibrium price P. Determine how many new

apartments are built now and compute the total subsidy paid by the city government

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 4 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Suppose the demand function for a product is given by the function: D(q) = -0.018q+50.4 Find the Consumer's Surplus corresponding to q = 1,550 units. (Do no rounding of results until the very end of your calculations. At that point, round to the nearest tenth, if necessary. It may help you to sketch the demand curve, which crosses the horizontal at q = 2,800.) dollars Answer:arrow_forwardAn economist estimates that a market has a demand curve of the form P = 26 - (0.867) Q and a supply curve of the form P = 0.5 + (1.21) Q. (See the curves graphed in the figure below.) Accordingly, she estimates that the equilibrium price ( P e) in the market will be $15.36 (or $15.355561). This means that the amount of the product bought and sold in the market must be ____.arrow_forwardIn this problem, p is in dollars and x is the number of units. The demand function for a certain product is p = 144 – x² and the supply function is p = x² + 2x + 104. Find the equilibrium point. (x, p) = ( Find the consumer's surplus there. (Round your answer to the nearest cent.) 2$arrow_forward

- The demand and supply functions for good x and good y are given as: Q = 145-2Px + Py Q& = -45 + Px Q = 30 + Px - 2Py Q5 = -40 + 5Py where QP, Q, and P₁ denote the quantity demanded, quantity supplied, and price of good i = x and y, respectively. (a) Determine the equilibrium price and quantity for good x and good y. (b) Are these goods substitutes or complements? Justify your answer.arrow_forwardConsider the horizontal sum of the two demand curves P = 8- Q and P = 12- Q. When 8arrow_forwardIf the number of buyers in a market increases from 25 to 75, you would expect the equilibrium price to _____ and the equilibrium quantity to _____, holding all else constant. Group of answer choices remain the same; remain the same decrease; decrease decrease; increase increase; increase increase; decreasearrow_forward

- Let Qd = 30 - 6 P and Qs = 9 P be the demand and supply curves for soft drinks. Then the equilibrium combination in the market is: a. P* = 2; Q* = 18 b. P* = 2; Q* = 15 c. P* = 18; Q* = 2 d. P* = 10; Q* = 90arrow_forwardSuppose consumers will demand 40 units of a product when the price is RM12.75 per unit and 25 units when the price is RM18.75 each. Find: The demand function. i) ii) 1) iv) Price per unit when 37 units are demanded Quantity (units) demanded when the price is RM20.00. The equilibrium point if the supply equation is p = q - 0.75arrow_forwardAn economist estimates that a market has a demand curve of the form P = 37- (1.23) Q and a supply curve of the form P = 1 + (0.984) Q. (See the curves graphed in the figure below.) Accordingly, she estimates that the quantity equilibrium (Qe) in this market will be 16.26 (or 16.260163) and that the equilibrium price (Pe) in the market will be. (Answer may be rounded to nearest hundredth.) Supply X Demand Q OA. $20.84 O B. $12.20 O C. $23.00 O D. $17arrow_forward

- If both supply and demand decrease, the equilibrium price A) does not change. B) cannot be predicted. C) rises. D) falls.arrow_forwardAssume that the supply and demand equations for 1-shirts at store A and 2 in a particular week are. = .7q+ 3 offer p= - 1.7q + 15 Demand Determine the equilibrium quantity and price that stabilizes the T-shirt market. (1) (4$5.5) (2) (7, $8) (3)($9.5) (4) (5, $6.5)arrow_forwardAbove is the demand schedule for tickets to a Carnegie Hall performance of the Grateful Dead. Carnegie Hall seats 1,800 people. What is the equilibrium price and quantity for a concert of the Grateful Dead at Carnegie Hall? If tickets were sold for $18, what would happen (be specific)?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education